This article originally appeared in Chinese on Momentum Works’s WeChat account. Translated into English by the Momentum Works team.

Investors, ecosystem stakeholders and Indonesian consumers have been following with intense interest the merger of GoJek and Tokopedia. Social media in Indonesia is awash with comments, mockeries and of course memes.

Although the synergies between the two firms are still questionable, they are ultimately the country’s two biggest unicorns with backing of notable investors.

However, the merger could profoundly affect the trajectory of another unicorn.

The upcoming divestiture

Being the leading digital wallet super app in Indonesia, OVO’s counts Grab and Tokopedia as the largest shareholders. In fact, Tokopedia might have increased its stake in OVO last year – which was not a bad hedge considering that Grab-Gojek merger was more plausible back then.

Since GoTo (the merged Tokopedia-Gojek entity) and Grab have become main competitors, there are questions about how Tokopedia is going to deal with its OVO stake.

Besides, Bank Indonesia (BI – the central bank) does not allow any company holding controlling stake of more than one e-wallet. With the merger GoTo will own controlling stakes in both OVO and GoPay.

While the breach, if GoTo were to retain its OVO shares, might be tolerated for a period of time by BI, it poses a big problem for public listing in the US.

Therefore, it is not a surprise that Tokopedia is now talking about divesting its shares in OVO.

We had predicted market consolidation in Indonesia in January 2020 – and it seems things finally accelerated in 2021, with the unicorn IPO dash.

As mentioned in the beginning, Indonesian social media users are unleashing their creativity to create all sorts of memes:

A bit of history (of OVO)

In the early days back in 2016, OVO was only a mobile payment application under the Lippo Group. Since then, BCG claims that it played an important role in the growth of OVO.

Originally developed by Lippo Group, OVO became the wallet of choice by Grab and Tokopedia later on as BI restricted new e-wallet licences. Both invested heavily in OVO and emerged as the top shareholders.

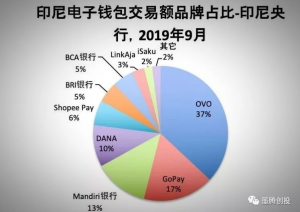

At the operational level, OVO was fully integrated into both Tokopedia and Grab – giving the wallet a strong combination of use cases: food delivery, ride hailing and ecommerce. Coupled with offline use cases both from Lippo and acquired by OVO’s own teams, OVO’s mobile payment ecosystem, back in 2019, was unrivalled.

OVO has also invested in or acquired startups in lending and other adjacent sectors to complement its core payment offerings. According to BI numbers that year, OVO was ahead of other e-wallets in user numbers and transaction value.

The changing landscape

The pandemic has accelerated digital adoption but also changed the market landscape.

On the one hand, ShopeePay has buoyed with the growth of Shopee’s ecommerce operations in general (which we will talk about in more detail in the upcoming 2nd part of Ecommerce in Indonesia report).

On the other hand, traditional conglomerates are cutting back their investment into digital wallets, as many of them realize the ball game is different from what they had anticipated. For example, there were reports that Dana, a joint venture between Ant Group and the local Indonesian consortium Emtek, would be merged into OVO.

The Japanese leasing giant Tokyo Century, which invested more than US$100 million in OVO before Grab and Tokopedia came into the picture, exited Indonesia’s fintech market.

In the meantime, as the competition intensified, OVO was also forced to juggle the priorities of its two biggest shareholders – Grab and Tokopedia. While Grab was gaining market share over Gojek, Tokopedia was losing to Shopee.

While this was understandable, it was probably not an ideal scenario for OVO, as it tried to develop itself into a digital finance super app in Indonesia, capitalising its head start and leading market position.

Blessing in disguise

After the merger of Tokopedia and Gojek, Tokopedia has already begun to take actions to de-prioritize OVO. For example, while OVO is still a prominent top-up and payment option, Tokopedia has replaced OVO’s loyalty points with its own.

Strategically, keeping shares in both Gopay and OVO should be more beneficial to GoTo. However, for the reasons mentioned above, it is not really feasible when the company is aiming for an eventual US IPO.

The plausible withdrawal of Tokopedia, however, might turn out to be good news for OVO. It will have to juggle with less competing priorities, and consolidate its cashback and discounts.

This will help with the bottom line, but that’s not the main point. The key is strategically OVO will be able to be more focused in developing its own ecosystem, regardless whether Grab takes over GoTo’s shares or not.

OVO’s existing ecosystem and relatively comprehensive financial offerings are still very valuable. After all, compared to an embedded wallet, OVO – being an independent app – shares more resemblance to Alipay, giving it the capacity to become a Super app in the financial sector by itself. (Imagine trading shares on Shopee’s Gojek’s app?)

The high-quality customers already acquired and served by OVO are likely to be the targets of emerging digital banks, offering opportunities of not only collaboration but also strengthening of the ecosystem.

Paytm in India, without a strong use case of any parent, has managed to survive and is now aiming for an IPO. We should not doubt whether OVO can do the same – as long as they retain strategic clarity and strong execution.