The article is written by Reinaldo Gani on Medium, republished on TheLowDown with the author’s permission.

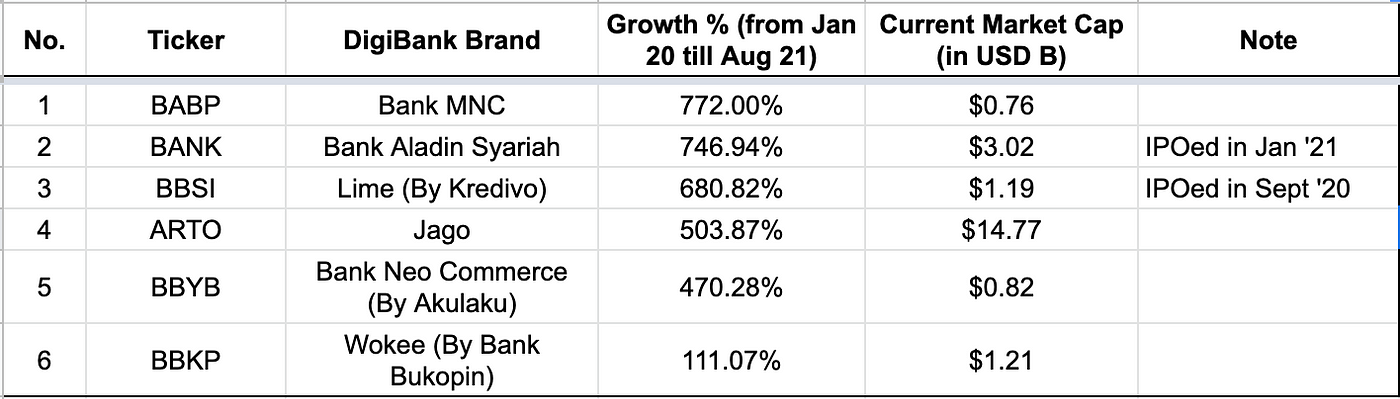

Recently Digibanks were getting all the spotlight in Indonesia especially from equity market investors with numerous new banks going public and astronomical stock price performance in the last 1.5 years.

As of Aug ’21, JAGO (Bank Jago) has witnessed almost 503% growth since Jan ’20 and BANK (Bank Aladin Syariah) that went public in Feb ’21 saw 746% growth.

But, how are digibanks any different from incumbent banks that digitalize themselves?

Being digital in nature, digibanks have the advantage to acquire and serve customers from all over the archipelago with a fraction of the cost of what incumbent banks will incur since digibanks require no or minimum physical branch.

With more than 17,500 islands and ~52% of Indonesians are still unbanked, digibanks can certainly increase financial inclusion in the country.

Digibanks can also provide personalized financial products tailored for every customer leveraging digital technology and data science. For example, portfolio recommendation for someone with a certain risk appetite, financial milestones, and age.

I took a look at some of digibanks’ products that have been launched to the public and observe that all of them are still pretty plain vanilla. Most offers simple current account & saving accounts (CASA) complemented with a debit card. Some of the other common features are subsidized interbank transfers and e-KYC for onboarding.

Playbook from other Regions

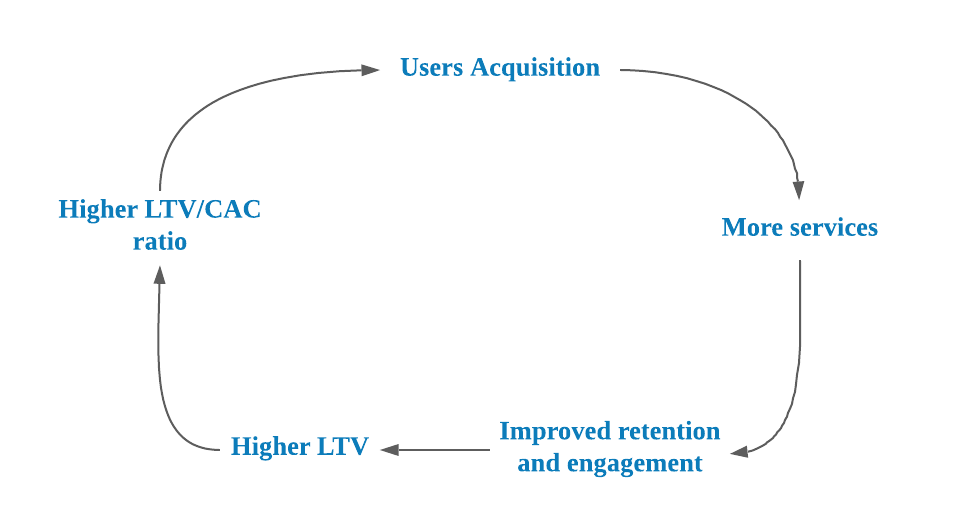

With the capital that these digibanks have raised, I’m curious to see what new product innovations they plan to offer.

Learning from consumer fintech apps’ playbooks from the other regions, the end goal is to always achieve LTV > CAC by increasing retention and engagement over time. The usual go-to-market is usually launching with a simple but strong wedge product to hook initial users and subsequently create other financial services to further increase retention & engagement.

We have seen a few successful use cases in Indonesia. The common theme is to provide daily financial products that are used frequently with a better experience, cheaper, and better access using technology.

- Saving account + debit cards — e.g. Jenius

- Stock trading — e.g. Ajaib

- Peer-to-peer transfers — e.g. Flip

- Stored-value wallet — e.g. OVO, GoPay, Dana

- Buy Now Pay Later — e.g. Kredivo, Akulaku

Land Safely then Expand

Neobanks from around the world have common patterns of launching a wedge product that is significantly underserved by the incumbent financial institution. Revolut for example started out by giving prepaid cards with free international transactions where the usual cards by incumbents will charge between 1.5%-2.5% FX spread fee.

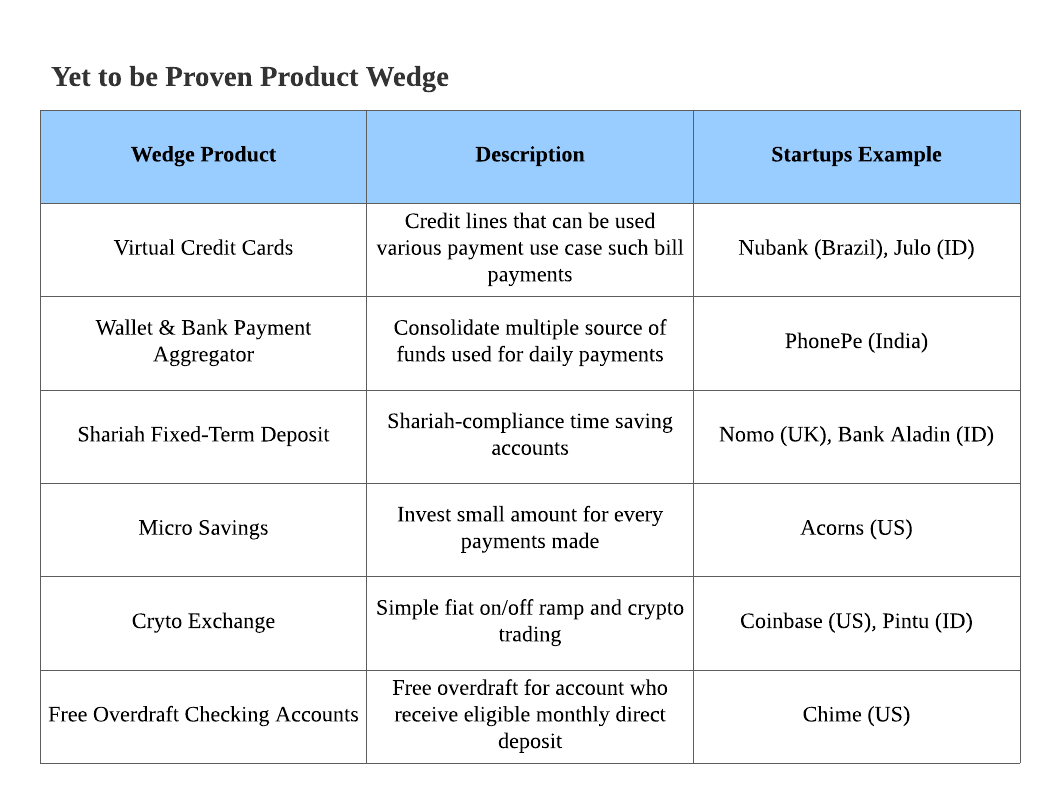

These wedge products are high-frequency and simple use cases such as payments and micro-investment. The other common theme is to offer more affordable access to incumbent financial products such as virtual credit cards and free overdraft checking accounts.

Learning from different companies, I consolidated a few proven product wedges in other regions that have not been proven to be successful in Indonesia.

What Product Features Can Improve Users’ Financial Situation?

Once a digibank has a strong wedge product now it’s time to expand to adjacent financial product offerings.

I have a laundry list of features that I believe if executed correctly can be very impactful for the customers and eventually increase retention & engagement.

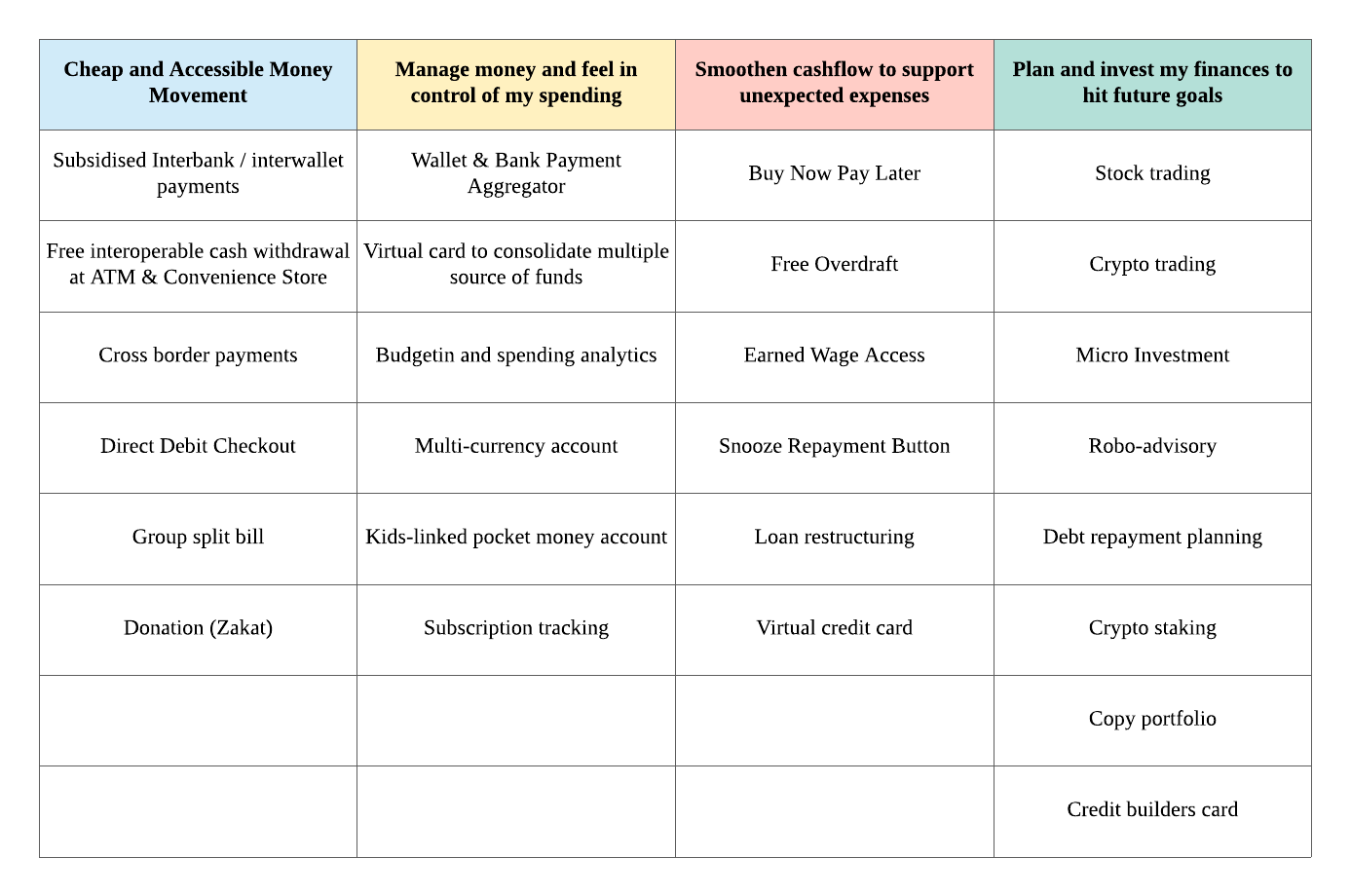

Broadly I have divided the product into 4 users’ needs

1/ Cheap and accessible money movement

Money movement use case is probably the most high-frequency use case in financial services. Affordability and speed is the name of the game for this bucket. With interbank transfers still cost ~IDR 6,500 (USD 50c), fintech can leverage treasury management to help subsidize interbank transfer costs.

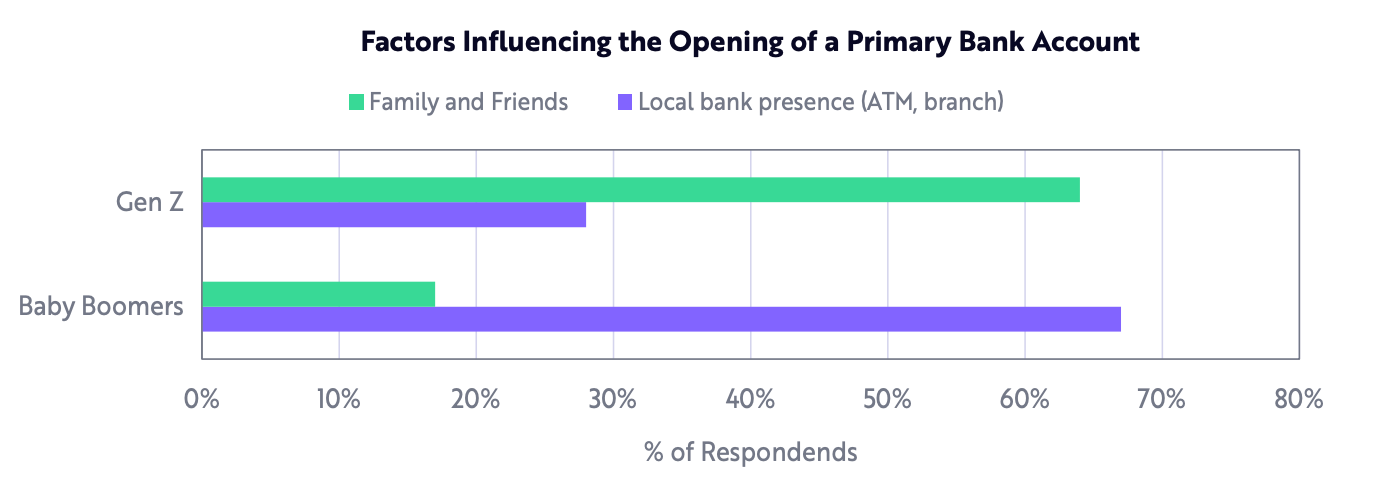

As much as the world is moving towards cashless, cash will still be around us for a long time. For the older generation especially, having the option to be able to withdraw cash free of charge with the widest ATM network can be a strong value proposition. US research suggested that for baby boomers ATM network is the biggest factor for them to open a primary bank account.

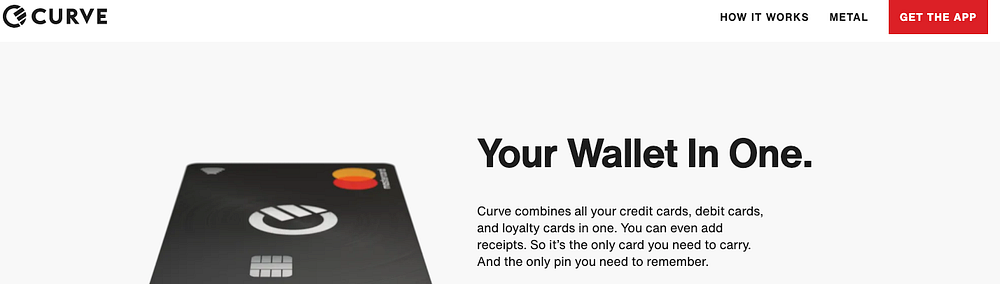

2/ Manage money and feel in control of my spending

It can be overwhelming to track all the money movement from all financial instruments one has, e-wallets, banks, credit cards, brokerage account.

Consolidating all payments and transaction records from different financial instruments within a single app can be a game-changer. Since now users can use one app to pay with all different financial instruments, it will be the de-facto payment app for daily life.

Combined with other social aspects, it can unlock interesting use cases such as digital pocket money where a parent’s account is connected to a kid’s account and able to monitor and control spending.

Example — Curve (UK), PhonePe (India)

3/ Smoothen cash flow to support unexpected expenses

The majority of working Indonesian adults working paycheck to paycheck, some estimate the number can go up to ~70% which sometimes creates cashflow volatility and unexpected financial expenses.

Players such as Chime offers free overdraft up to $200 for an account that receives monthly payroll direct deposit. Chime also offers early wage access (EWA) for up to 2 days in advance, to help alleviate users’ financial needs.

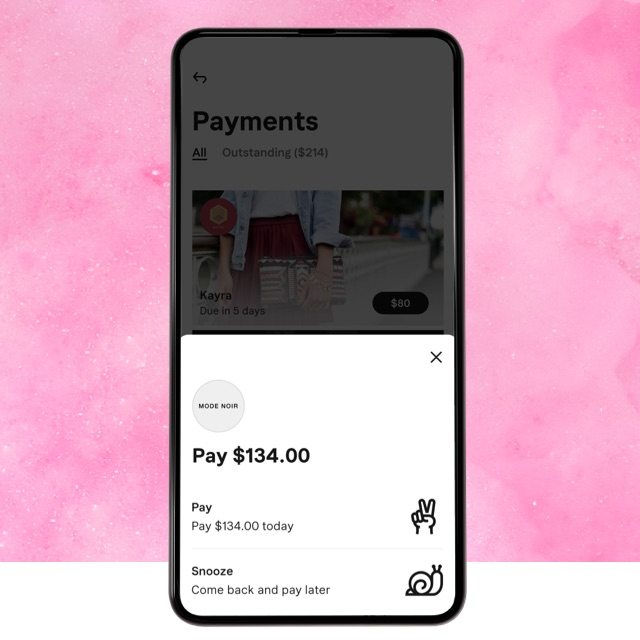

Klarna, one of Buy Now Pay Later (BNPL) player give their users an option to snooze repayment date for a few days for a small fee (smaller than the actual late fee)

4/ Plan and Invest my finances to hit future life milestones

There are 145.3M Gen Z + Millenials aged 8–39 in Indonesia which represents 53.81% of the country’s population. With a non-existent retirement system in place (e.g. CPF in Singapore) and low financial literacy of 38.03%, people in this bracket have to plan their finances very well for big milestones in their life.

Most young adults in their 20s or 30s can expect few life milestones such as housing, cars, wedding (the median marriage age in ID is 25) waiting ahead of them.

There are 2 schools of thought to help people better plan their finances.

First, is the belief that people want to be in the captain seat when it comes to their finances. For this user segment, trading accounts such as Robinhood and Coinbase are enough to fulfill their needs. For more risk-taking users, they might want to explore a higher yield than the usual saving accounts such as crypto staking feature with interest rate up to 10% per annum (e.g. Blockfi)

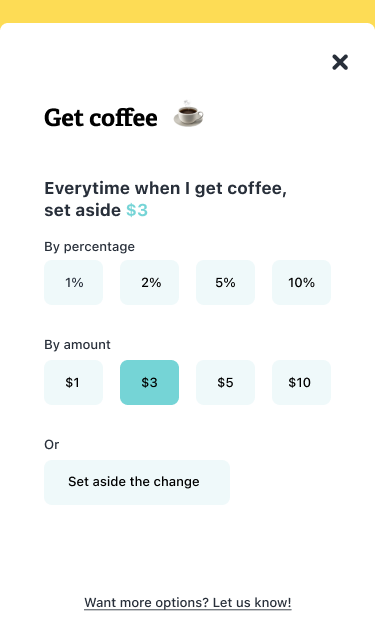

The second school of thought is that people need guidance in planning their finances and managing their investments. Acorns (US) combines micro-investment and robo-advisory so that users can round up their spending and automatically allocate the rounded amount into a robo-managed investment account. Additionally, users can create special-purpose sub-accounts (e.g. house, wedding, school) to reinforce discipline. The sub-account can also be shared with others (e.g. parent, spouse) so that more than 1 person can contribute to the vault.

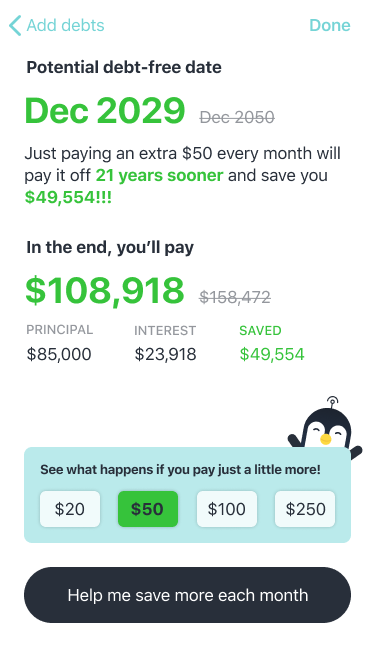

While most personal finance management (PFM) fintech focuses on how they can grow user’s assets, no one really pays attention to reduce user’s liability. If a mortgage or credit card debt can be visualized and its payments can be automated, a user might be able to pay off their debt much faster.

I have put some other product features I found interesting and categorize them in the below table.

Many of the interesting use cases mentioned above require a major revamp in our existing financial infrastructure which I spoke briefly about in my previous article. Financial infrastructure such as open banking enables access to banking products in a granular building block to rebuild superior financial service products.

If you want to bounce ideas or looking to build something in the space, feel free to reach out to me at [email protected]