Our friends at Cento Ventures have been systematically tracking tech and venture investments in Southeast over the years, resulting in a very good repository of intelligence about evolving trends of the region’s booming tech ecosystem.

For the past few iterations, Momentum Works has had the privilege to partner with Cento Ventures on the Chinese release of the Southeast Asia Tech Investment report. We have included a section with specific data points and analyses for Chinese investors and the tech ecosystem that are expanding into the region.

In the newly released Southeast Asia Tech Investment FY 2020 Report, the latest in the series, we thought the following insights are worth noting:

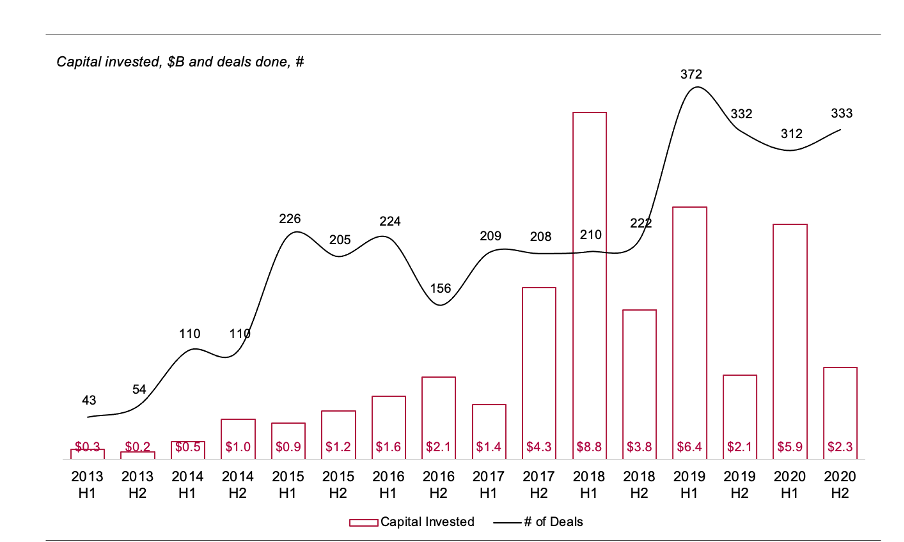

- SEA tech investment volume only dropped slightly from 2019

Despite the hit of COVID-19, the tech investment scene in Southeast Asia remained quite resilient and achieved an overall $8.2B investment in 2020. Total investment amount and deal activities dropped -3% and -8% respectively.

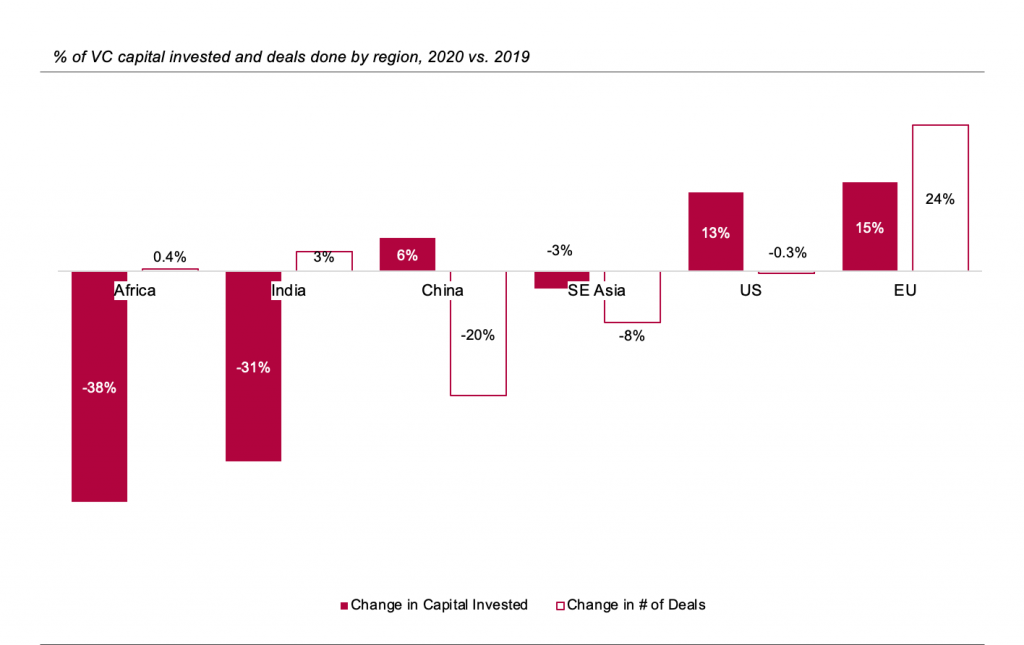

- Among all emerging markets, SEA was least impacted by COVID-19

Although developed markets became more favored by investors amid COVID times, Southeast Asia significantly outperforms all its emerging market counterparts. Overall perceptions of the SEA startup ecosystem remained stable, only seeing a minor decrease in capital invested and deals proceeded.

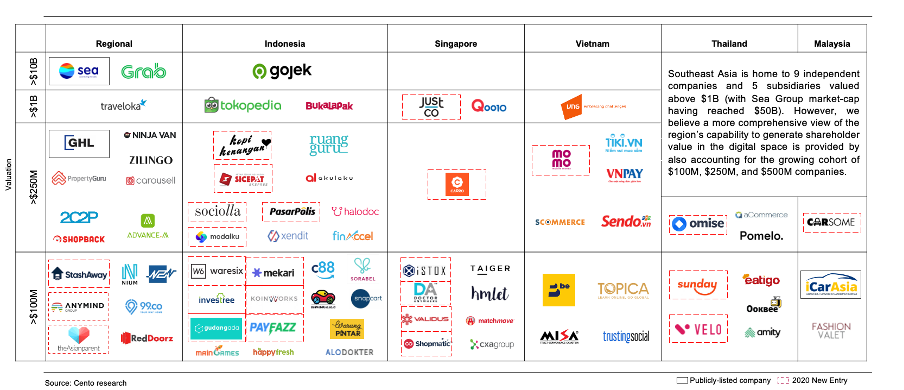

- New tech leaders valued above $250M emerged in SEA

2020 witnessed a new set of leading tech companies in SEA, especially the unicorns (i.e JustCo) and the crowd valued above $250M (i.e. Carsome, Sociolla, and Momo).

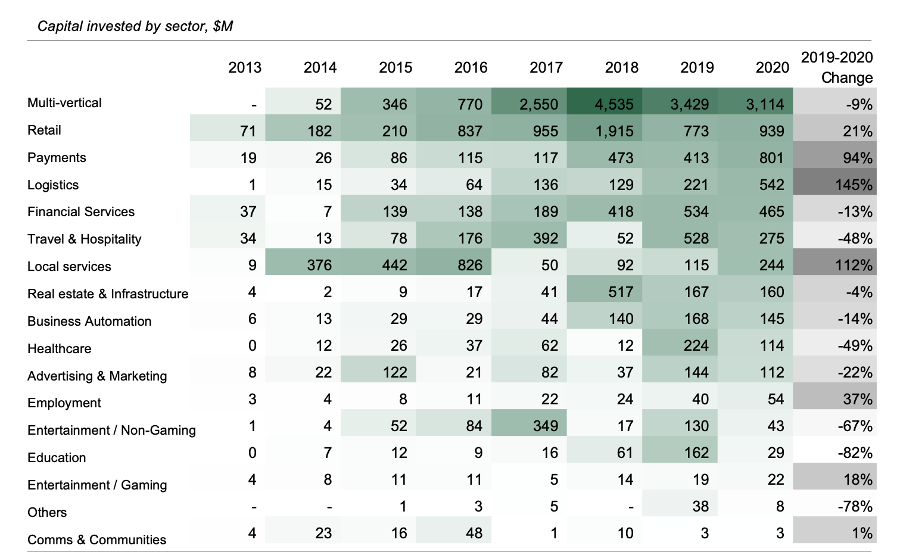

- Payments, logistics and local services dominated the in-bound investment, and FinTech investment soared

Sectoral performance varies significantly –payments, logistics and local services took up the top three seats in the capital invested, while healthcare and edutech failed to deliver its expected growth. (MW community reflected on this previously)

Deal-wise, FinTech investment accounts for 20% of the overall amount.

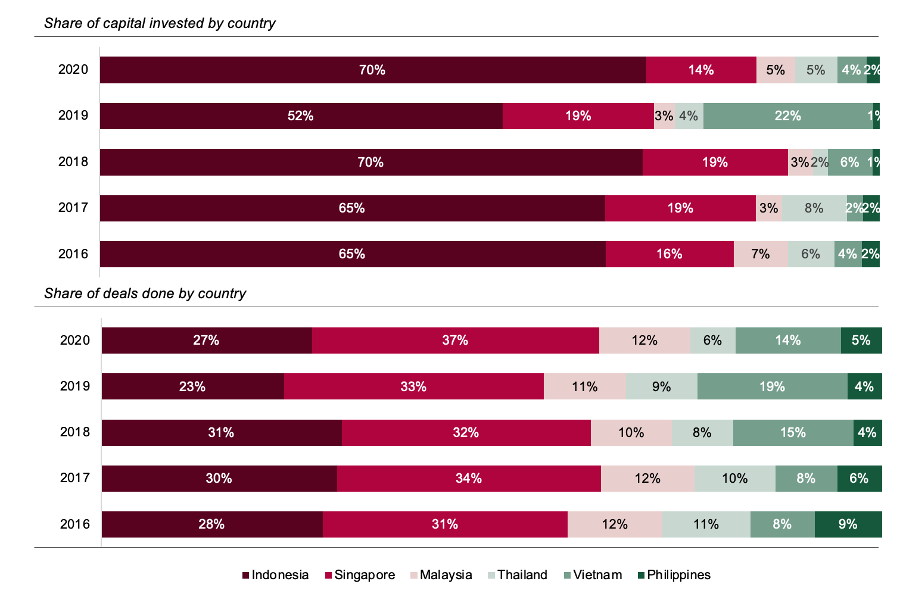

- Indonesia attracts 70% of capital invested in SEA in 2020

Indonesia certainly picked up the momentum and attracted 70% of the capital invested in SEA in 2020, headed by the financing of a few mega-deals including Gojek, Bukalapak, and Waresix etc. Singapore, Malaysia and Thailand followed, but Vietnam saw a significant decrease after NOW’s financing completed in 2019.

Singapore pioneered in the number of deals made in 2020. In FinTech investment particularly, it took up 43% of the share of deals.

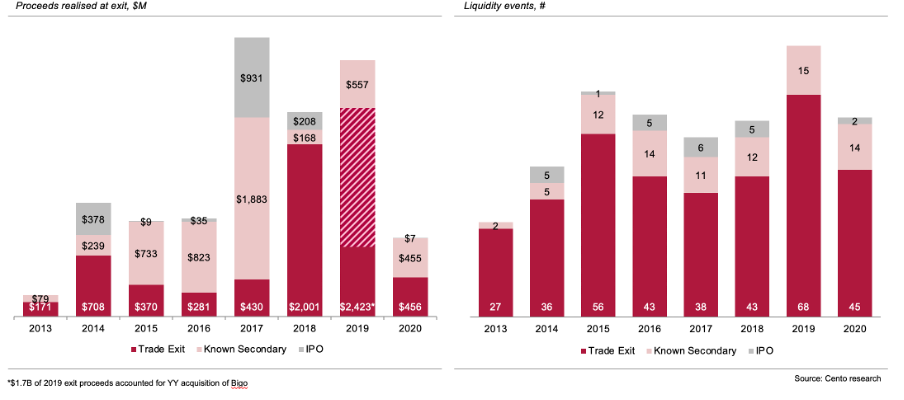

- Lower exits proceeds generated, along with lower exit valuations

In general, exit proceeds were realized at a significantly lower value in 2020.

Matthew effect also appears in SEA’s liquidity event and proceed scene. $1M – $50M exits in 2020 almost doubled that of 2019, while exits above $50M saw a sharp decline.

Finally, some thoughts and questions worth looking next:

- SEA has inevitably benefitted from the escalating tension between China and India, as Chinese capital rushed out and flew into the region. We have reflected on this ourselves the end of 2020. A more important question is, will this be a lasting scene we can expect?

- Under pandemic, other emerging markets all suffered significantly in 2020, except for SEA. What’s the fundamental driver, and what can we reflect from the SEA investment scene to understand other developing markets better?

To gain a better understanding of the tech investment landscape of Southeast Asia in 2020, email us at [email protected] to request the full report. Please share your questions and thoughts with us too – we are curious to hear what you have in mind as well.

In the meantime, Momentum Works and Cento Ventures will be hosting a briefing on Southeast Asia investment the end of April. If you’re interested to join, please drop us an email to register, places are limited.