After years of development, the market has come to a consensus that Southeast Asia’s consumer tech space is now dominated by three publicly listed giants: Grab, GoTo and SEA Group.

The three have overlapping businesses but are not exactly comparable in many dimensions. GoTo’s Gojek competes against Grab in mobility and food delivery; GoTo’s Tokopedia competes against SEA Group’s Shopee; and GoTo Financial competes against both Grab Financial Group and SeaMoney in digital financial services. GoTo largely focuses on Indonesia, while Grab decided to be a regional player, and SEA Group has aspirations to be global.

Recently, Shopee and its parent company Sea Group have been under a lot of negative publicity, primarily due to a succession of cost cutting measures including rescinding job offers, closing markets and layoffs. The focus now is “self sufficiency”, which echoes a message of “path to profitability” that Grab has been emphasizing since Q4 2019.

In the current challenging macro environment, how do these companies fare against each other? Since all three have released their Q2 2022 earnings with a slew of numbers and metrics, we thought of making simple comparisons on some important numbers:

Apple to Apple

To make effective comparisons, we need to first make sure we are comparing apple to apple. The three companies use very different terms in their reporting – this can make intuitive comparison obscure.

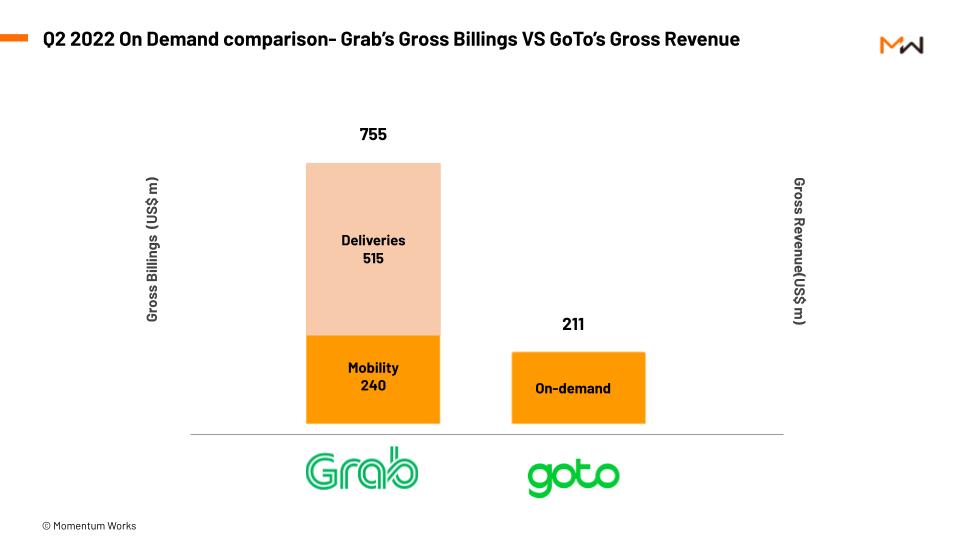

For example, GoTo reports ‘gross revenue’ for on demand, while Grab reports ‘GMV’, ‘commission rate’ and ‘revenue’. Which metric of Grab is exactly comparable to the ‘gross revenue’?

Well, Grab used to report “gross billings”, which is “GMV” times “commission rate” – that is the apple to apple comparison with on demand “gross revenue” of GoTo.

Platform GMV

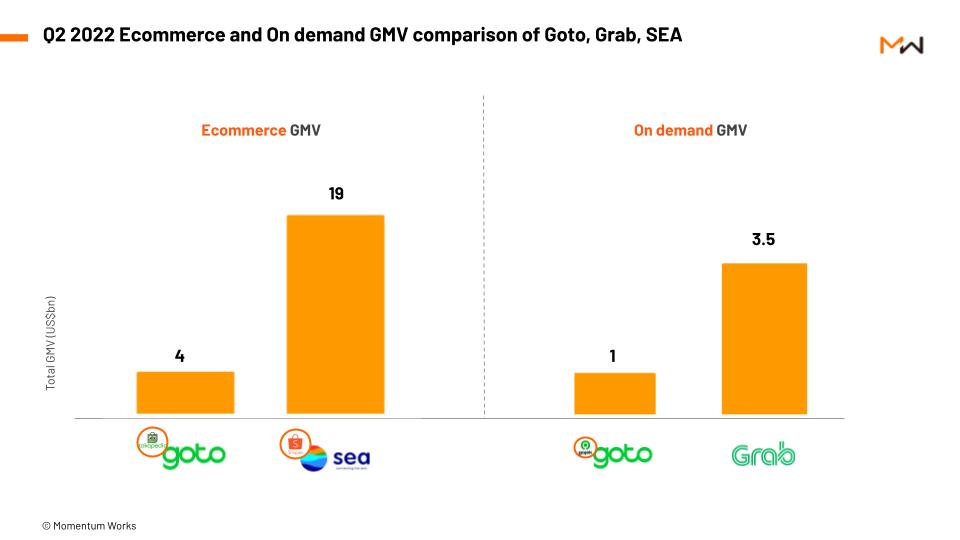

Many people do not like the metric of GMV, saying that it is often, if not always, inflated. However, we assume that GMV (or GTV) is measured in comparative ways, and ignore the accounting treatments of new/minor segments (such as Shopee’s food delivery business).

As we can see, Grab’s quarterly on demand GMV is about 3.5X that of GoJek, while Shopee’s ecommerce GMV is 4.75X that of Tokopedia. Analysts typically assume ⅓ of Grab’s business is in Indonesia, while Shopee has also Taiwan, Poland and Latin American markets – the ratio seems to be about right.

Ecommerce take rate

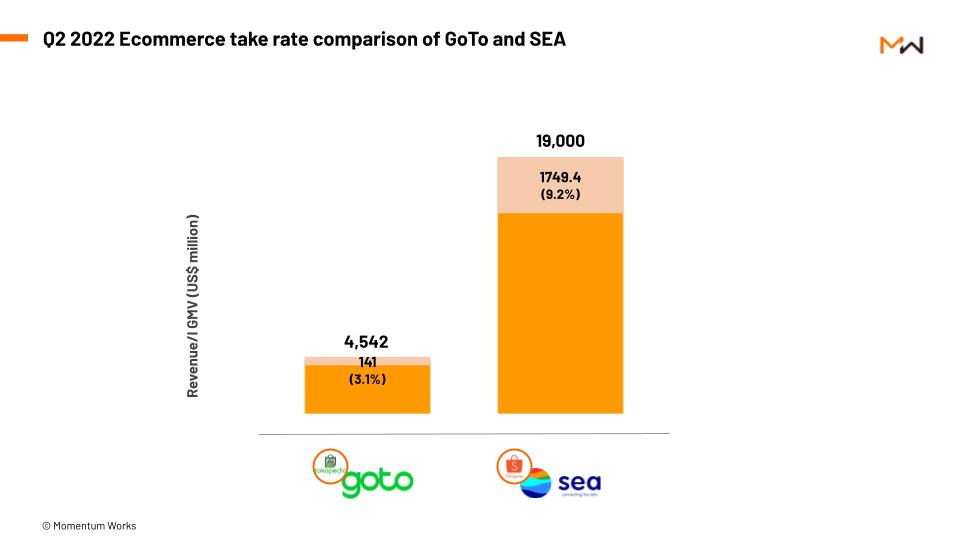

Tokopedia has upgraded the commission scheme for C2C merchants, which effectively raised take rates (revenue/GMV) from 2.4% to 3.1%. This nominally inches closer to Alibaba’s about 4% in China, but is still way behind Shopee’s 9.2%.

Logistic fleets we have spoken to indicate that Tokopedia’s parcel volume has barely grown in the last year, suggesting the growth of GMV is possibly contributed mainly by virtual goods and services, which are lower margin in nature.

Shopee is taking extraordinary measures to reach profitability sooner rather than later – on the ground sources told us that marketing spend has been reduced as well in recent weeks. The question is whether it can still grow or reach segment profitability when incentives are removed.

A large part of those incentives are in logistics – we know that Shopee has taken measures to reduce the logistic cost, and having its own Shopee Express increases the bargaining powers before third party logistics providers. An issue is that TikTok, which has expanded its ecommerce operations beyond Indonesia into all major markets of Southeast Asia, might wish to continue to subsidize logistics to grab market share.

Financial services

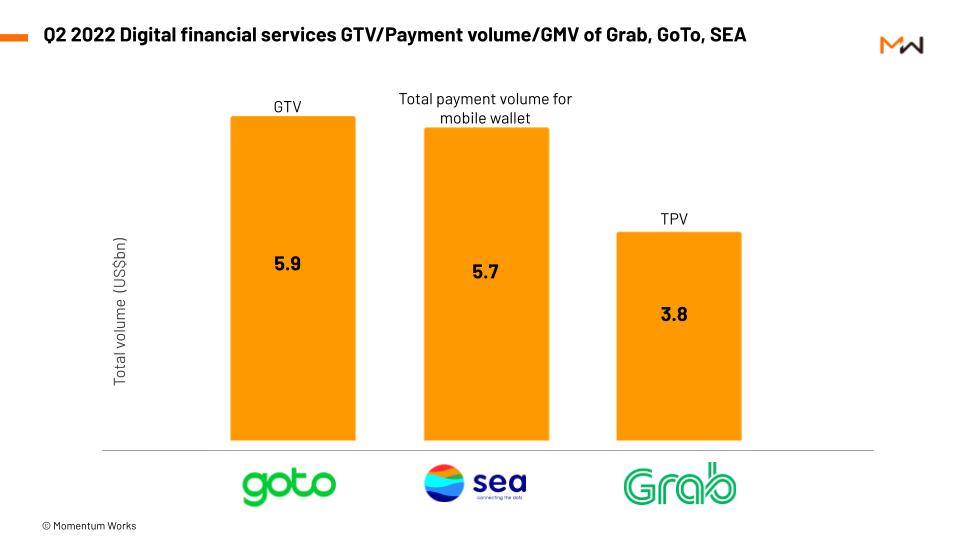

Amongst all three companies, GoTo seems to process the most payment value, reported as the GTV for GoTo Financial. In addition to GoPay, an e-wallet and digital payment service created by GoJek, GoTo also owns Midtrans, one of the largest payment gateways in Indonesia. The fintech take rate reported by GoTo is about 0.5%, which is in between the net revenue margin of Xendit (a major alternative to Midtrans) and the merchant rate charged by GoPay. Grab reported a commission rate of 2.7% for financial services, on the other hand.

None of the companies explicitly highlight the fintech lending volume in their reports. It is, however, noticeable on SEA’s Balance Sheet (by 30 June 2022) that its short term loan receivable (net allowance for credit loss) has grown from US$1.5 billion (half a year ago) to about US$2 billion.

This is probably the combined loans issued from the balance sheet of SeaMoney Group as well as SeaBank in Indonesia. We understand that banks like DBS also fund co-lending programmers together with SeaMoney, which means the actual loan balance of SeaMoney is more than US$2 billion.

On GoTo, we can probably take a look at Bank Jago as a proxy. The bank, which counts GoTo as a major shareholder and provides capital for GoTo’s lending business, recorded US$330 million loan balance as of 30 June 2022, growing from US$221 million half a year ago.

How long can each company survive?

Another key question is how much can these three companies sustain their operations without additional fundraising – raising which can be very difficult in the current capital environment.

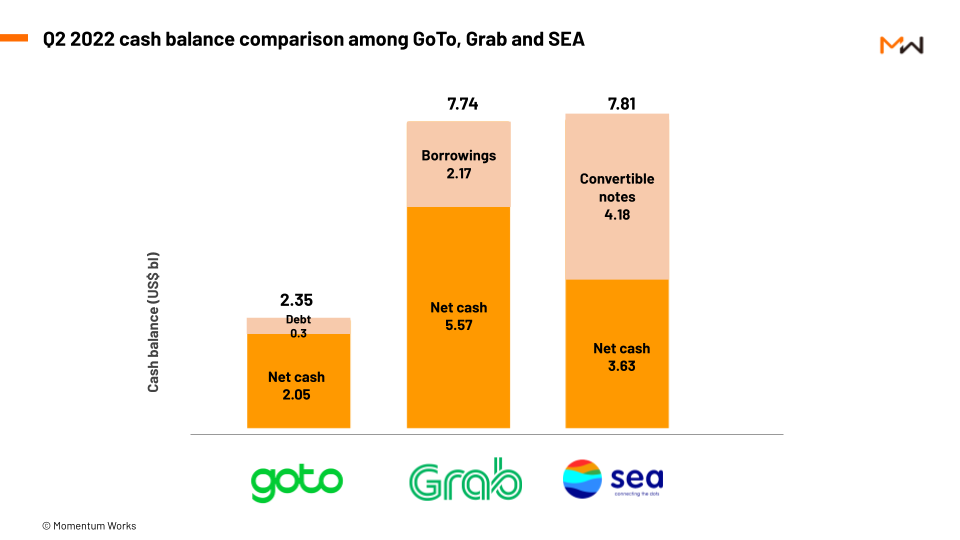

Grab’s net cash is at US$5.572 billion – cash liquidity of US$7.74 billion minus borrowings of US$2.168 billion. At the Q2 2022 rate of cash burn, it can last for about 4 years without additional cash raise – ample time for it to achieve self sufficiency.

SEA Group, on the other hand, reports cash/cash equivalents/restricted cash to be US$7.81 billion in total (without counting the $2 billion loan receives for sure), It has US$2.8 billion of net property and equipment, and US$2.65 billion of short and long term investments – some of this can be converted into cash, though probably not very quickly.

What is notable is SEA’s US$4.18 billion worth of convertible notes. The only issue of concern is the tranch issued in 2020 which is due in 2025, with a convertible price at about US$90.4. SEA Group will need to make sure it pushes its share prices above that level, or reserve enough liquidity for possible redemption.

At the current burn level, the cash can last about 3.5 years. SEA Group is undertaking drastic cost cutting measures, the result of which will probably start to show in Q4 2022.

The weakest cash position amongst the trio is GoTo, which has a cash balance of US$2.35 billion. At the current level of burn, this cash position can last for 6 quarters, or 1.5 years. At the elevated valuation GoTo enjoys now, it is harder to raise additional money from private investors as compared to Grab and SeaGroup. A US listing within that time period is also highly uncertain – with many predicting the current rate hike cycle to last for 12-18 months at least.

Under these circumstances, GoTo probably will need a state bailout to remain a going concern, while addressing the profitability issue aggressively.