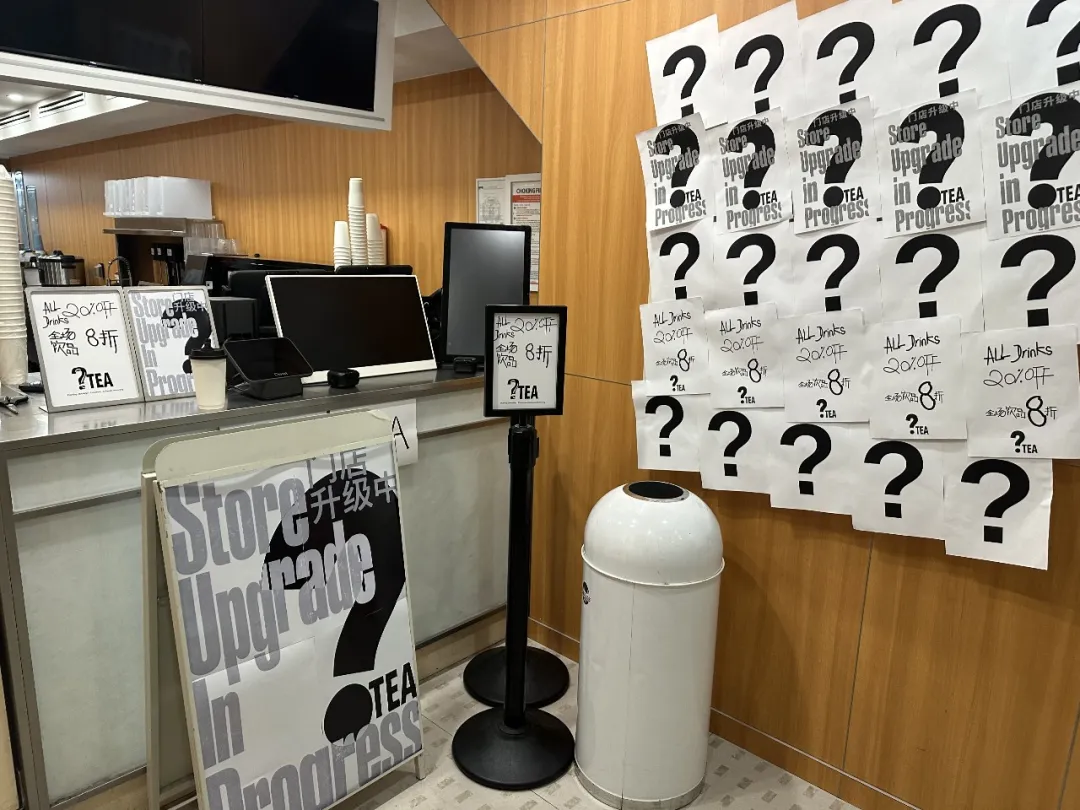

For a branded tea chain, losing your own name on the shopfront is about as dramatic as it gets.

That is what appears to have happened to Molly Tea in New York. Across several branches, the brand’s logo was reportedly covered up and replaced with “? tea”. And it’s not just the signage at the front. Everything in the store, the billboards, the ordering app, even the uniforms have lost its Molly Tea branding.

The funny version of the story is obvious: a Chinese tea chain goes overseas, falls out with its local partner, and ends up as a question mark.

The more interesting version is this: Molly Tea did not become “? Tea” because consumers in the U.S. rejected the product. It became “? Tea” because the market seemed to validate the product faster than the partnership structure could handle.

That is especially striking because Molly Tea was not one of China’s largest tea chains when its New York story began. Founded in 2020, Molly Tea now runs 2,000 stores worldwide, including 2 successful outlets in Singapore.

But back in 2023 when its New York story first began, they reportedly only had around 100 stores in China. It was at that time a local partner from New York approached Molly Tea HQ with a partnership offer. He will develop and operate five stores in New York – and pay the required fees for using the brand name, while Molly tea will provide the technical, operational, and supply-chain support.

At the time, Molly Tea did not have any serious plans for the U.S. market. Their natural response was “Why not try it?”. They also agreed on an effective 20%/80% structure in favor of the local partner in 2025.

But this willingness changed as Molly became more successful in China.

Its first New York store, in Flushing – a neighbourhood with a large Asian community and many Chinese F&B joints – reportedly became a breakout hit. According to the Chinese outlet 36Kr, monthly revenue reached around half million dollars.

More stores followed in Brooklyn, Manhattan’s Chinatown, and near Columbia University.

Then the relationship between Molly Tea headquarters and its local U.S. partner broke down.

The brand says the partner breached their agreement and misused its trademarks. The partner says he helped build the U.S. market from scratch, took the early risks, and was squeezed once the business became valuable.

The case is still in court, and we trust the truth will surface with the judgement.

But the business lesson is already visible: the dangerous moment in overseas expansion is not always when the first store fails. It is often when the expansion succeeds too well.

When things work too well

It is a pattern we have watched play out as Chinese F&B has gone abroad: these partnerships work fine while the market performs as expected, but once it performs much better than expected, people start having second thoughts.

When the store is still an experiment, both sides can live with ambiguity. The brand needs someone on the ground. The local partner needs a product and brand to operate. The upside is still theoretical.

Once the store works, everyone starts recalculating.

Headquarters may think: consumers are here because of our product, our recipes, our brand, our training, our supply chain.

The local partner may think: this market only exists because I found the location, signed the lease, hired the team, dealt with landlords, and operated through all the early uncertainty.

Both would think that they deserve a bigger part of the pie. Both can be right. That is why these disputes are hard. And that is where Molly Tea U.S. is now.

The franchisee who thinks he is a founder

One reason overseas F&B partnerships become emotionally messy is that “franchisee” is often the wrong word for the first local partner.

In a mature franchise system, a franchisee buys into a tested machine. The brand has already built the playbook: suppliers, store standards, training, marketing, disclosure documents, site-selection logic, and operational control.

The franchisee executes. But in a new overseas market, the machine often does not exist yet.

The first partner may be finding landlords, signing leases, hiring staff, solving local supply-chain issues, managing regulators, localising operations and explaining the market back to headquarters. That is not just store operation. That is market creation.

Headquarters may see a franchisee. The local operator may see himself as the person who proved the country.

That gap is where the dispute begins.

The China playbook meets American boredom

There is a phrase Chinese operators like to use: 降维打击, or “dimensionality-reduction attack”.

It comes from Liu Cixin’s The Three-Body Problem, where a weapon flattens an enemy into a lower dimension, making resistance impossible. In business slang, it means entering a weaker market with superior capabilities and overwhelming it.

You can see why Chinese F&B brands might think this way.

China’s F&B market is brutal. Products change quickly. Prices are compressed. Consumers are demanding. Delivery platforms, social media, supply chains and store operations are all highly competitive.

If you can survive China, it is tempting to look at the US and think: slow service, high prices, sleepy competition – easy.

Just bring the Chinese playbook and flatten the market. The problem is that America refuses to be flattened.

The hard things are often boring: franchise disclosure, state-by-state rules, landlord negotiations, lease guarantees, labour, local regulations, and the partner who knows all of these things better than you do.

The Chinese playbook does not steamroll the boring stuff. It breaks on it.

This is the part many fast-growing brands underestimate. They are good at speed. But speed is not the same as control.

And speed without structure often creates the conflict that later slows everything down.

Get on the bus first, buy the ticket later

A lot of overseas expansion starts with a practical compromise. The opportunity is hot. Competitors are moving. Good locations are scarce. Everyone wants to show progress.

So the brand and partner move first and formalise later.

Open the store. Test demand. Fix the paperwork afterwards.

In Chinese, this is sometimes described as “getting on the bus first, buying the ticket later”.

It is not always irrational. Early markets are uncertain, and if both sides waited for perfect documents, many stores would never open.

But this approach only works while trust is strong.

Once the relationship changes, every missing detail becomes dangerous.

Was the partner allowed to open the next store? Did the brand promise territorial protection? Could headquarters change the equity split? Who controls the store entity? Who owns the customer relationship? Who has the right to appoint management? What happens if headquarters wants to go direct?

These questions are boring at the beginning.

They become existential at the end.

The model is the strategy

And notably, this is not an isolated case, and not to Chinese brands alone. Similar partner-control issues have happened before, notably Gong Cha’s Singapore partner flipping all the stores into their own brand – LiHo, and a pizza chain in Korea. We are also seeing an active tussle playing out with a very large beverage brand in Southeast Asia.

In Momentum Works Chinese F&B in Southeast Asia and Coffee and Tea Chains in Southeast Asia report, we have discussed extensively how different partnership models have played out – along with the perils each comes with.

The Molly Tea tussle falls squarely in some of these patterns, and both partiers should have seen it coming.