Our own Jianggan Li moderated a panel discussion on ICO & Regulation last Thursday (12 Oct), as part of INSEAD FinTech Week. On the panel were Daniel Ben-Aron, Csaba Robert Horvath, Nizam Ismail, David Moskowitz, and Igor Pesin

In addition to an extensive (and sometimes intensive) exchanges on regulation and regulators, the panel also discussed whether ICOs are indeed more democratic, what the real costs of ICOs are, and where the middlemen (like the VCs) will find their place in a world of ICOs.

Here is a quick summary of the highlights during the panel:

What do the panelist think about ICOs?

The panels have different perspectives on ICOs, especially from legal and regulatory points of view:

ICOs are an effective way to raise funds. When used correctly, it can help entreprises, startups raise funds efficiently, directly from the market. This benefits investors, as well as the society. The risk is high, but so is the potential return. There are companies, even those completely unrelated to blockchain, raising funds through ICOs. From this perspective, regulators could appreciate the value that ICOs bring.

ICOs are just one way to circumvent the laws, which are put in place to protect the consumers and prevent fraud. For example, the SEC in the US makes clear that if you are buying a token and that token, as result of you holding it, is going to return any funds to you directly- then it’s a security, plain and simple. But there are some ICOs trying to get around the regulations by pretending to be something else.

Rules are grey, and there is quite a sizeable space for development.The crux of whether existing regulations apply to a cryptocurrency or an ICO, depends on its definition of a security. In jurisdictions like Singapore, Hong Kong and Australia, the regulators provide a positive list of what is a security, whereas the regulations in the US are broader, i.e. anything that implies an indebtedness to a company or an investment contract can be considered a security. One panelist noted that whether an ICO is listed on an exchange shouldn’t be the only factor to assess whether this is a security. It could be ONE in a matrix of factors to determine how the ICO should be regulated. It is worth noting that two of the panelists have legal background.

What is the regulators’ state of mind concerning ICOs?

Some were caught off guard and had to do something about it. To put it in context – In China, ICOs were unheard of in April this year, but in September, everyone was buying these coins! Even people in the countryside who had no idea what a security is were buying it because their friends and family claimed that it was THE way to make money now. This scared the government because there is a risk to social stability. Why? There have been, historically, a lot of scams disguised in technology and trendy terms. A lot of these happened when many retail investors, who didn’t have the knowledge to invest, got burnt and put the blame on the government for not protecting them. So the government extremely careful about these investment schemes which could quickly spin out of control. And that is the reason why the Chinese government has shut down ICOs. Nonetheless, this does not mean the ban is permanent – putting a pause at it allows time for the government to come out with proper regulations.

Regulators don’t understand it (yet). The sense is that most governments feel that ICOs are moving very fast, and they don’t know what to do – some have a notion that these are scams and should be banned, others feel this is the beginning of a more effective way of investing.

So, most are curious and want to learn. For example, the Monetary Authority of Singapore wants to understand why companies are coming to Singapore to launch ICOs. They want to understand it, instead of just shutting it down. They have been reaching out to industry players to understand the cryptocurrencies as well.

The DNA of regulators is to think of the worst possible outcome. They could have seen the ICO as a tool to perpetrate fraud or scams. They could have made it very difficult for the ICO industry – but they did not. It is a small niche market, and they want to see what will happen because it could be good for Singapore. It could potentially be the next stage of economic development.

So, the more the industry engage with the regulators, the easier it is to discuss and explore whether existing body of regulations today can regulate such activities. That is why people in the ICO industry are volunteering to teach institutions about blockchain technology, about smart contracts and decentralised applications.

Regulators do not want an unregulated market but they don’t want to thwart innovation either. The happiest moment would be when such innovations happen in their jurisdiction, without causing anything bad.

It will be a while before there are clear regulations specific for ICOs or cryptocurrencies

There are still a lot of grey areas before everyone can agree to clear regulations for ICOs or cryptocurrencies. Regulators might address some of the gaps relating to anti-money laundering but how would you regulate cryptocurrencies as it is? How are you going to enforce something that is easily tradable anywhere in the world? It’s hard to enforce. The problem is that current regulations were not designed for the cryptocurrencies and it is going to cause regulators to rethink a lot of stuff at the basic level.

What does the wider community think about ICOs and cryptocurrencies?

Apart from the negative remarks on cryptocurrencies made by some figures (e.g. some chairman of some bank), let take a look at the positive comments in the market.

A former SEC chairman said positive things about cryptocurrency. He said that it would be here to stay because it actually balances out some of the gaps in monetary policies of certain governments. The IMF chief said that cryptocurrencies could actually address financial inclusion issues. More and more people are realizing the value that cryptocurrencies can bring.

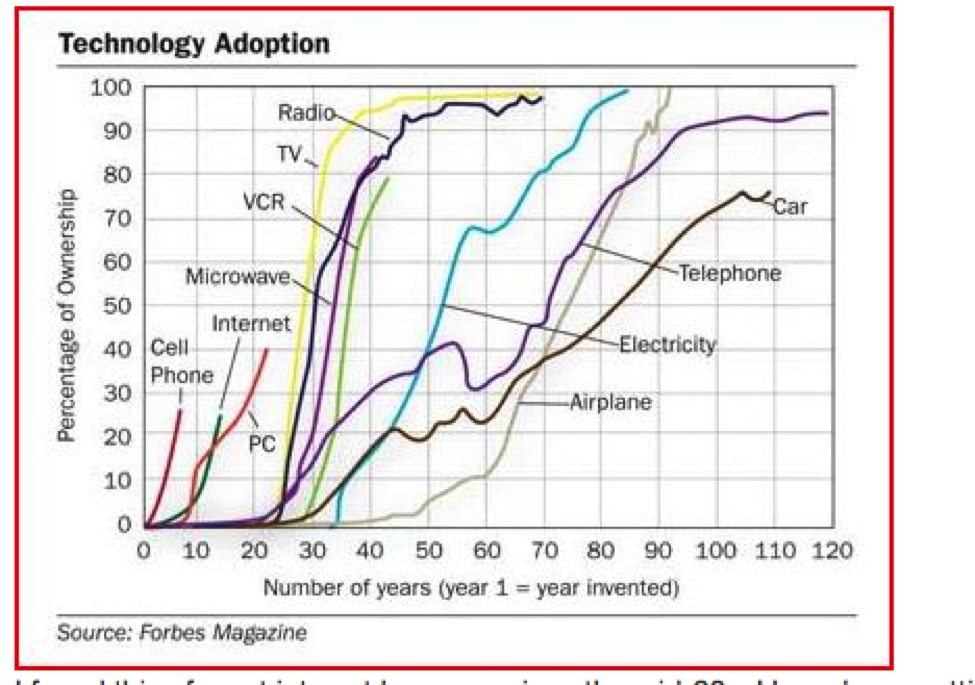

You could say that the surge of ICOs points to a bubble. But if you think about the technology adoption of things that have revolutionized human history (e.g. telephone, television, car, microwave, internet), the trend (see table below) is similar to the what we are seeing for the ICO market. The question is whether ICO is going to revolutionize the way money is raised, or is it just the tulipmania all over again.

What some people are seeing is that in most cases of ICO purchases, people don’t know what they are buying or what the underlying structure is. There are even some successful ICO with 90 pages of document, of which 60 pages are conditions and full of disclaimers that “We are not responsible for anything. We are not accountable for anything.” So in this aspect, it is truly the wild wild west. The regulators are trying to encourage the usage of ICOs for their benefits but clamp down bad or irresponsible behaviours. That is the way forward.

Is ICO a more democratic way of raising money?

There are two schools of thoughts on this:

Yes – If you are an enterprise and you want to raise funds, the options you have today is to go to your angel investors, friends, family or VC funding and then you go through a trade sales or IPO process. It’s long and painful. Of course you can argue that the process will have some mechanism to do some checks and balances but it is less efficient and more expensive (you need the auditors, lawyers, go through a rigorous process). With an ICO, you can reach out directly to the market without going through this process. You don’t have to get your stocks traded on an exchange or pay expensive listing fees.

No – An IPO could be just as efficient if we remove the outdated regulations. But if the regulations are actually needed, then it is no more efficient, and you are underpricing the risk of fraud and uneducated consumers. So in this some people are sceptical that ICOs are more efficient.

Also, when more and more companies opt to raise money through ICOs, it becomes increasingly difficult for them to stand out. Thus, to reach out to investors (and to explain to investors why they should invest), they spend a lot of money on legal fees, underwriting and especially marketing. There were instances where an ICO marketing cost amounted to close to US$1mil.

Two of the panelist made a bet on this (with a number of ethers). Let’s see who is right in a few years’ time.

What’s the future of ICOs?

ICO participants: More and more people who are less tech savvy and less involved in cryptocurrencies are becoming interested in investing in ICOs as an alternative investment class. More and more companies who are thinking of doing ICOs are not the traditional blockchain-based or blockchain-aware companies, but conventional companies willing to adopt some blockchain applications within any of their functional teams, and looking at ICO as a way of generating tokens to facilitate funding. So ICOs are getting more and more acceptance.

Regulations: There could be regulations in future that only participants with some knowledge and qualification can buy ICOs – e.g. “Do you understand how to secure your cryptocurrency? Have you bought bitcoin or ethereum before?” – so that the customer has a technical sophistication before they can participate. Hopefully this will protect the aunties and uncles of Toa payoh and Punggol who don’t understand this sort of things. It is conceivable at some point in time, when a significant amount of aunties and uncles start investing in ICOs, the regulators will see a greater need to regulate this.

The middlemen: intermediaries will still be there, but just wear a different hat. Most panelists do not believe that disintermediation will happen. For example: VCs will act not necessarily as gatekeepers (as they are now), but as trusted advisors issuing opinions to those who put the money in ICOs (their LPs now). It is a marketplace at the end of the day with great asymmetry of information, so you always need someone in the middle to facilitate information flow and transactions. It is for the same reason real estate portals never replaced the agents.

Conclusion of the panel discussion

There were people saying that bitcoins wouldn’t survive when it started a few years back, and now we are seeing the ICO evolution.

Yes, there is a bit froth and euphoria about ICOs, and there will be some instances of fraud. But along the way, if you believe in the markets forces, then there will be a new equilibrium, and people will wise up to the value ICOs and encourage proper behavior.

But who knows what will happen in a year? Things will change and there may be some form of regulations or guidance in this space in different jurisdictions, but people will create new opportunities in new areas surrounding it. It’s just a natural evolution.

At the end of the day, ICOs are not a silver bullet which will completely change the world. It’s just one tool, an effective one, which needs to be put in proper use.