aCommerce was once the big brother of e-commerce enablers. Founded in Thailand in 2013, it was set up with the aim of providing support to its clients to sell their brands successfully online.

Back then, as e-commerce was taking off in Southeast Asia, major bottlenecks became more apparent like logistics and lack of fulfilment centres. aCommerce’s parent investor Ardent Capital seized the opportunity and brought their experience and skill set to launch aCommerce’s end-to-end enabler services. They built their own delivery and warehouse systems and catered to various ancillary services like digital marketing, software development, customer care, etc.

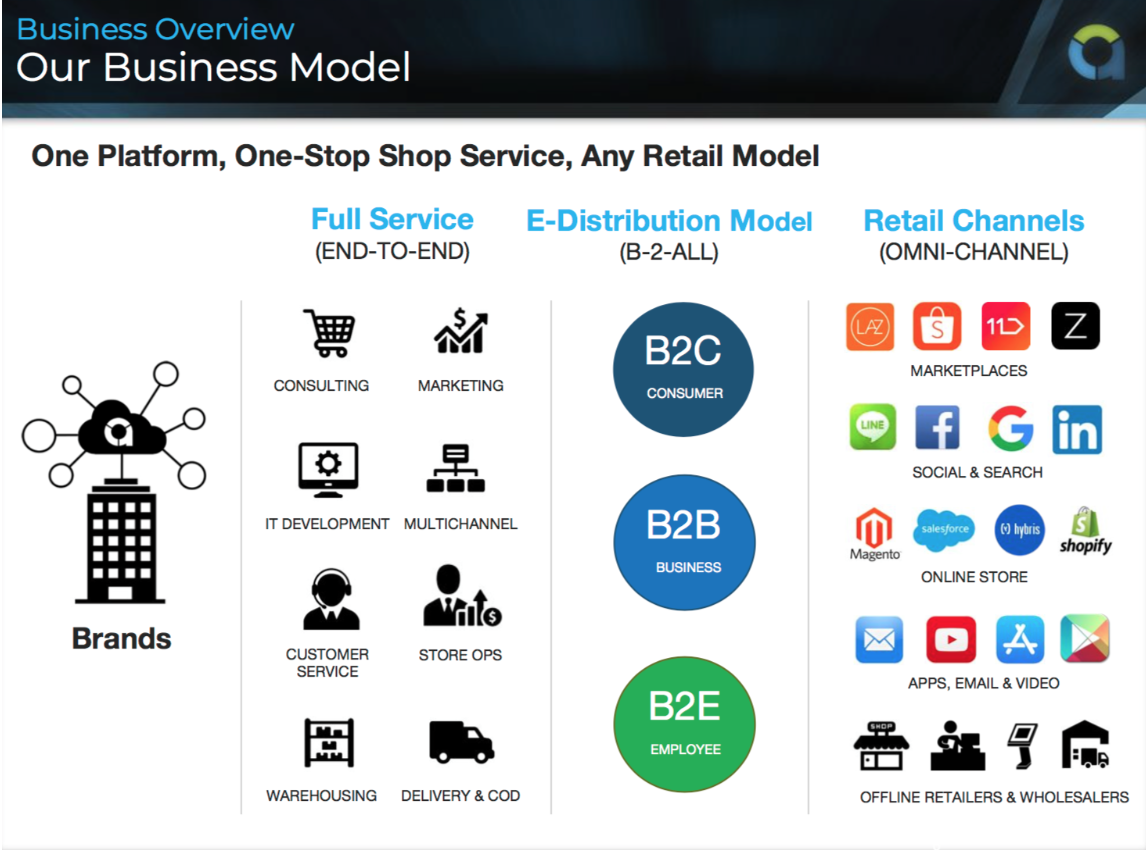

The strategy is to be a one-stop service for brands and to invest more in every aspect of the e-commerce journey to serve them end-to-end.

Over the years, aCommerce has grown its foothold in Southeast Asia and is regarded as the leading e-commerce enabler in the region. Today, it operates across five markets namely, Thailand, Indonesia, the Philippines, Malaysia, and Singapore.

Up until now, aCommerce has raised around $100M with the majority coming from a latest $65M series B round led by KKR owned Emerald Media.

It also has investments from industry leaders such as BlueSky private equity, DKSH logistics and distributors, Inspire Ventures, NTT Docomo, and Indonesian conglomerate Sinarmas.

Last year, they also announced plans for an IPO in 2020 with its eyes set on either the Singapore or Thailand Stock Exchange.

Sounds good, right?

Well, if you ask us, not all appears to be well underneath and there are a few telltale signs.

Mass exodus of talent

Hushed word on the street is that top lieutenants and members of the early founding team have mostly left. The Indonesian team saw four CEOs shuffle around and leave in quick succession in the span of 4 years. They haven’t been able to retain top management from various departments, including regional teams.

The slew of top-level turnovers obviously begs the question – are there deeper issues brewing within the company? One can never get straight answers and they will vary depending on who you ask but it’s an issue aCommerce seems to be grappling with.

Could it be a change in strategy and direction? We discuss this next.

Shift from an e-commerce enabler to an e-distributor

When aCommerce was founded, it was set up as an e-commerce enabler. However, the company then shifted from being an e-commerce enabler to what many describe as an e-distributor, where they buy products from brands to sell (mostly, online).

So with this, they don’t just provide services to brands but hold an inventory of different products.

Why this change in direction? The obvious motivation is to diversify its business model and increase revenue streams. CEO Paul Sriworakul said the company was seeking a $550 million dollar valuation in 2019. So bottom lines will matter. For aCommerce, working directly with brands increases profit margins and eliminates distributors who hold a bargaining power. For the brands, they get the benefit of working with a single platform that provides end-to-end service and reaches customers through various different sales channels that aCommerce can tap into – social media, websites, marketplaces. aCommerce also lets the brands have ownership and access to sales/performance data (which marketplaces usually don’t).

However, e-distribution comes with its own set of challenges for the enablers. The biggest being – unsold stock.

E-commerce is a fast moving business and companies need to match their inventory closely to sales. And aCommerce is apparently struggling with an expanding list of unsold goods. This could mean anything from poor inventory management, ineffective marketing leading to a drop in sales.

Could this have led to declining revenues and the inability to free up more capital to expand further?

Are e-commerce marketplaces a threat to enablers?

Existing big marketplaces like Lazada openly encourage 3rd party service providers to come on board as Lazada Partners (LP).

How does this help brands? Well, without these partners, the marketplace on its own only helps brands set up a store and provides some basic help with marketing and some data on their performance.

Now with these 3rd party partners, brands can get help on everything from strategy planning, brand positioning, logistics, customs, store operation, digital marketing, order fulfilment, customer service, etc. Brands can choose these services on the platform to manage their entire e-commerce journey or just a part of their operations. So basically what e-commerce enablers do.

This begs the question- when brands can sign up to be on these major marketplaces, leverage their large consumer base, huge promotions, and avail a range of 3rd party services why would they turn to e-commerce enablers? Are the complete experiences offered by big marketplaces making the role of e-commerce enablers redundant? What might have been a “special” relationship that players like aCommerce have with the major sellers is now perhaps set on a level playing field?

Brands become more demanding

Brands on their own are growing increasingly competitive and demanding in recent years.

With e-commerce becoming more established in the region brands are getting better educated about business strategy and are becoming more aggressive with targets.

Their appetite to have in-house expertise has driven them to hire staff from marketplaces (e.g., Lazada) and e-commerce enablers (e.g., aCommerce) to forge ahead with their ambitions.

This reduces the dependency on enablers and then there’s the issue of poaching of top execs from enabler companies.

Competition from other enablers

With the role of enablers becoming defensible and less exclusive, which makes it even more challenging is the entry and growth of other competitors, in an industry already under perceived threat.

There still seems to be interest in the e-commerce enabler market. We are seeing a number of new entrants/existing enablers gearing up to take more market share in this area.

N-Squared, founded only in 2017, is an up and coming e-commerce enabler also headquartered in Thailand, competing for aCommerce’s market share. Like aCommerce, it too has an official partnership with Lazada and Shopee (access to more brands and customers) and has over 30 brands under their management. Not bad with some high profile names for a company around for less than two years.

aCommerce’s website, on the other hand, lists 16 clients in total. The 16 clients are of course bigger, established brands but N-squared is moving fast and aggressive. Recently they were appointed to manage the online marketing and distribution of Huawei products on various marketplaces such that consumers that bought Huawei products from N-squared’s stores got special offers.

Then there’s Singapore-based Anchanto that raised US$4 million in its series C funding in 2018 led by MDI ventures (owned by Indonesia’s largest telcom provider Telkom Indonesia).

Although it has offices in India as well as SEA markets such as Singapore, the Philippines, Indonesia and Malaysia, with the new funding they will focus more on SEA especially Indonesia. This is where aCommerce too gets its biggest revenue source- hence direct competition.

Telkom Indonesia will give Anchanto access to its 170+ million users as well as its digital platforms, mobile payment (T-cash!), and Telkom’s DELON service for eCommerce fulfilment/warehousing– all which will enable them to scale up and onboard thousands of Indonesian small and large enterprise business to e-commerce.

We think that for the aCommerce to grow and stay relevant they need to tap into a large number of businesses that are still offline and make it easy for them to venture into e-commerce (in Indonesia less than 2% of retail business is online). However, this is also where they face stiff competition from competitors like Anchanto as well as big marketplaces like Lazada and Bukalapak that are using their huge fundings to partner with offline vendors in remote areas and mom-n-pop stores.

What’s next?

So what’s in store for aCommerce’s future? Will it realise its ambitions of an IPO or are investors betting on hopes of cashing out by being bought by a giant player?

We won’t lie- we are surprised no one has covered about the industry’s open secret regarding aCommerce’s struggles yet. However, we hope to get more viewpoints from anyone and everyone who would write in to us. We will publish every, and all angles of the story.