Southeast Asia Tech Investment - 2021 H1

The first half of 2021 has been an exuberant period for many aspects of Southeast Asia tech investment. Even as COVID-19 cases reached a record high and many countries went into a prolonged economic lockdown, the region tech scene continued to break a number of new records.

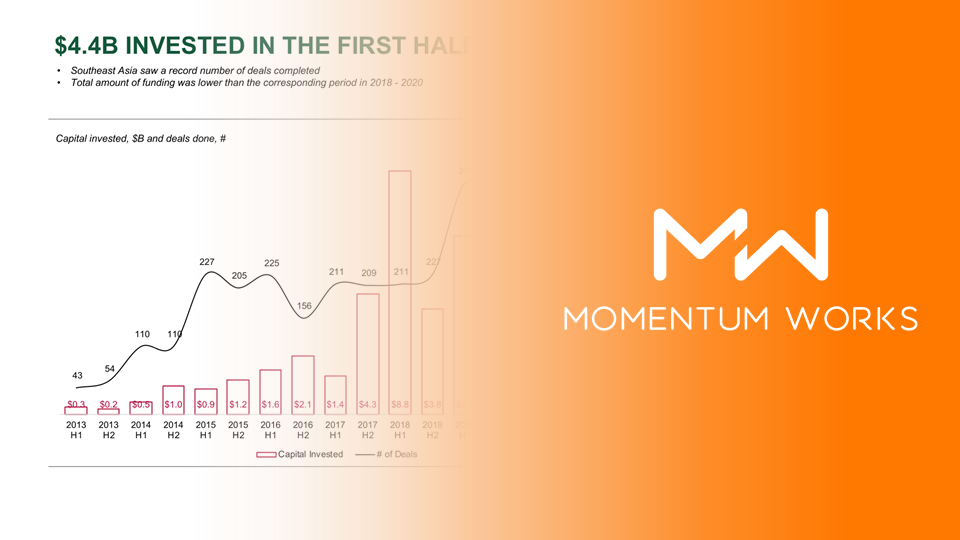

Record number of deals in H1, but total amount invested fell

H1 2021 has seen a surge in the number of deals. We tracked 393 investments across the region in the first half, exceeding the previous high of 375 in H1 2019, and well ahead of the 327 last year.

Deal sizes and valuations rise

Deal sizes and valuations at each of the early funding stages have remained remarkably stable over recent years. In H1 2021, we saw a sharp upturn in both. Median round sizes rose, with Pre-A rounds of $0.8M, Series A rounds of $4.3M, and Series B of $10M.

Indonesia and Singapore still attract most capital

H1 2021 was entirely typical in terms of the geographic distribution of deals. 51% of capital was invested in Indonesian startups, and Indonesia and Singapore startups combined accounted for 70% of the total number of deals done. There was also an increase in activity in the Philippines.

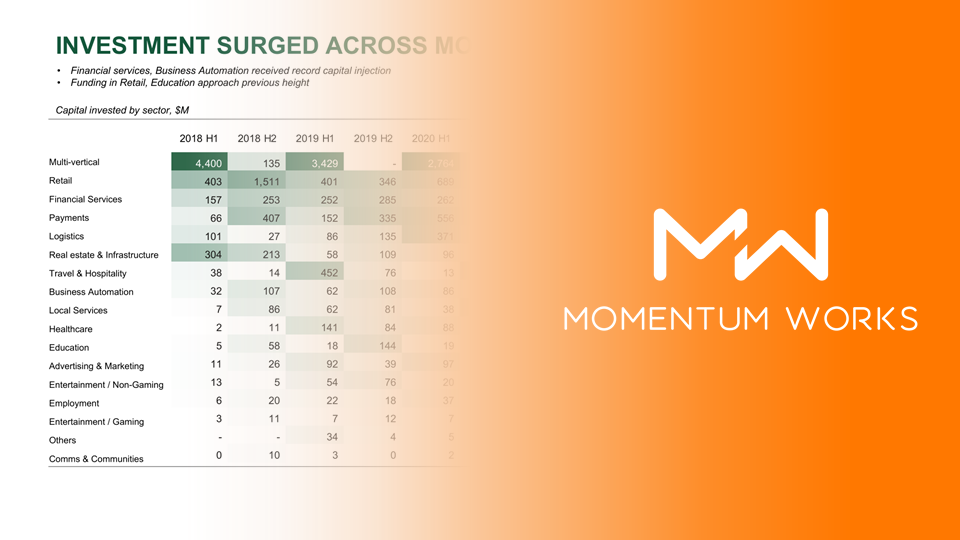

Sector diversification continues

More narrowly focused digital retailers collected over $1.1B in investment, nearly double that of H1 2020. Fintech startups saw a similar amount of capital inflows, in that case about four times the volume of H1 2020. Fintech appears to be the sector of investor focus at the moment.

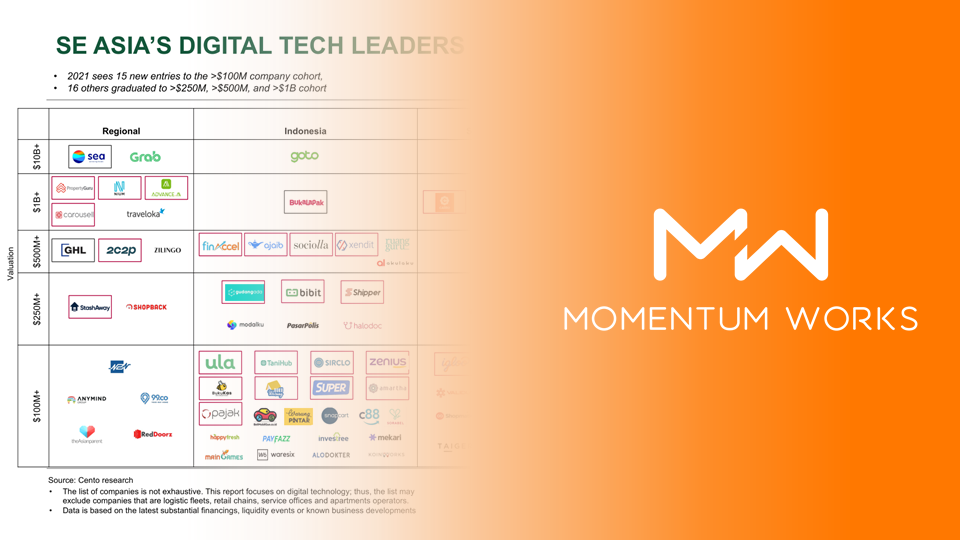

New unicorns

H1 2021 saw PropertyGuru, Nium, Carro added to Southeast Asia’s companies valued at over $1B. While relevant press announcements did not make it to a strictly defined H1 timeframe, we now know $1B+ valuations were being finalized for companies such as Carsome, Carousell, Xendit, VN Life, and Advance – thus, considered them as $1B+ companies, although some of the announcements came in Q3.

IPOs appear

In a first for the region, IPOs accounted for more than 50% of liquidity. While this was the product of one IPO carried out by CTOS (ctosdigital.com) in Malaysia, it may signal the start of an interesting trend.

Looking forward

The profile of other exits in H1 2021 seems to follow the rather subdued trend noted in our 2020 report. We continue to assume that some larger potential deals have been delayed and that we will see some pick up in trade sales in the second half of the year.

4.0")