In Momentum Works’, “Foundational Stages of Digital Lending in Southeast Asia” report, we analyzed Southeast Asia’s digital lending landscape. The report provides a broad overview of the fintech infrastructure in Southeast Asia, the accelerators of growth, as well as the challenges ahead. Furthermore, it presents opportunities the region possesses in terms of digital lending as well as a brief comparison between the different players.

Key insights from the report includes:

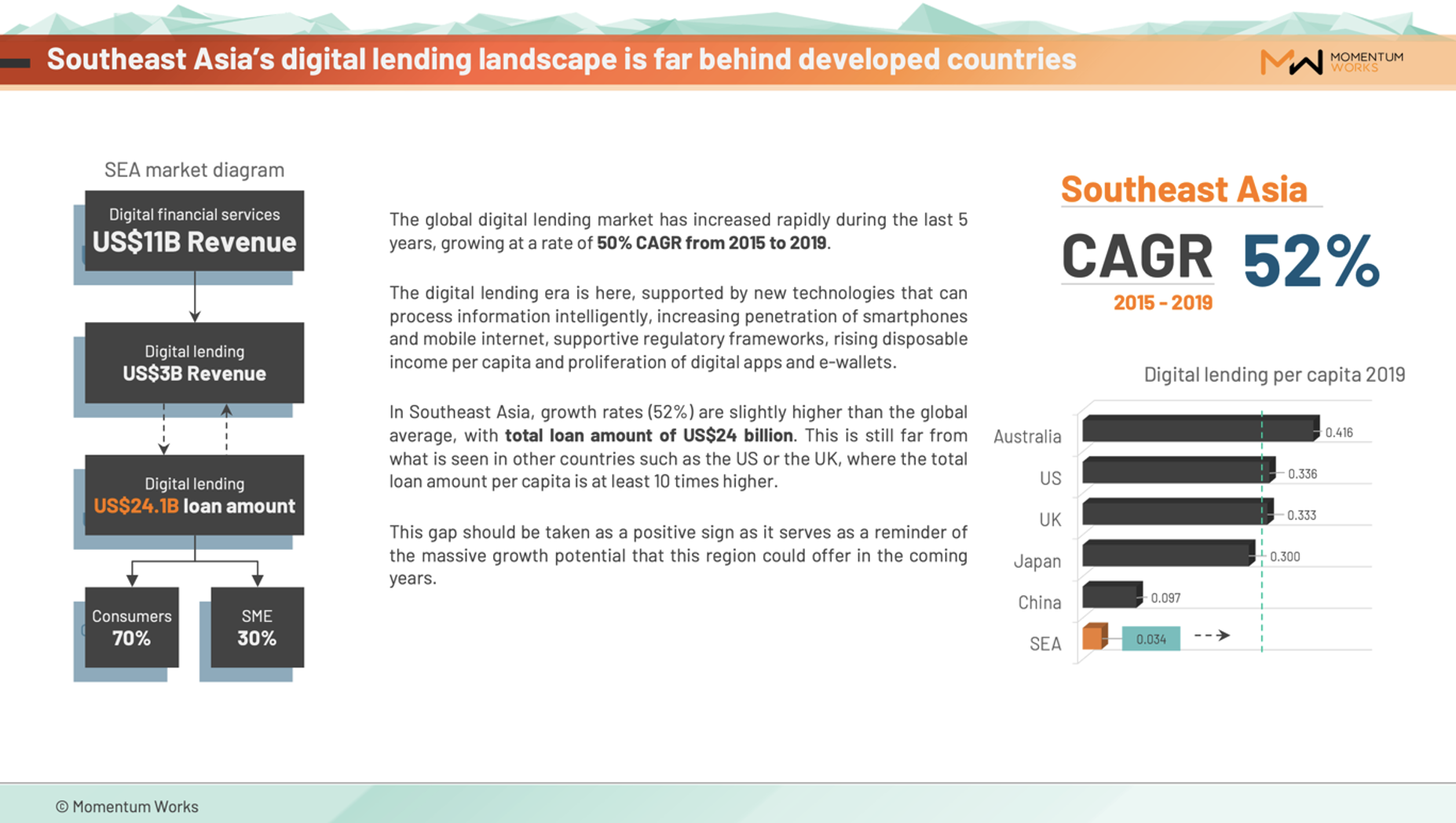

1.Southeast Asia’s digital lending landscape is far behind developed countries.

Based on our estimates, the CAGR for digital lending in Southeast Asia (52%) is slightly higher than the global growth rate of 50%. However, the loan amount (US$24 billion) is far from what we see in developed nations like the US or UK which are about 10 times higher.

Based on our estimates, the CAGR for digital lending in Southeast Asia (52%) is slightly higher than the global growth rate of 50%. However, the loan amount (US$24 billion) is far from what we see in developed nations like the US or UK which are about 10 times higher.

Apart from Singapore, countries in SEA have a very low level of digital lending. Nonetheless, Momentum Works is optimistic about the growth potential of the region, especially in the fintech field.

“A market’s credit system reaches an inflection point once the GDP per capita reaches US$4,000. This region is now fast approaching that turning point and fintech will consequently start to take off” Co founder of SuperAtom Scarlett Xiao said.

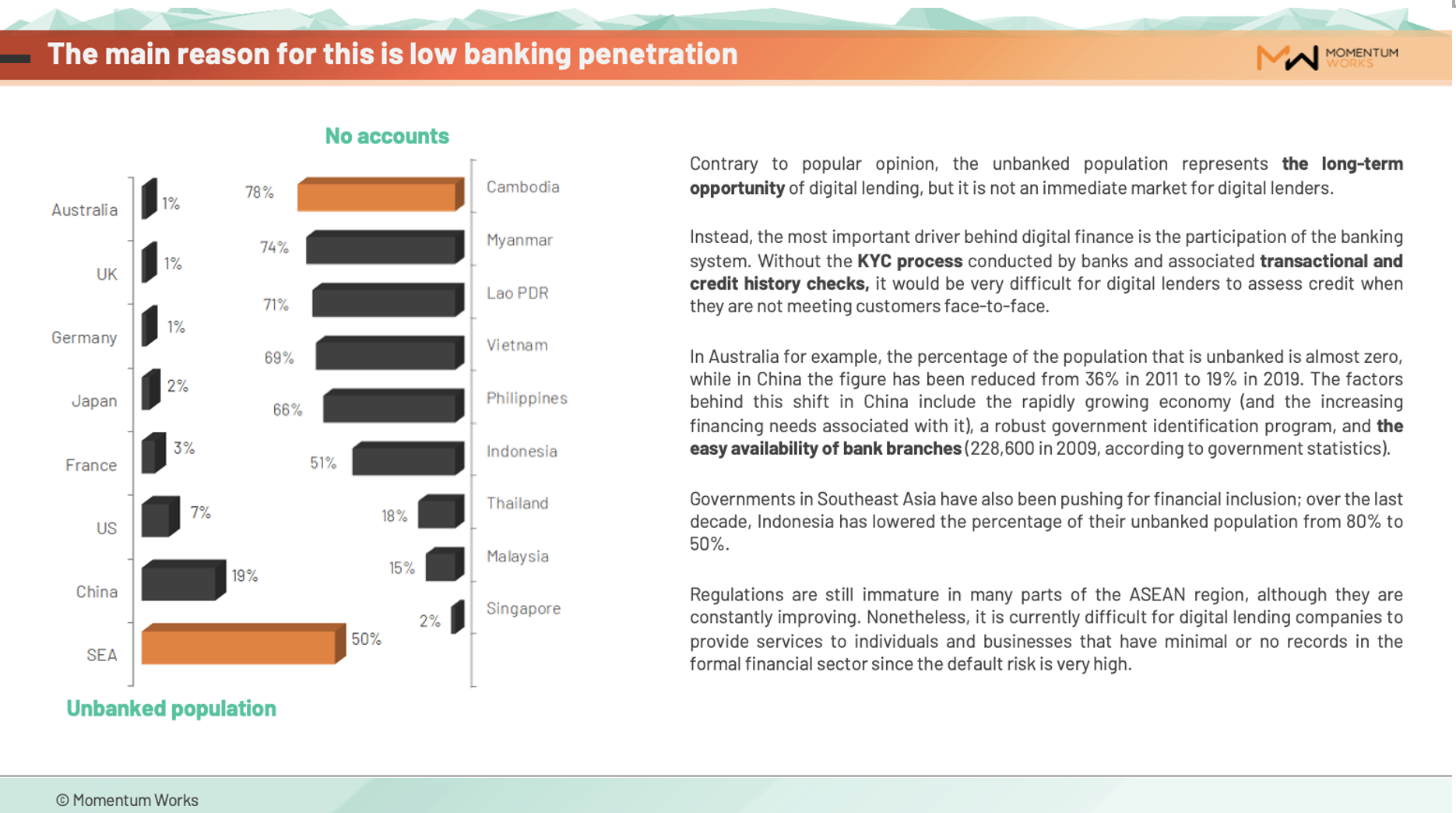

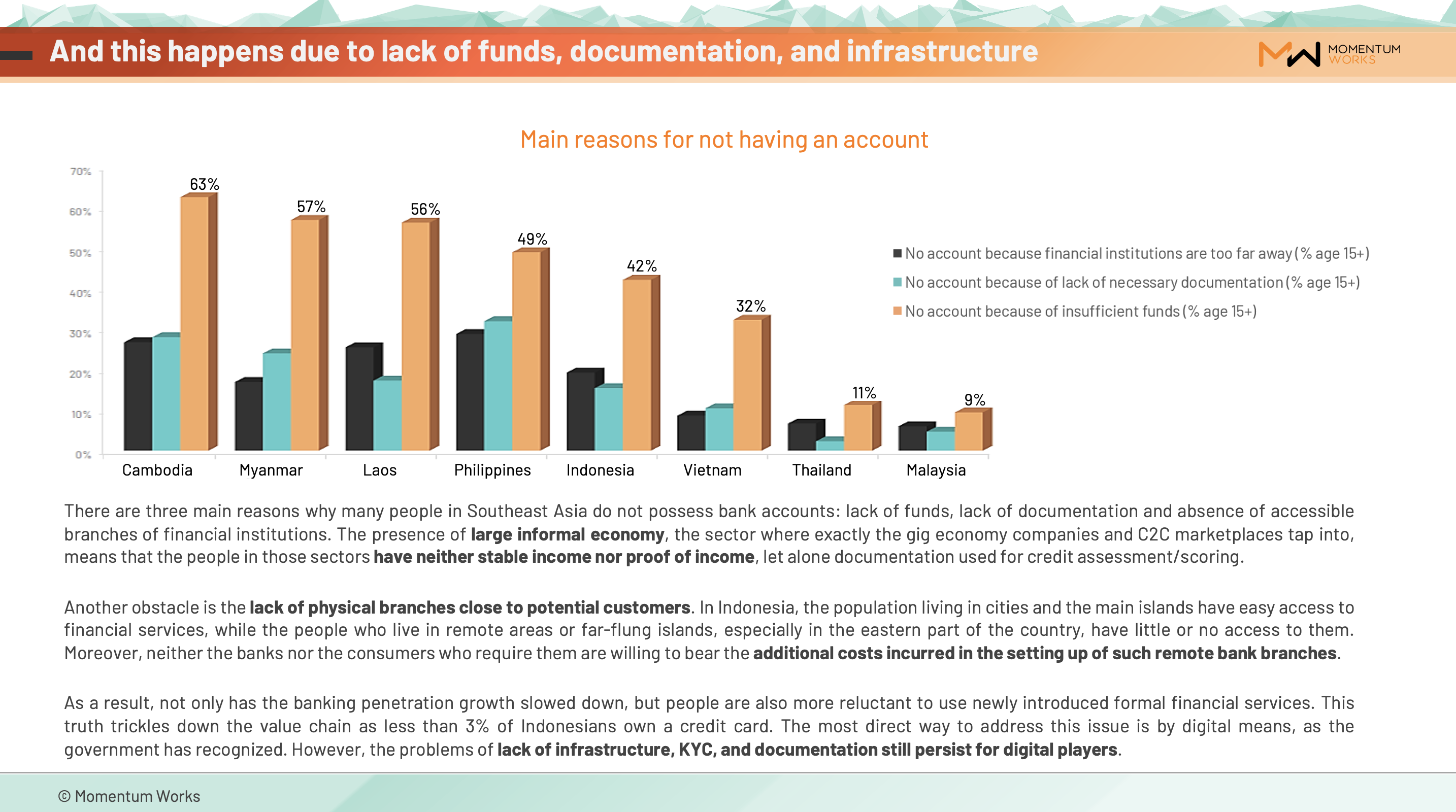

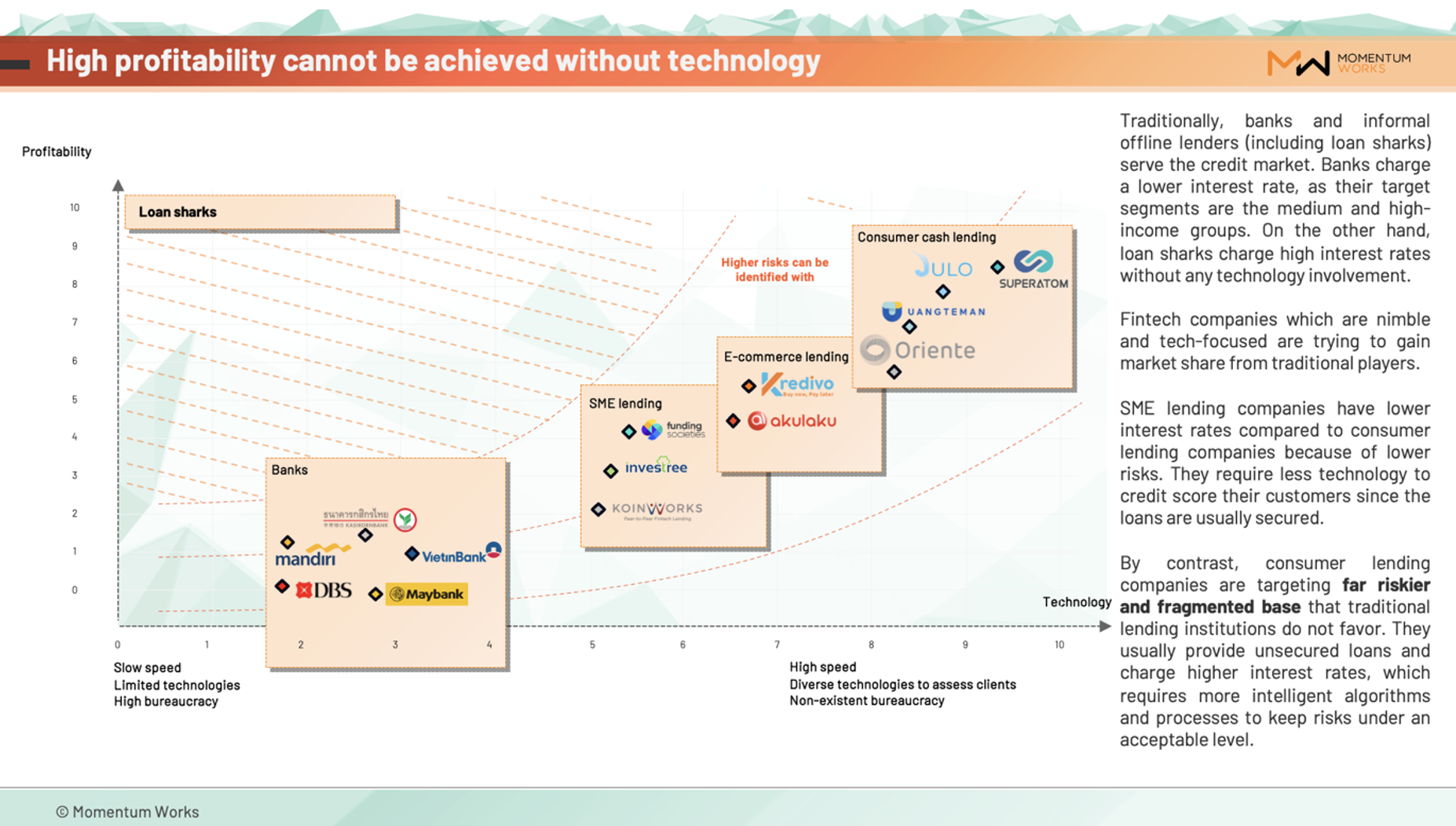

2. The reason for low digital lending can be low banking penetration, lack of funds and infrastructure etc.

A high proportion of unbanked population poses significant challenges to the growth of digital lending. However, this could also represent the long-term growth opportunities for strategic players. The first step to financial inclusion is first having a traditional banking system, and to many of the developing regions of Southeast asia, the foundation is not even done yet.

Evidently, the main reason why there is such a high proportion of unbanked population is the lack of sufficient funds for saving. This coincides with the low GDP per capita of these countries and the presence of a large informal economy – where people in these sectors does not have a stable income nor proof of income. This is a significant challenge for digital lending as it limits credibility due to the absence of documentation, which in turn hinders companies from ‘credit scoring’.

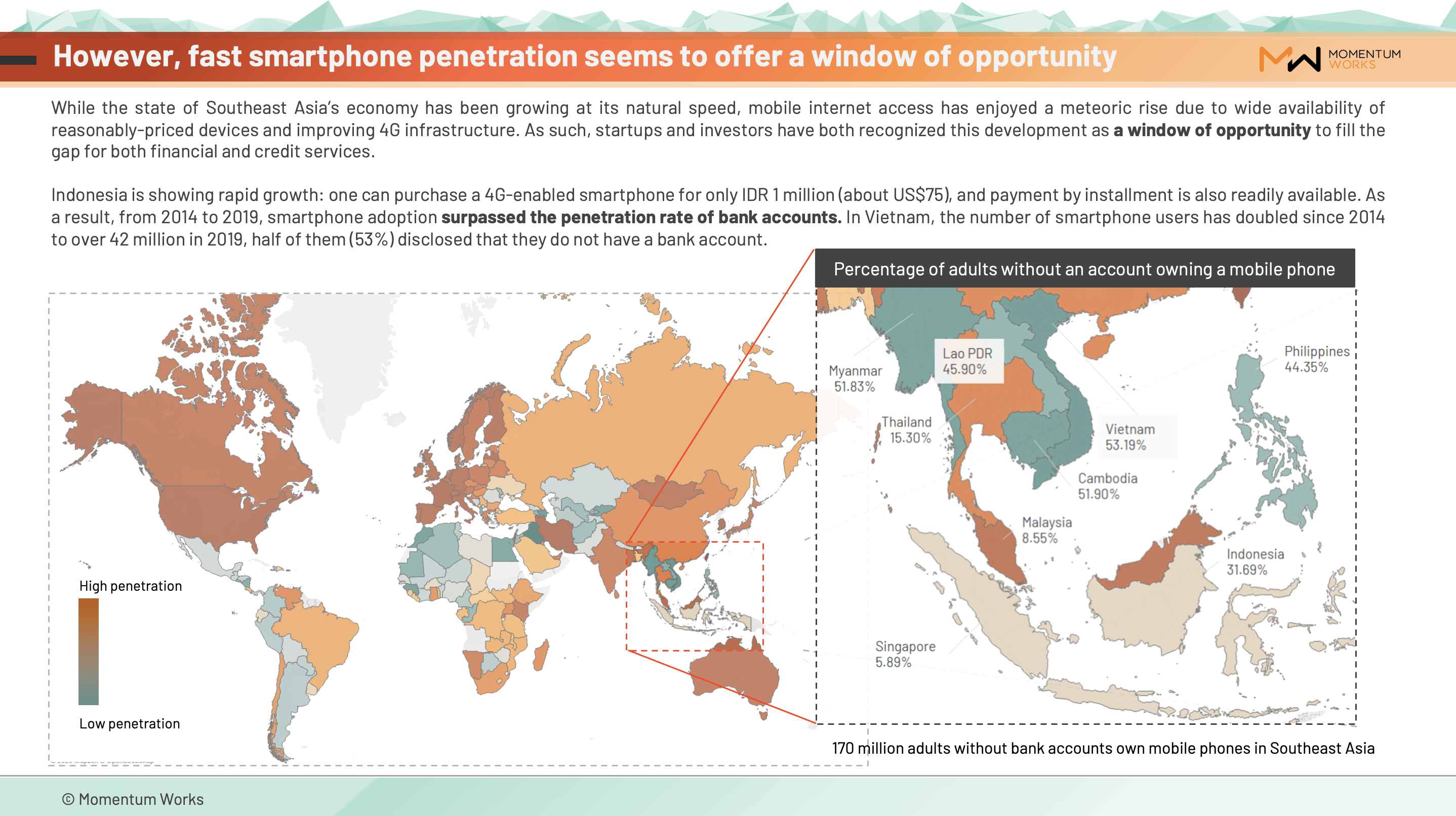

3. Good news is, fintech players are still emerging from this region

Even though banking penetration remains low, smartphone penetration is rather high in the region, attributed to the low prices of smartphones and improving network infrastructure.

The development of smartphone-related infrastructure such as 4G offers a window of opportunity narrowing the gap for financial services. This allows for easy access to digital lending at the tip of their fingers, although a certain level of effort may be needed to gain the trust of users.

4. An analysis of current fintech players

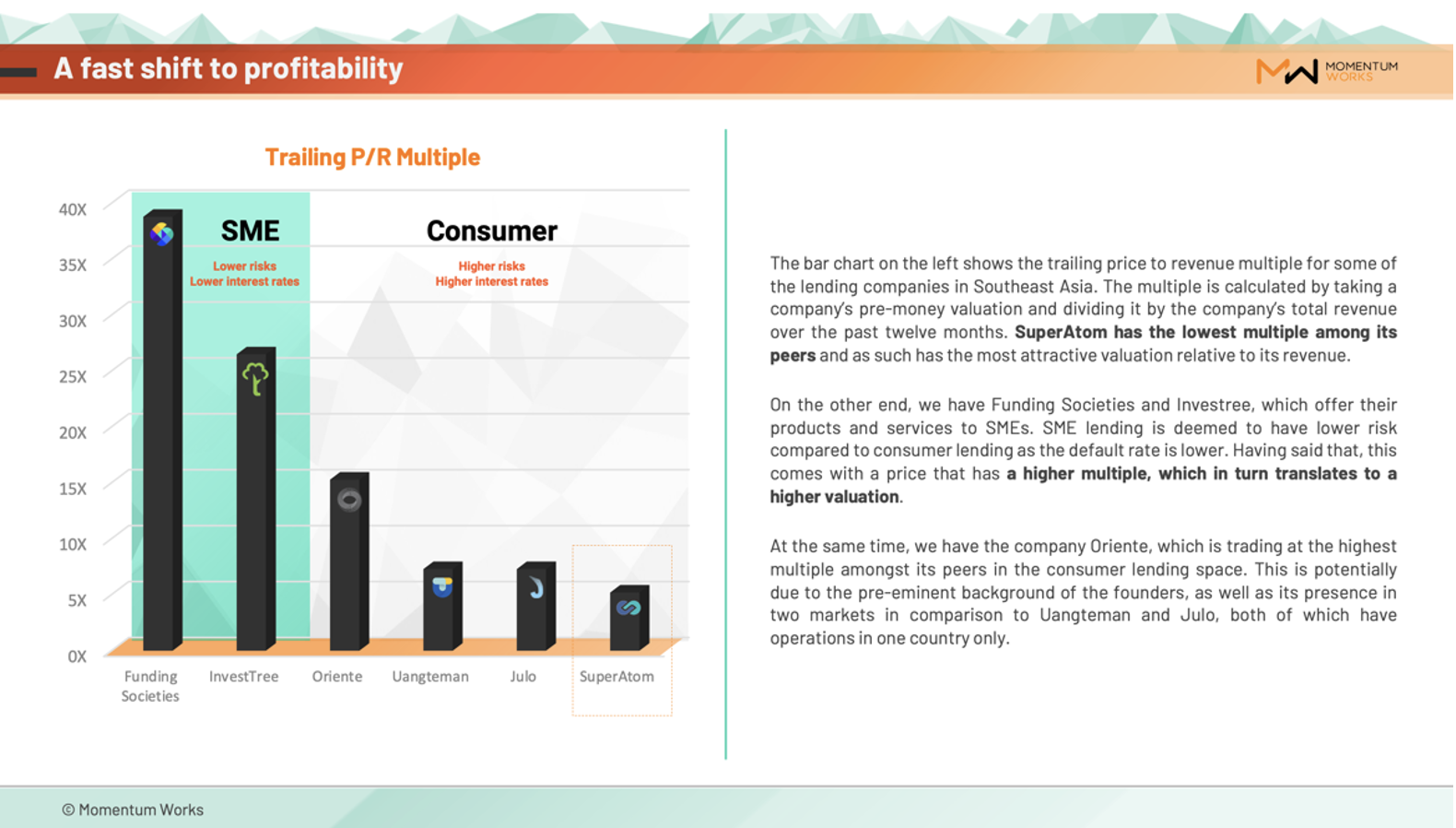

The Digital lending scene in Southeast Asia comprises of both B2B and B2C players. B2B players include Funding Societies and InvestTree who offer lending services to SMEs. Among B2C players, SuperAtom has the most attractive valuation relative to its revenue.

5. High profitability for the fintech sectors

Even though fintech startups have a long way to go before being on par with the major banks in the region in terms of providing financial services, the high margins and extra mobility fintech startups possess in employing technology can put them at an advantage.

In conclusion

The digital lending landscape in Southeast Asia is still largely immature. Having said that, the high rate of growth of the region as well as the fast adoption of technology such as smartphones shows a rising potential of growth and progress for the region. There are different strategies taken by fintech players in the digital lending business, and they will all need a clear value proposition in order to succeed.

To gain a better understanding of the digital lending ecosystem in SEA, get your hands on a copy of this report in this page. Email to us at [email protected] if you have any questions.