Delivery Hero spent more than a decade assembling leading food delivery positions across East Asia. Today, much of that portfolio is being unwound.

foodpanda Taiwan is being sold to Grab, Baemin is on the market, foodpanda has lost leadership in Hong Kong, and the company has already exited Japan.

At the same time, a new generation of Asian operators – Meituan, Coupang and Grab – are rewriting the competitive playbook, bringing experience forged in some of the world’s toughest delivery markets.

Today, we are releasing the Food Delivery Platforms in East Asia 2026 report, Momentum Works’s first dedicated to the four major food delivery markets of Hong Kong, Taiwan, South Korea and Japan.

The four markets in East Asia share similar economic and demographic conditions for food delivery – developed, urbanised, Confucian work cultures, declining birth rates, and a commoditised foodservice base where chains hold about half of value.

Yet food delivery penetration varies drastically, ranging from just ~3% in Japan to over 20% in South Korea – suggesting that operator execution, not market readiness alone, determines market outcomes.

Key findings of the report:

-

- The four East Asian markets vary greatly in food delivery development

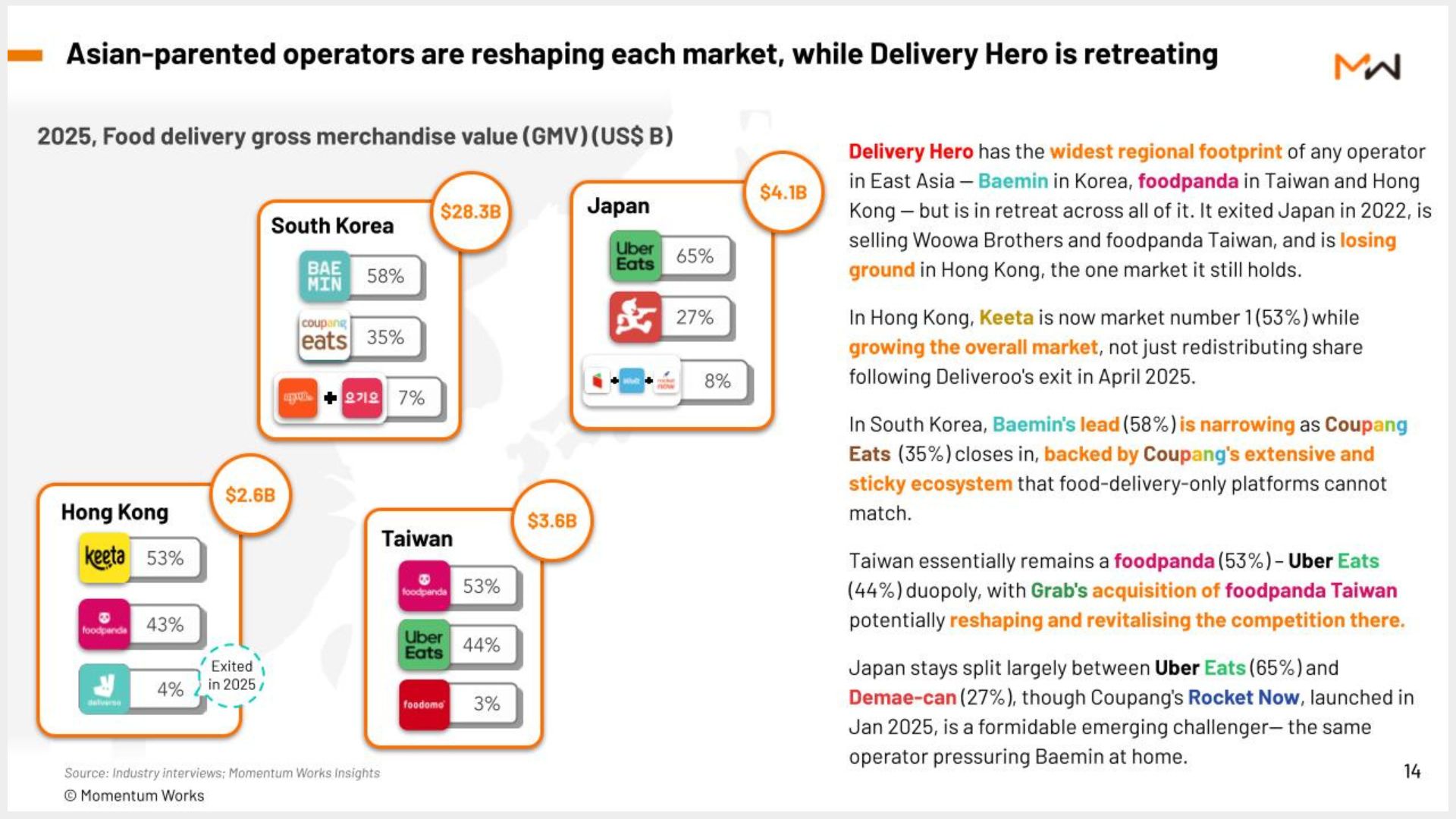

Together, the four East Asian markets generated an estimated US$38.6 billion in food delivery platform GMV in 2025. South Korea alone accounted for US$28.3 billion, or roughly 73% of the total, while Japan, Taiwan and Hong Kong generated US$4.1 billion, US$3.6 billion and US$2.6 billion respectively. - Delivery Hero’s acquisition-led strategy is reaching an inflection point

Delivery Hero once controlled leading platforms across Hong Kong, Taiwan and South Korea while maintaining operations in Japan. Today, much of that footprint is being dismantled. Delivery Hero’s acquisition-led model designed to consolidate markets is increasingly challenged by competitors that continue investing aggressively in growth and operational excellence. - Hong Kong: Keeta rewrote the market

Meituan’s Keeta entered Hong Kong in 2023 with a playbook centred around subsidised one-person meals and rapid network density expansion. Within 29 months it became profitable, overtook foodpanda and fundamentally shifted competition from subsidy spending to operational efficiency. - Taiwan: Grab has the opportunity to reignite market growth

Taiwan has largely remained a profitable but comfortable duopoly for years, with market growth relatively stagnant and penetration hovering around 10%. Grab’s experience competing in Southeast Asia gives it a credible opportunity to re-energise Taiwan’s food delivery market. - South Korea: The world’s third-largest food delivery market faces a new challenger

South Korea’s US$28.3 billion market was built on decades of consumer delivery habits rather than platform creation. While Baemin remains the market leader, Coupang Eats continues to gain share by leveraging Coupang’s broader ecosystem, raising important questions for any future owner of Baemin. - Japan: The toughest market to crack

Despite its wealth, density and sophisticated food ecosystem, Japan’s food delivery penetration remains around 3%. Japan’s extensive convenience store infrastructure and deeply embedded solo-dining culture reduce many of the frictions food delivery solves elsewhere. Coupang’s Rocket Now is testing whether affordable solo delivery can unlock the next phase of growth. - Asian operators are rewriting the industry’s playbook

Unlike the previous generation of global consolidators, today’s Asian operators learned to compete before they learned to expand. Rather than simply acquiring assets, today’s leading Asian operators have developed capabilities through sustained competition in highly contested markets. The report argues this operational experience – around density building, unit economics, customer acquisition and ecosystem integration – is becoming a competitive advantage as these companies expand internationally.

- The four East Asian markets vary greatly in food delivery development

All four East Asian markets are now in motion – in each, a challenger has moved against the status quo. What happens next depends mostly on that challenger. And across all four, the challenger is Asian, and determined to win.

Food Delivery Platforms in East Asia 2026 is now available at US$59.95, in English, Japanese, Korean and Traditional Chinese.

Purchase any one version and you can request complimentary access to the others.

[You can purchase the full report here]