One of the key developments in Malaysia’s digital space in 2018 was the intense competition within the crowded e-wallet space.

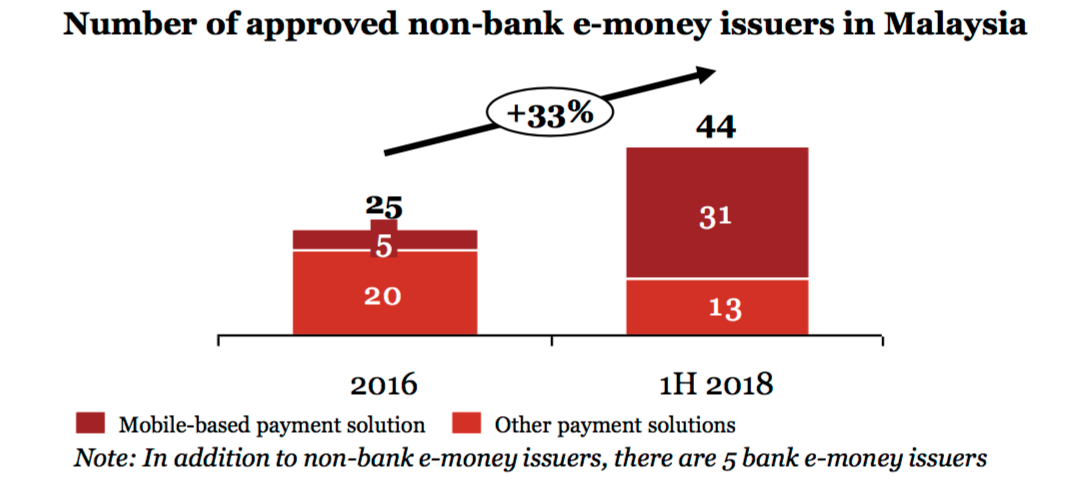

E-wallet licenses are issued by The Central Bank of Malaysia (Bank Negara Malaysia, BNA), and according to the latest count there are a total of 44 licensed e-wallets (5 banks and 39 non-banks).

According to BNM, Malaysia’s consumer behaviour is still 80% cash driven and a move towards e-payments could potentially save as much as 1% of the country’s economy. The aim is to increase the number of e-payment transactions per capita from 44 transactions to 200 transactions, and reduce cheques by more than half from 207 million to 100 million per year.

So what does BNM do? It has been pushing for e-payments in three waves.

In the first wave, it’s aim was to promote electronic fund transfers to replace cheques. In a second wave, they set out to promote debit cards over cash. And in the third and current wave, BNM made it easier to make mobile payments through e-wallets through a variety of ways, including creating a shared payment infrastructure, linking e-wallet accounts to a unique customer number (e.g. mobile or Malaysia ID card), and using standardised QR codes. E-wallets are especially attractive for merchants as they require no extensive infrastructure costs since they rely mainly on QR codes as opposed to POS terminals.

According to a FT Confidential Research survey published around a week ago, the top 3 leading e-wallets in Malaysia are GrabPay (35%), Boost (24%), Touch n Go (21%) and WeChat Pay (20%).

Let’s take a deeper look at each of these e-wallets :

-

GrabPay

Grab rolled out its GrabPay wallet in Malaysia in June 2018.

The e-wallet is a part of the Grab app itself and consumers can use it to pay for Grab rides, GrabFood, partner merchant outlets as well transfer funds amongst each other.

Since Grab is already integrated within the Grab app it has a head start over others. Saves the need to spend crazy marketing dollars getting customers to download an additional app. Grab has more than 100 million downloads across SEA and it can be used in Malaysia even if it was downloaded elsewhere. Great for Singaporeans (and others) who frequently visit for business and shopping.

Grab’s core services of food and transport are frequent needs, and they provide a strong use case for the e-wallet. Grab has also launched several incentives to get customers to use its e-wallet (instead of cash/credit card) to pay for the services. An example is getting extra GrabReward points that can be used to redeem cash rebates, F&B, retail or future Grab services.

Also, Grab’s strategic partnerships have helped it to further enhance the use case. It has partnered with over 500 popular food and beverage outlets, KLIA Express and Maybank to exponentially increase its use as it can leverage its partner merchants.

However, the landscape is filled with other well-funded e-wallets also with existing use cases (we discuss this below). With them fast onboarding various merchants and throwing huge promotions to attract customers, it will remain to be seen how Grab continues to maintain this lead.

-

Boost

Boost is an e-wallet developed by the Axiata group, Malaysia’s telecommunications giant. As of December 2018, it has 3.3 million registered users, and 50,000 touch points.

Apart from allowing payments with partner merchants and other typical e-wallet services, it allows paying utility bills with partners such as Telekom Malaysia, Astro and Syabas.

Boost has been one of the most aggressive e-wallets in terms of marketing. Instant cash rebate via its addictive shake rewards after each transaction has made it popular and addictive among users.

It is also aggressive in onboarding merchants. Boost’s CEO had announced that they were targeting to reach 100,000 merchants by end of 2018 and it seems like this message was received loud and clear by their marketing department because they’ve been going all out to expand their reach. The merchants they have onboarded, include large brands, as well as smaller convenience stores, grocery shops, eating joints, hardware stores and even pasar malam (night market) businesses.

Boost also announced its partnership with the Chinese giant UnionPay International (UPI) in July 2018. Boost users will be able to make payments to any merchants that accept UPI. This strategy signals that they are keen on expanding overseas which makes sense since Malaysia is a small market and UPI’s 51 million merchants worldwide will help it boost (pun intended) its presence globally.

- Touch-n-Go (TnG)

Touch-n-Go (TnG) started as smart cards for highway tolls and has now expanded to e-wallets. TnG e-wallet is a joint venture between China’s Alipay and CIMB Group (second-largest bank in Malaysia by assets). TnG e-wallet users can use the credits to pay for toll at selected highways. It has 2.3 million registered users and is accepted by more than 30,000 merchants. They also claim to be on their way to hitting the target of 40,000 merchants by the first quarter of 2019.

Being a national smart card that is used by almost every commuter carries with it a heavy burden. TnG had a few hiccups on communications regarding how consumers can use the money in the e-wallet services, leading to wide criticism and scrutiny. It has since improved its services – gaining back its customer trust.

Now it remains to be seen how TnG will expand. Will they extend their e-wallet to other transport services like bus and railways?

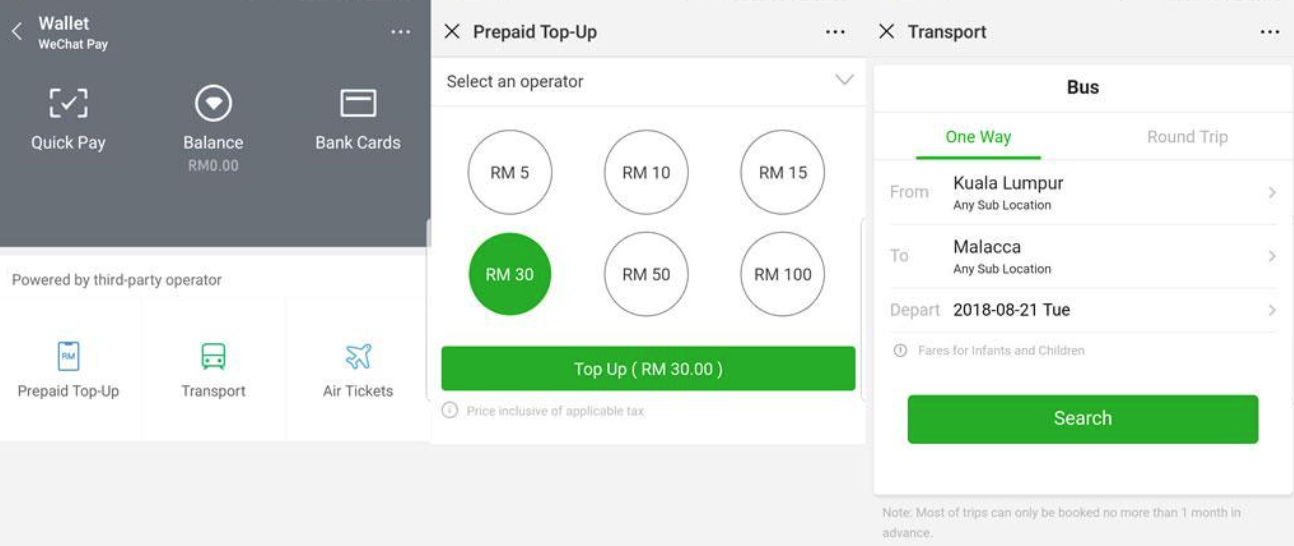

- WeChat Pay

Chinese e-wallet giant WeChat Pay launched a Malaysian version of the app WeChat Pay My in second half of 2018, after a long two-year beta testing phase. This was the first time WeChat Pay expanded outside China and Hong Kong.

This is different from its expansion strategy in other regions, where WeChat Pay doesn’t have a localised product but is mainly used by Chinese tourists to pay using their e-wallet. In this case, they intend on serving Malaysians directly by getting into local payments.

We think WeChat understandably chose Malaysia as an e-wallet testing ground because of the high WeChat user penetration – more than 20 million users in a population of 31.6 million. If WeChat Pay proves to be successful in Malaysia, it can then serve as a model to expand to larger emerging markets in the region.

In a stark contrast to Alibaba’s strategy that prefers joint ventures with local players (Touch-N-Go in Malaysia), WeChat Pay has directly entered the market and has partnered with quite a few local players such as Hong Leong Bank, MOL Pay, iPay88 and Revenue Monster. This gives it access to various local merchants.

However, having joined only recently it won’t be easy to accelerate in the presence of other e-wallets that are fast becoming popular among users.

How many e-wallets till it is too many e-wallets?

We’ve discussed just the top 4 e-wallets but there are 40 more in the market to choose from. However, e-wallet adoption comes with its own challenges in this market

- Cashless doesn’t have to mean only e-wallets. The government and BNM are pushing the cashless narrative hard. However, the challenge for e-wallets is that Malaysia’s small market is already well-served by cards (high penetration of 44.1 million debit cards in a population of 31.6 million). China was able to jump from cash to mobile payments because card adoption came in very late, and mobile payments actually served a need for payment convenience. What’s the pull factor for Malaysian consumers beyond just promotions?

- Too many e-wallets? Even if consumers do want to adopt e-wallets, which one do they go for? To put Malaysia’s numbers into perspective, Indonesia with a 264 million population, has only 35 licensed e-money operators. Not only don’t the economics add up here, consumers are left confused as to which one they should adopt. The more wallets come into the market, and the more competitive they get, the less differentiated the products will be as eventually everyone would want to do everything.

- More e-wallets = more cash burn. E-wallet players in Indonesia got lucky when regulators became stringent about giving out licenses. Grab, Shopee, Tokopedia, Bukalapak – all these unicorns had to suspend their e-wallets and merge with existing licensed players like OVO. This meant fewer big players competing for the same pie. This is not the case in Malaysia where a bigger number of players are battling it out for a much smaller pie.

- No unified QR code. Unlike SGQR, Malaysia doesn’t have a unified QR code for merchants to display. With 44 different e-wallet options, it’s confusing and a hassle for merchants. How do they prioritise without alienating any customer base?

Which players will win? Deep pockets not enough

Needless to say, the e-wallet landscape is highly competitive. Independent players are not only competing amongst themselves, but also with banks that have their own e-wallet, notably MayBank Pay e-wallet, which launched in 2016 without much fanfare, but is gaining popularity and also working with Grab as we mentioned above.

Some of the players are launching very competitive incentives to attract customers. For example, WeChat launched promotions such as RM20 rebates on RM40 worth purchases at petrol stations in early December 2018. However, the CAC is not sustainable, and they had to end it almost a month before its initial end date. Boost too has had huge promotions such as 50% cashback however economics dictate that it can expect to break even only after 2021.

Burning cash can only help in the early days to weed out weaker players without financial might, as Malaysia is already seeing pointed out by Financial Times. In the long run, it’s strong use case that generates customer loyalty that will dictate which remaining players will dominate. This means non-bank e-wallets have a better chance and Grab, Boost, Touch n Go, WeChat Pay are examples of that.

However, none of them would probably achieve the (de facto) duo-poly or dominance Alipay and WeChat Pay are enjoying in China.