In part 1 we briefly discussed the future of crypto where we suggested that central banks around the world might pick-up bitcoin as a means of balancing their portfolio or turn to issuing their own cryptocurrencies. Part 2 will focus on how exactly to position yourself to profit from this.

Since then, bitcoin has plunged below US$10,000 and is currently trading between US$11,000 and US$13,000. It has been hailed as the bubble that has finally popped, but has it? Since 2011 many pundits and detractors have called for its death, but it has gone from strength to strength.

Price of cryptos are less important than the industry it will put out of business

The internet has put countless organisations out of business. It is single-handedly one of the most important inventions of the 20th century. In the early dotcom boom, stock prices of many internet companies shot through the roof. Many of them (if not most of them) had no fundamentals – but they were backed with the dream that the internet was the enabler of all. This is the exact same situation we are witnessing today with the crypto boom.

The financial industry, though very regulated and very protected by governments around the world, will find it hard to shake off the progress and disruption that cryptos have introduced to the industry. For one, it is helping push through the government agenda of a cashless society, but perhaps not in the way governments have envisioned – to have control.

It is time businesses (regardless which industry you are in) take this revolution seriously. 9 years in the making (that is how old Bitcoin is), it is no longer a play thing or a bubble. Adapt, and stop complaining or be prepared to be put out of business.

Creation of a new asset class

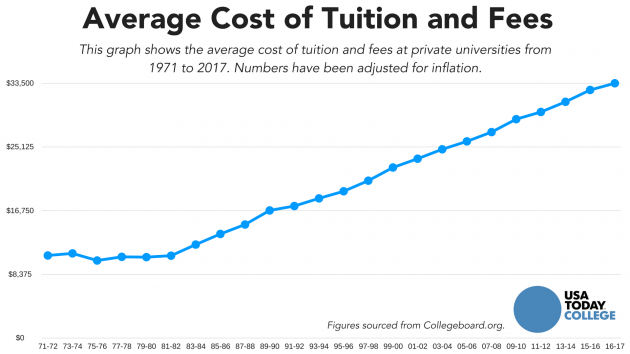

In the past half century or so, the world’s economy has grown tremendously and in the process it made the baby boomer generation incredibly rich and comfortable. Yes, we are most likely referring to your parent’s generation, who probably benefited a lot from the stock market boom, real estate boom and affordable higher education. It used to be entirely feasible to study in the best schools the world had to offer, and work part-time waiting tables. No loan was necessary.

However, take a look today. Quality higher education, real estate, and even stocks are out of reach for most young adults. Most young adults cannot enjoy the fruits, let alone afford to invest in this “paradigm” their have been enjoying for many decades. The younger generation will now have to pay higher taxes to fund retirement and pension funds that they will never enjoy. Many have come to see the situation as a kind of ponzi scheme.

This changed when bitcoin, blockchain and cryptocurrencies provided a possible escape from this perceived trap. In a recent survey conducted in the United States, it was found that 27 percent of millennials would prefer to invest in $1,000 worth of bitcoin rather than the same amount of stocks. Our advice is not to be too quick to write off this potentially new and very lucrative asset class.

The World would be better with more science and maths, and less interest payments?

Are traditional bankers a dying breed? Yes, bankers still command the highest pay packages – but this is rapidly changing. Individuals highly specialised in crypto will no doubt be the next millionaires and billionaires. Why even bother studying finance? Does this mean parents will again push their children to pick up math and science, instead of studying public relations or finance?

Perhaps the crypto boom would be the biggest catalyst to push many people out of poverty, to enable the disenfranchised to build their lives up without the threat of high-interest payments. After all, who cares if the banks go out of business because they cannot leech off the productive members of society? That is indeed what crypto aims to do. In any case, we believe the current finance model will be disrupted, like it or not.

It may sound dystopian, but future generations looking back, may laugh at the very idea of the stock market, teller machines and paper money.