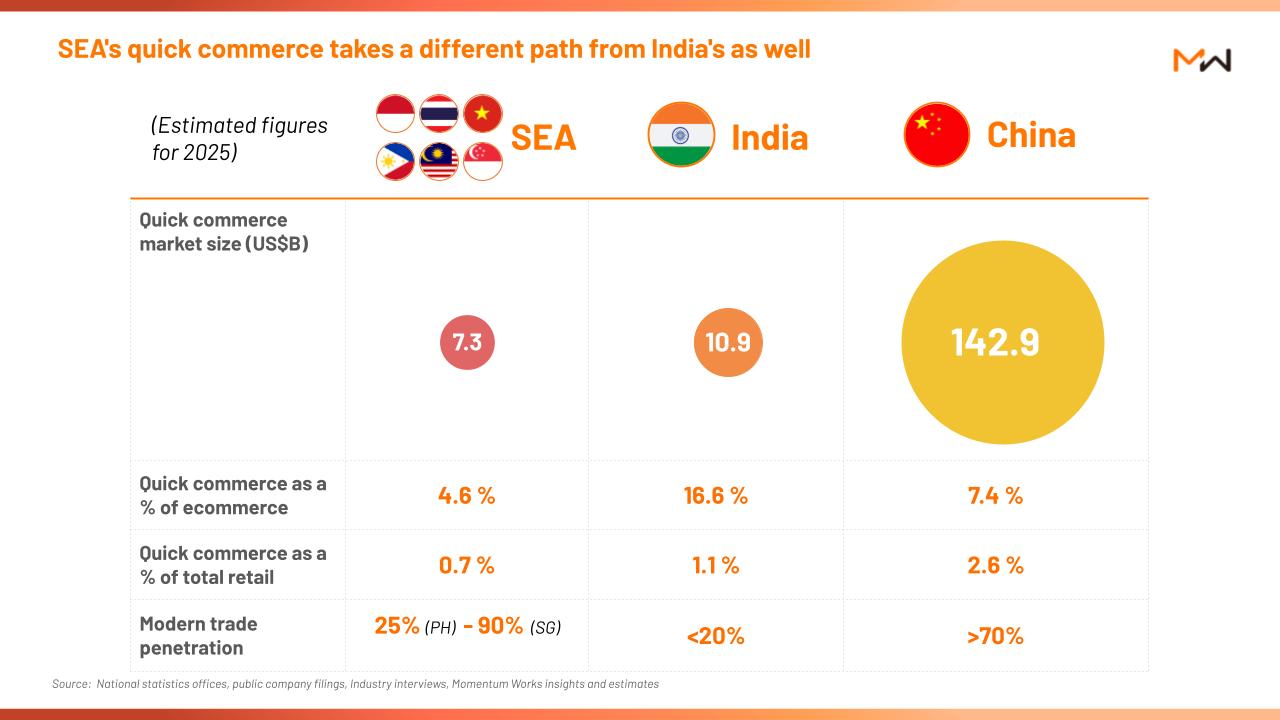

Quick commerce in Southeast Asia has finally hit the scale that matters — but not in the way most observers expected.

Here’s the twist: in China, quick commerce replaced trips to the store. In India, dark stores leapfrogged a thin retail network. In SEA, quick commerce is doing neither. It’s layering on top of dense offline retail and existing food delivery infrastructure — and the platforms driving it (Grab, ShopeeFood, Foodpanda and their peers) already had the riders, the stores, and the user base before quick commerce was a category.

Today we are releasing the Momentum Works Quick Commerce in Southeast Asia 2026 report, with in-depth analysis of how the region’s biggest platforms are stitching grocery, food and on-demand essentials into a single fulfilment layer — and why, despite all the infrastructure being in place, the category is still smaller than its potential.

The supply side is solved. What’s missing is demand.

SEA has the riders. It has stores. It has platforms with hundreds of millions of MAUs. What it doesn’t yet have, at scale, is the habit — consumers reaching for an app instead of walking to the minimart downstairs. And in a price-sensitive region where offline retail is genuinely cheap and genuinely close, that habit is expensive to build.

Underneath all this, the economics of the category are being rewritten. A few things we dig into in the report:

- SEA quick commerce extends offline retail – it doesn’t replace it. Unlike India’s dark-store leapfrog, SEA already has dense minimart and wet market networks. The winners will be those who plug into this fabric, not those who try to disrupt it.

- Demand is the binding constraint — not supply, not fulfillment. The infrastructure exists. The habit doesn’t. Closing that gap takes sustained subsidy to reach price parity with offline — and not every player has the balance sheet.

- Savings, not speed, will unlock mass demand. Speed is the headline pitch, but SEA consumers are structurally price-sensitive. As long as on-demand carries a premium, it stays a category for the affluent and the rushed.

- Six markets, six playbooks. Indonesia is not Vietnam is not the Philippines. The operators trying to copy-paste one model across the region will be disappointed — and some already have been.

- Food delivery platforms hold the structural advantage. Grab, ShopeeFood and their peers have the user base, the rider fleet, and the merchant relationships. Standalone quick commerce players are competing on someone else’s home turf.

For platforms, retailers, FMCG brands and investors, the question is no longer whether quick commerce in SEA is real. It’s who closes the demand gap first — and whether anyone makes money before they do.

Quick Commerce in Southeast Asia 2026 is now available at US$59.95. You can get your copy from this link.

👉 Quick Commerce in Southeast Asia 2026