As the fintech players, Afterpay and Affirm (backed by Shopify) have become popular in the capital market, many Southeast Asian fintech players are also getting into this field and want to emulate the Australian and American players’ success.

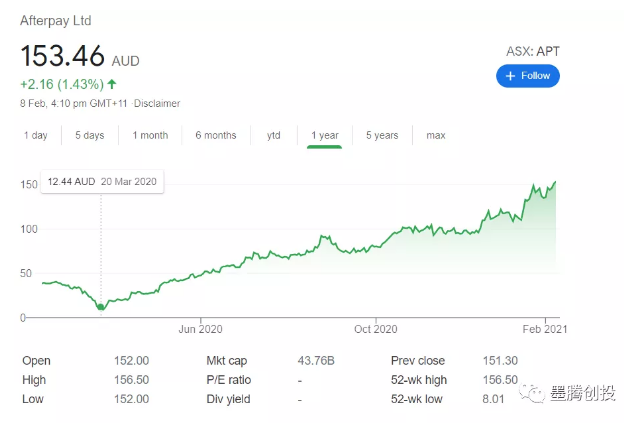

Afterpay, the Australian financial advisor, had a pivotal 2020. It saw Tencent purchased a 5% of its stake in March and April, and in November, it announced an investment of US$10mil into China’s BNPL service provider Happay (The Chinese name means “Watermelon pay”) in Nov 2020 to lay out the Chinese market. Not surprisingly, its’ stock price has soared from A$12 in March 2020 to A$153 in February 2021 – a new time high.

Affirm, the US BNPL service provider took on a different journey in 2020. It partnered with Shopify in July 2020 to ride the surge in online shopping demand bought about by the epidemic. It not only became Shopify’s exclusive installment supplier, but it also achieved significant growth with consumers and merchants using its installment service. It eventually went IPO in Jan 2021 and share price doubled on the first day of trading.

BNPL in Southeast Asia

Fintech lending has always been one of the most active industries in Southeast Asia’s startup ecosystem, and BNPL has always been around. It just wasn’t called BNPL, but installment lending, or “cicilan” in Indonesia.

The key players were Akulaku from China, and Kredivo from Indonesia(founders from india) – both competing for market share in the key battleground – Indonesia. Akulaku received an investment of US$100 million from Ant Financial. On the other hand, Kredivo (the company is called FinAccel) received a US$90 million investment led by South Koreans, with a valuation of $450 million, and it is eager to go public but is hitting some allegedly roadblocks.

We are seeing many cash loan players also moving to consumer installments because, in theory, consumer loans are less risky and have higher user quality and stickiness compared to cash loans. But friends who are familiar with the development of fintech in China should all know-unless you are a big platform such as Ant Financial and Meituan, the risks of consumer loans and cash loans are really the same.

Many BNPL companies have also become popular with the encouragement of Afterpay’s success – in particular, Hoolah, Atome, and Pace.

Hoolah, founded by two former executives from Visa and Worldpay (it is said to be derived from the Chinese “后来”), received tens of millions of dollars in financing from an Australian institution in 2020, targeting the Southeast Asian millennial market and catering to the consumer needs of young people.

Atome, which also wants to power millennial consumers, is the BNPL subsidiary of Advance Intelligence Group after the upgrade of Advance AI invested by Vision capital and GAO RONG capital. Their sister companies include Kredit Pintar, the leading P2P cash loan platform in Indonesia, which focuses on the 2B data risk control business for banks and financial institutions.

Pace, the new kid on the BNPL block – was built by Turochas Fuad (a successful serial Southeast Asia-Indonesian entrepreneur whose credentials include creating a shared office platform and sold it to WeWork) with the support of Vertex Ventures.

Of course, Grab, Gojek, and Tokopedia are also actively paying attention to BNPL. Grab is no stranger to BNPL. As early as 2019, Grab Pay launched similar services to cooperate with Qoo10, 11Street, and other e-commerce players. Consumer loans and installment business are also an important part of Sea group’s financial business relying on Shopee.

Are regulators catching up?

The surge in online shopping demand driven by COVID-19 and some consumers whose income is affected by the epidemic are more inclined to pay in installments. This has a certain role in promoting BNPL, which is interest-free and does not require credit card binding, and is why BNPL has become so popular recently one of the reasons.

Although all BNPL products focus on millennials as a consumer group to expand, they are also a group with relatively low savings rates. In Singapore, nearly 1.1 million people in Singapore have used the BNPL service in 2020. According to a survey conducted by Finder, about 9% of consumers pay late fees for failing to repay in time, and about 27% of consumers say that their financial situation is not good when using BNPL services.

To this note, regulators have announced that they will be “reviewing BNPL regulations” which is a sign that the industry is getting big enough to warrant some sort of supervision.

The Monetary Authority of Singapore also stated on Friday that in the face of many BNPL products, there is still a lack of corresponding supervision. For example, even though BNPL is considered a “loan” to the customer, it is not included in the unsecured 4 times salary credit limit set by the Monetary Authority of Singapore. If consumers accidentally overspend, it will still cause potential financial difficulties for this group.

If BNPL is contributing to overleveraging risk in a country like Singapore where savings rate is high, what’s more, other Southeast Asian countries that are still developing and savings rates are lower.

The intervention by regulators, such as Monetary Authority of Singapore, is positive. Appropriate supervision will contribute to healthy competition in the BNPL market and minimize the problems left over from early rapid growth.

The BNPL’s business model does not have high barriers and is easy to replicate. Current BNPL players do not have any obvious unique advantages – in business-coverage, payment, or security. Existing players can only enhance their competitiveness through continuous expansion, obtaining enough users, and increasing loan balances.

Moreover, competition is not only with other BNPL players. Traditional financial and tech giants are also coming in to fight for market share. For example, UOB launched SmartPay to support customers to convert credit card bills within 6-12 months into interest-free instalments, and only charge a one-time handling fee. Grab, OVO, Gojek, and Shopee that have a good foundation in digital ecology and regional markets.

In fact, the exclusive cooperation between Affirm and Shopify has also pointed the way for many BNPL players. Shopify’s contribution to its user growth and today’s record-high stock price is obvious.

The reason that BNPL is easier to operate in the European and American markets is that there are big ecommerce transactions happening outside the major platforms (e.g. Amazon) and retail demand is quite scattered across the various players. However, in China, BNPL is dominated by large ecommerce platforms such as JD and Alibaba, and the diversity of smaller players is small. Hence, there is not much room for third-party companies to expand.

Southeast Asia is more similar to China than to the US in terms of concentration of e-commerce. As such, we believe that big platforms will dominate BNPL. This is, after all, easier for them, and they are more willing to take profits into their own hands. It will be difficult for BNPL to survive in such a fierce environment for a long time only by relying on its own alone. How to gradually establish its own ecosystem products while expanding is crucial.

For many small and medium-sized platforms, it may be a more reliable choice to grow loan book (to a reasonable size) and find a buyer.