Today, Momentum Works is launching our 4th annual Food delivery platforms in Southeast Asia report.

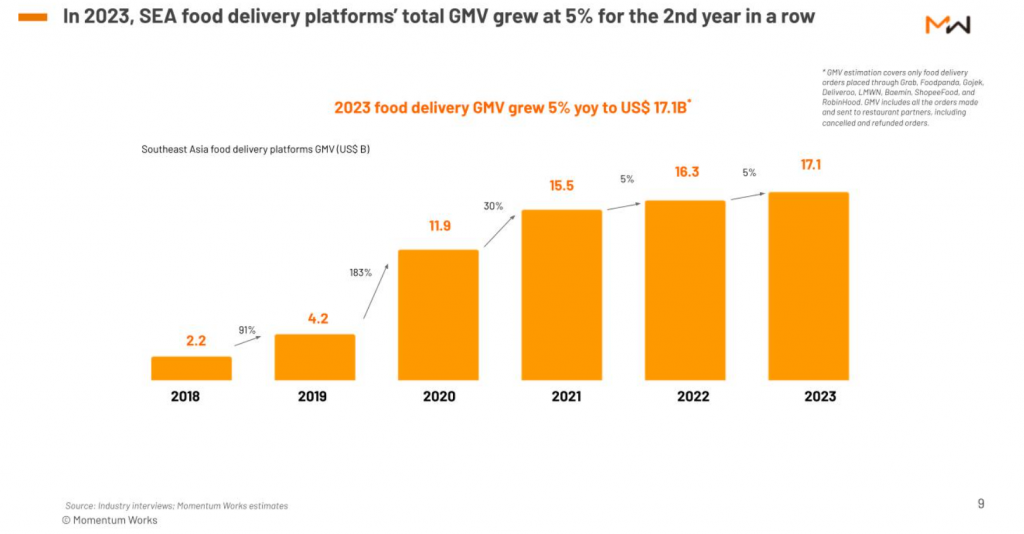

Southeast Asia’s total food delivery platforms GMV grew a modest 5% YoY to reach US$17.1B in 2023, mirroring the growth rate observed in 2022.

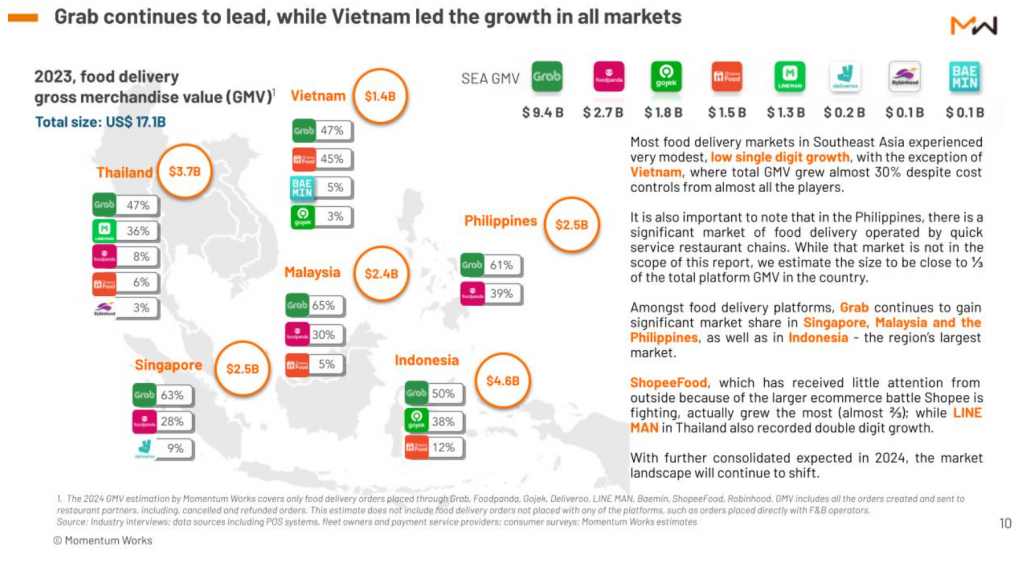

The growth was driven primarily by the region’s smallest food delivery market, Vietnam (+US$0.3B or 27% YoY), followed by Malaysia (+US$0.2B or 9% YOY). Thailand and Indonesia registered low single digit growth, while Singapore’s topline remained flat.

With continuous pressure to achieve sustainable profitability, most incumbent food delivery players have continued to rein in food delivery subsidies and adopt differentiated strategies to compete. As of end 2023, Grab is estimated to account for 55.0% or US$9.4B of the region’s food delivery GMV, a 6.8% increase from the year before. Foodpanda and Gojek are estimated to contribute 15.8% (US$2.7B) and 10.5% (US$1.8B) of the region’s GMV, a 12.9% and 10.0% YoY decline respectively. Shopee and Lineman showed notable growth, and are estimated to contribute 8.8% (US$1.5B) and 8.1% (US$1.4B), respectively, to the region’s GMV.

To better understand the evolving landscape and market dynamics of food delivery platforms in the region, check out our Food Delivery Platforms in Southeast Asia 2024 report. The report is complimentary for a limited period of time.

Some key topics discussed include:

- In 2023, SEA food delivery platforms’ total GMV grew at 5% for the 2nd year in a row to US$17.1 billion

- Grab continues to extend its leadership (55.0% market share), while LINEMAN and ShopeeFood showed notable growth. Across all six major markets, Vietnam grew the most.

- Chinese F&B brands have accelerated their market expansion into Southeast Asia, bringing their methodologies and intensifying the competition in the region

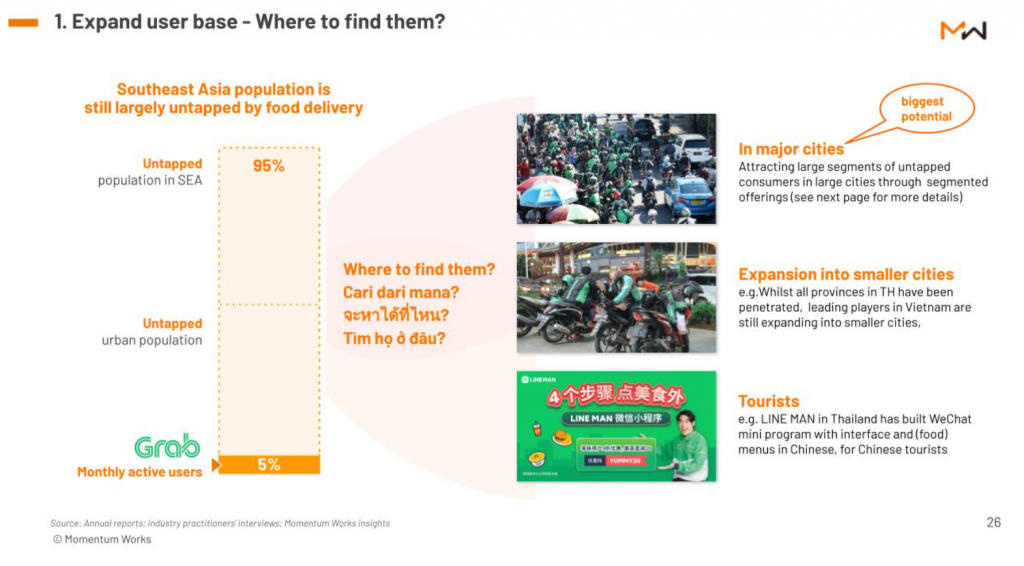

- With only 5% of the region’s population using the largest platform (Grab) on a monthly basis, there are still a lot of untapped market segments. Where are they and how to effectively serve them while maintaining profitability?

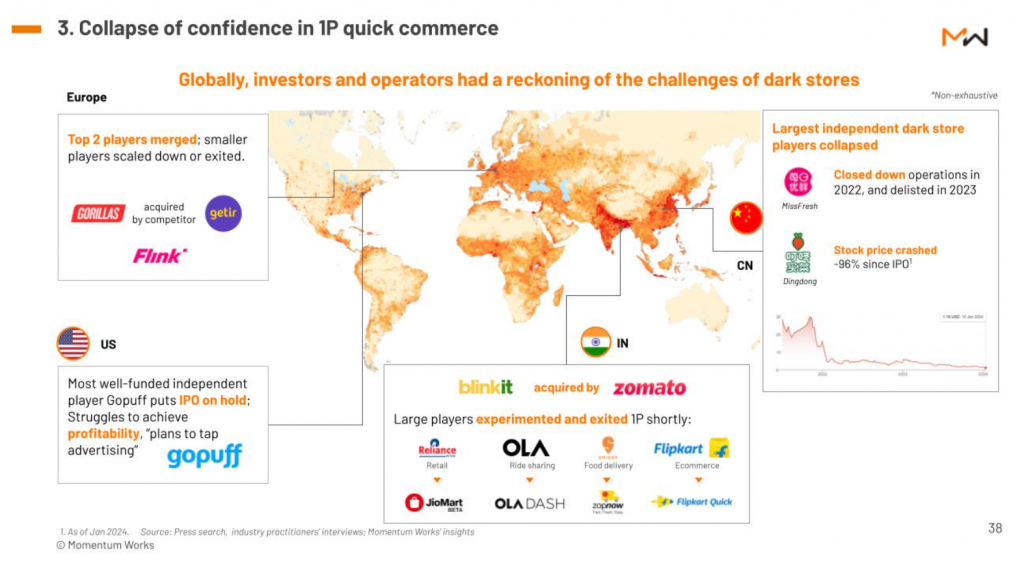

- Across the globe, the confidence by investors and operators on 1P quick commerce has been waning. A few selected players affiliated to large players, however, have found the volume and density to break even: