Momentum Works’s deep dive into the Food Delivery Market in South East Asia (SEA) – Now and Post Coronavirus

Momentum Works has published the “Food Delivery Platforms in Southeast Asia (SEA)” Report where we analysed the food delivery market in Southeast Asia – the macro landscape, players, challenges, and factors for growth. We also evaluated the fundamental differences in SEA’s food delivery industry when compared to overseas players and present a comparison between the different players in SEA.

Five key highlights below.

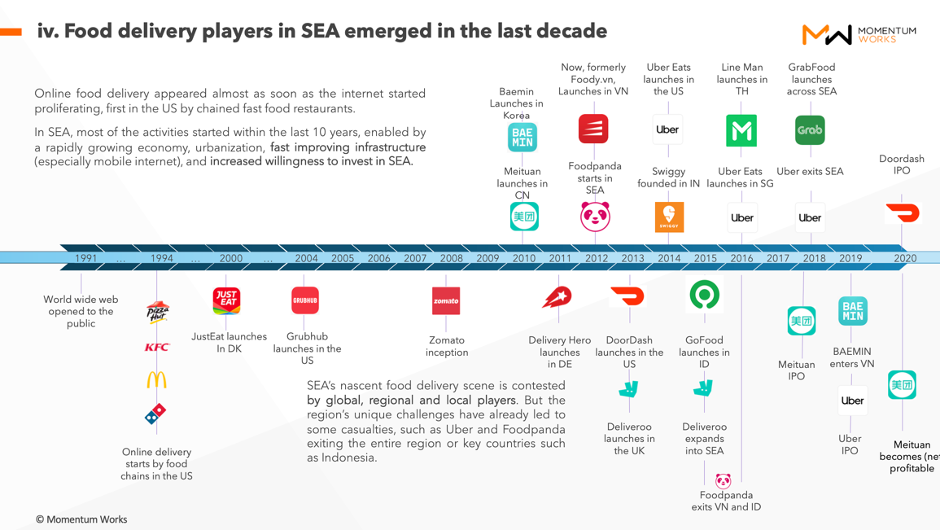

1. Food delivery in SEA has grown significantly in the last decade.

Competition continues to intensify among global, regional and local players – with some retreating from key battlegrounds or exiting the region entirely.

2. Food delivery grew 183% from 2019 to 2020 and is estimated to reach $11.9bil in GMV by the end 2020.

COVID-19 accelerated the growth of the industry, and we expect a large part of the growth to be permanent given the increasing digitalisation and changes in consumer behaviour.

All markets saw accelerated growth in 2020, with the three largest food delivery markets in SEA being Indonesia, Thailand and Singapore, contributing US$3.7bil, US$2.8bil, and US$2.4bil in GMV respectively in 2020.

Grab contributed almost half of the region’s food delivery GMV in 2020, with leading positions in 5 out of the 6 markets. It is followed by Foodpanda, which operates in 4 markets, and generates about 20% of the region’s GMV. Gojek, which owns about half of the market share in Indonesia, came third.

3. There are many reasons for the trend – unique to SEA and will shape the key players in the region.

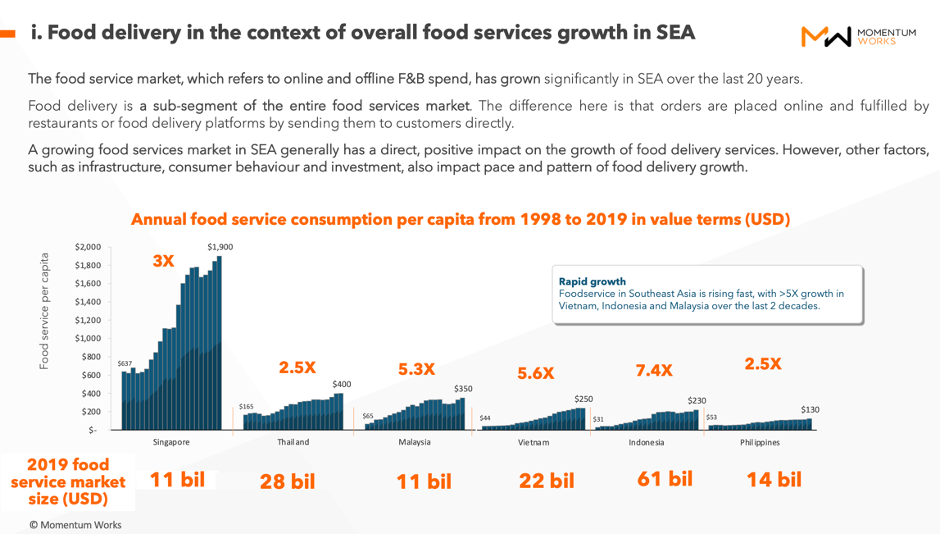

(a) Disposable income and offline spending on F&B may be low in SEA; but overall food service spending has been growing with economic growth and urbanisation. With the proliferation of smartphones, online food delivery spending has been growing healthily. While the average food delivery order is lower in SEA compared to other regions, this can be offset by high volumes and density, similar to the case in China.

(b) Fragmented food service market creates more opportunities for innovation. About 90% of restaurants in SEA are independent and are slow adopters of food delivery services, but they are also much more dependent on food delivery platforms than chained restaurants. This fragmented market gives platforms more room to innovate and differentiate their offerings from competitors.

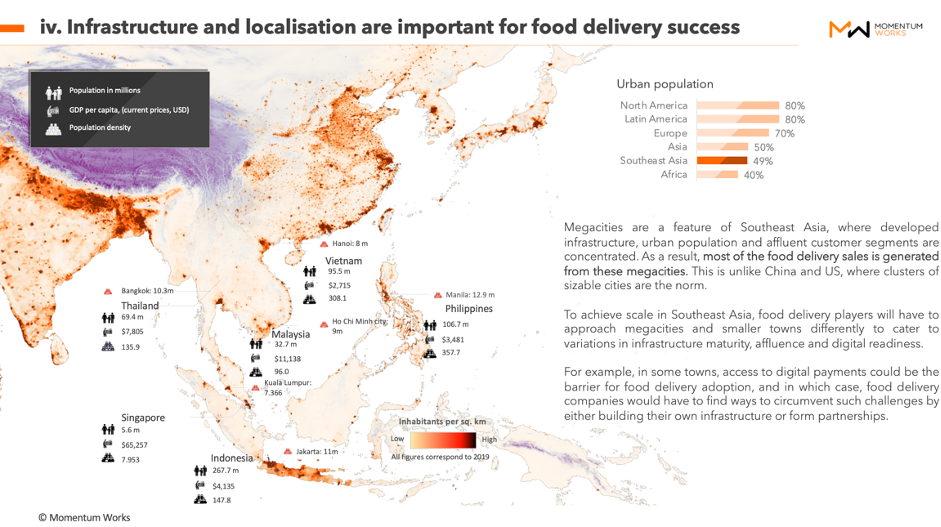

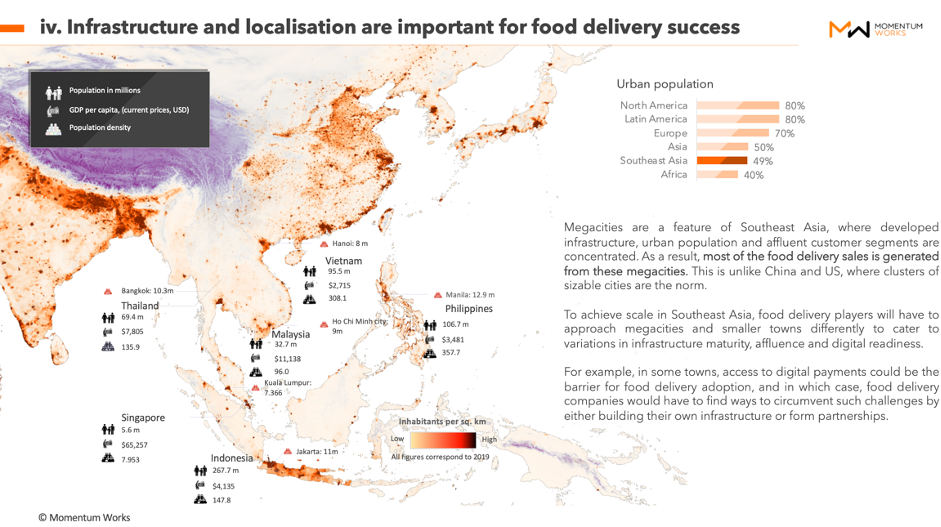

(c) Infrastructure and localisation are critical for food delivery success. Most of the food delivery sales are generated in megacities today. As platforms scale outside of megacities and into smaller towns, they’ll have to adapt to variations in infrastructure maturity, affluence and digital readiness. By nature, it’s more cost-efficient for super apps like Grab and Gojek to operate in Southeast Asia as they already have the transport and payments infrastructure required for food delivery to scale.

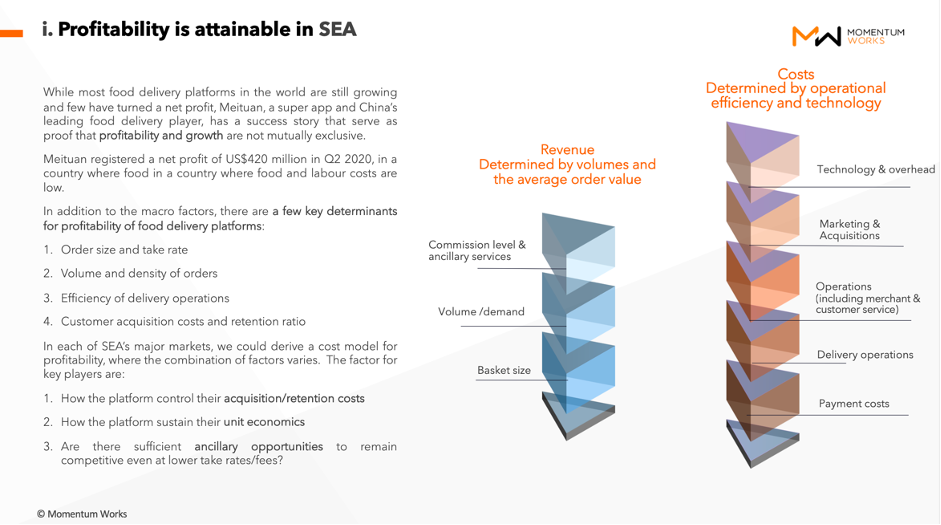

4. Profitability is attainable in SEA if the players can balance the various revenue and cost factors.

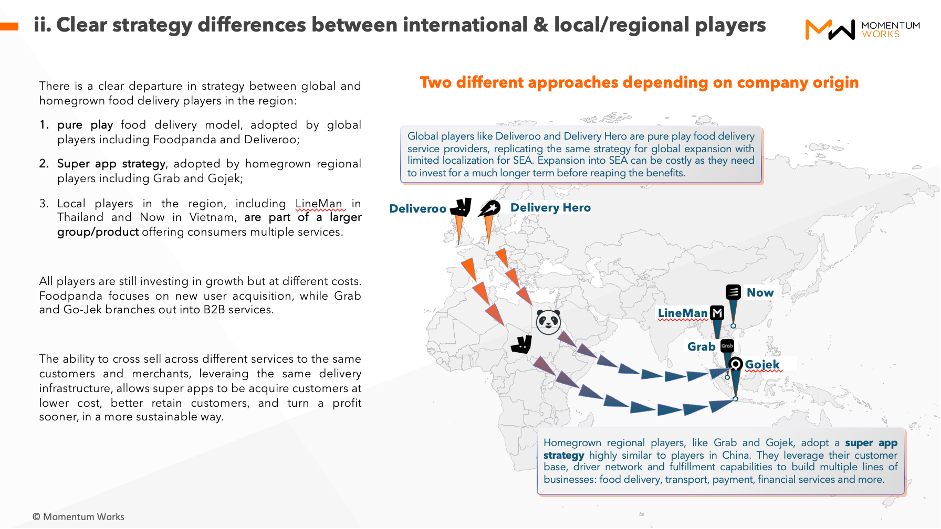

5. Grab, Foodpanda and Gojek are key players in the region. Each has their distinct strategies, pros and cons.

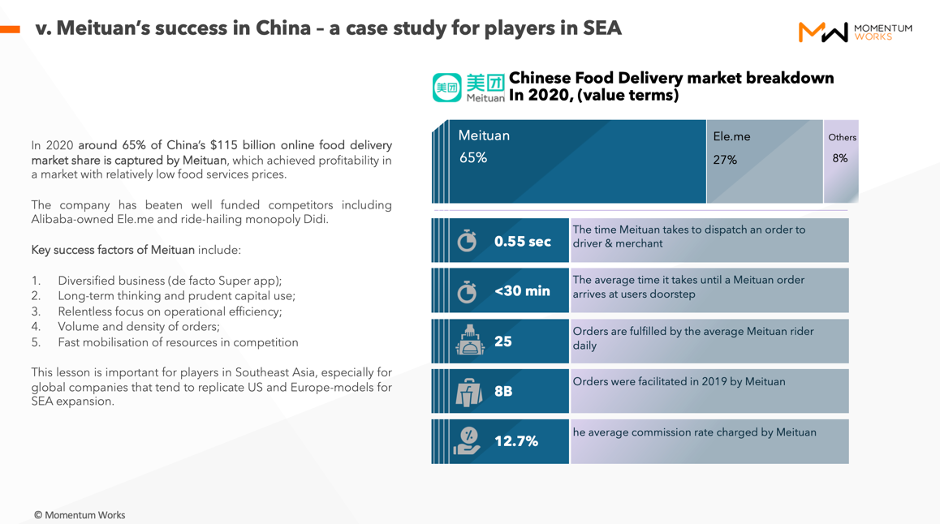

The path to profitability is clear, with Meituan in China setting a very nice case study, though approaches among the three key players differ:

(a) Grab’s super app strategy lowers the cost of acquiring users. The company, however, will have to respond to competitors with a high appetite to spend to gain market share in the short term. Its move to expand into B2B services is promising if executed well.

(b) Foodpanda’s user acquisition and market share strategy in SEA is based on heavy price promotions, as they have high growth expectations. The challenge is to prove its ability to hold market share when promotions are removed. Its expansion into product and grocery delivery services provides some diversification and an additional revenue stream.

(c) Gojek is juggling many priorities. While still strong in Indonesia, it is seeing declining market share in its home country which puts it in a defensive position. Their efforts to expand outside Indonesia since late 2018 have had very limited impact so far.

In conclusion

There are many strategies that food delivery players are taking. Unlocking this market will require food delivery companies to adapt to the SEA context and address challenges such as low food service prices, infrastructure and city variations, and cost management. As such, high growth doesn’t mean that any company can easily tap into the SEA food delivery scene.

Covid-19 pandemic proved to be a key accelerant for adoption. Path to profitability is clear, with Meituan in China setting a very nice case study. Execution is key.

To gain a better understanding of the food delivery ecosystem in SEA, get your hands on a copy of this report by clicking here

4.0")