Grab seems to have simplified its strategy – will they execute it well?

Last Tuesday (27 Sept), we published an article comparing the results and cash positions of Grab, GoTo and Shopee. Coincidentally, Grab held its ‘Investor Day” on the same day.

While there were a lot of speakers and slides (you can read the 107-page deck) during the half day event, we thought the following 8 are probably the most useful to give an understanding about what Grab is heading to next:

- Grab’s growth initiatives – they are fairly self explanatory. The company also laid out the evolutionary history of its key products/initiatives:

2. The groceries strategy – nothing new really: still a combination of 1P and 3P, though in their last earnings announcement, it was clear that dark stores were out. From the presentation, it seems that while the company is doing a lot with its Jaya Grocer acquisition in Malaysia, it is quite cautious about expanding this business model in other countries:

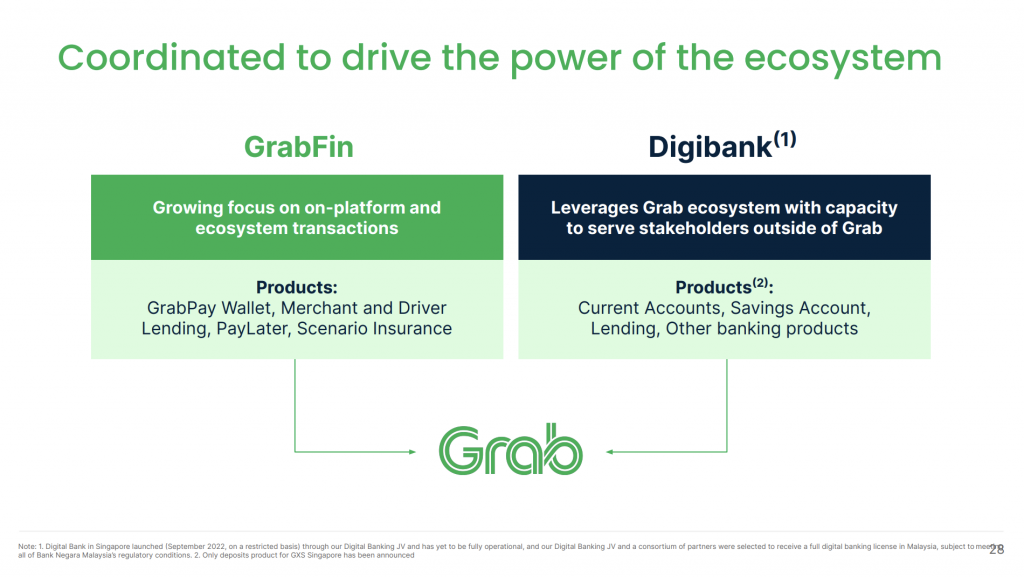

3. The financial services strategy is consolidated as well – which we heard that they had already communicated internally earlier this year. GrabFin and Digibank are the main focus areas – grouping the previous checklist of multiple services. It is also clear that Grab is no longer pushing for payment off the platform (e.g. offline merchants):

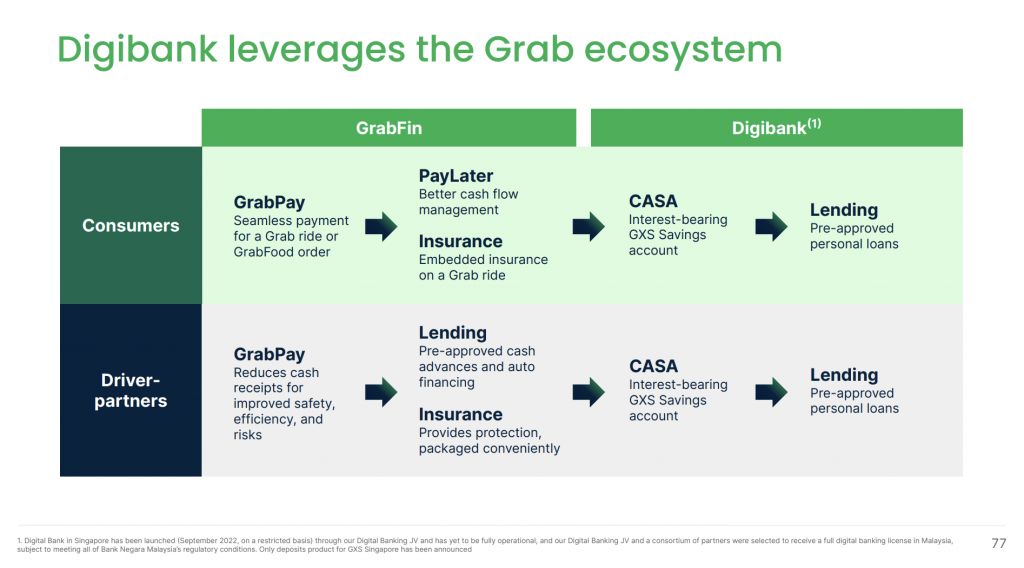

It also gave more details about the strategy for Digibank and how it interacts with GrabFin:

4. The GrabUnlimited loyalty strategy, mentioned above, seems to have some parallel (though differ in pathways and implementation) to how Alipay and Alimama together help drive loyalty and traffic distribution at Alibaba:

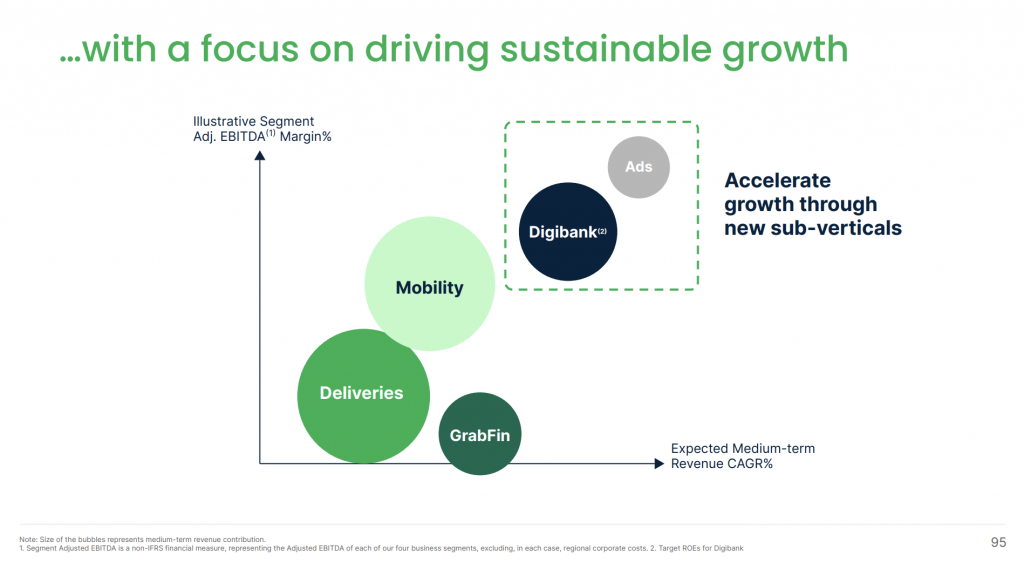

5. The company expects ads and digibank to have the best adjusted EBITDA margin and highest medium term revenue CAGR, though Mobility and Deliveries will remain the largest sectors in terms of revenue:

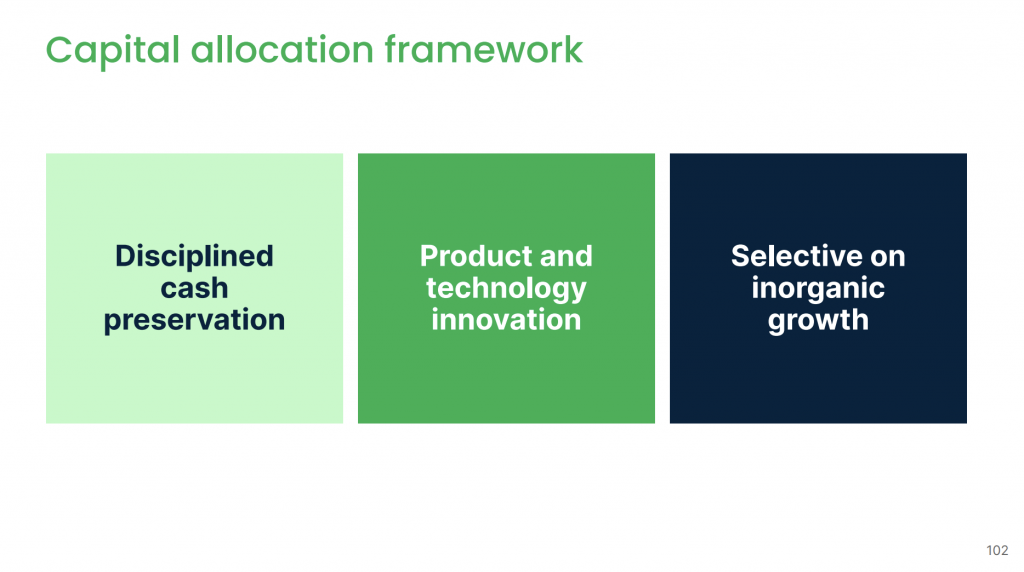

6. Of course, what investors in the current environment care about the most – path to profitability. The interesting part here is that inorganic growth (e.g. acquisitions) is not ruled out, though the company vows to be “selective” on it:

Thoughts:

Grab has probably the best cash position compared to other two peers (SEA Group and GoTo). However, looking at the share price and macro environment – investors probably expect it (as they do with the other two companies) to reach break-even points earlier rather than later.

The strategies laid out here are simplified from previous iterations, especially on deliveries and financial services – however, the key is still relentless execution to drive efficiency in all areas.

Although with 8 quarters worth of cash, Grab is racing against time.