The article is written by Reinaldo Gani on Medium, republished on TheLowDown with the author’s permission.

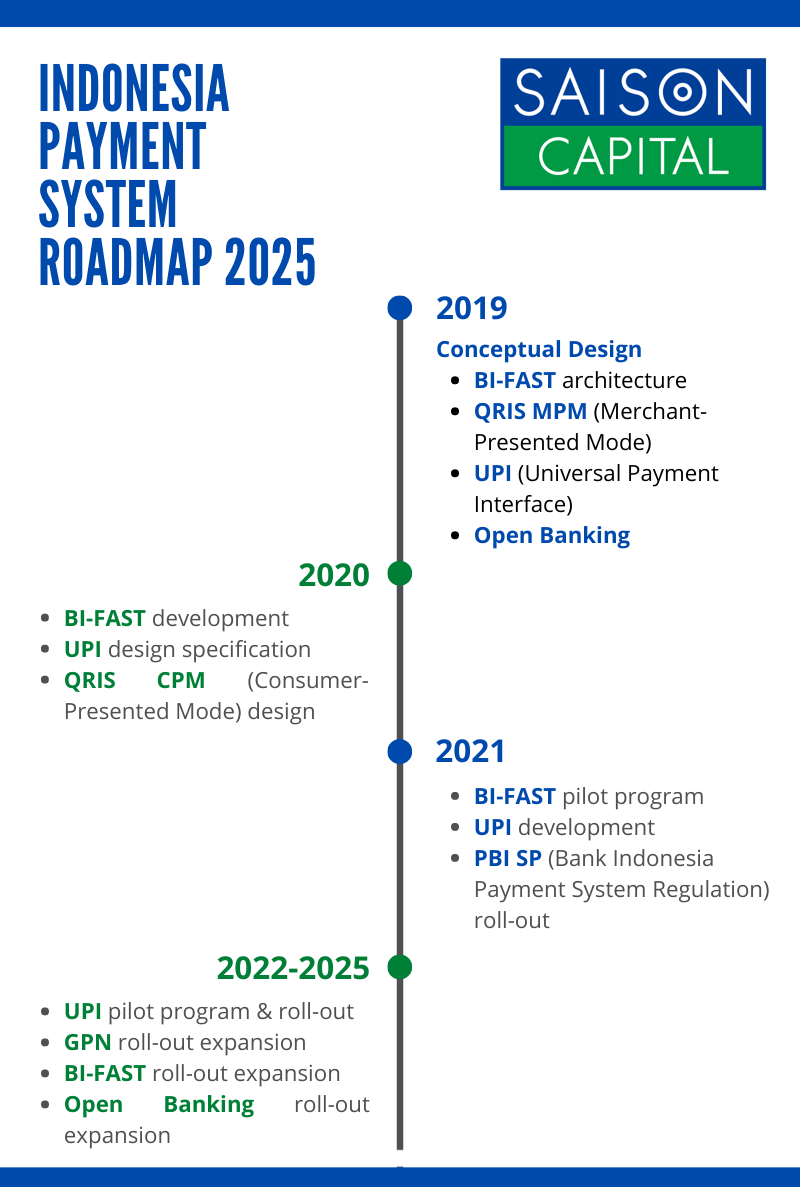

I spoke briefly about my excitement to improve payment interoperability in Indonesia. As part of Saison Capital’s continuous effort to track Indonesia’s payment scene, I will talk about Indonesia’s Payment System Roadmap 2025 in more details and its impact to the ecosystem starting from existing landscape, drivers for change, pain points, payment roadmap, and future possibilities.

Existing Landscape

Indonesia’s digital payment started to develop only in the early 2000s. Indonesia’s payment rails are divided into 2 parts, retail & wholesale. More than 85% of all transactions are currently processed with SKNBI (retail payment rails). This is not surprising as Micro & Small Enterprises in Indonesia attribute to 99% of all businesses and contribute 60% of Indonesia’s GDP.

Retail Payment System

Wholesale Payment System

![]()

Despite all of the government’s push to increase the usage of cashless payment instruments, Indonesia is very much a cash society, second biggest in the world after India. Only around ~15% of transactions are using non-cash payment methods.

Drivers for Change

I observe there are 2 major adjacent trends that popularise cashless payment methods to mainstream populations:

- Smartphones penetration in Indonesia has increased dramatically. In 2020 , Indonesia is home to more than 180 million smartphone users (67% of population). Back in 2015 this number was a mere 90 million which is around half of what we see in 2020.

- Boom of fintech companies. From ride-hailing companies to e-commerce companies, there are tremendous uptick in the development of fintech ecosystem in Indonesia. According to Bank Indonesia, there are currently 56 e-money licensed operators, meanwhile in 2015 there were only 20 e-money operators which were mainly banks. Major e-wallet backed by ride-hailing & e-commerce companies bombard markets with massive discount and cashback promotions to entice users to adopt their e-wallet products.

Pain Points

There are a few issues in existing payment infrastructure that hinders convenient, cheap, and safe payments.

- Data security & privacy. Data security is the first step when it comes to authenticate user’s identity before granting access to various financial data parked under their particular identity. Imagine linking your bank account to multiple e-wallet apps and then one day losing your phone, it can be challenging to revoke all access to your bank account from a centralised location. Currently, there is no standard governance and protocol enforced on how to manage one’s data access, security, scope, and access continuity of various financial information. While some players have adopted the latest state of the art authorisation protocol such as OAuth 2.0, many are still struggling to inject the latest technology because of legacy issues and lack of resources.

- Interoperability. One of the biggest pain points of existing payment infrastructure is arguably interoperability of existing payment infrastructure. Today it is not possible to send or request money from different e-wallets because there are no common payment rails that connect them.

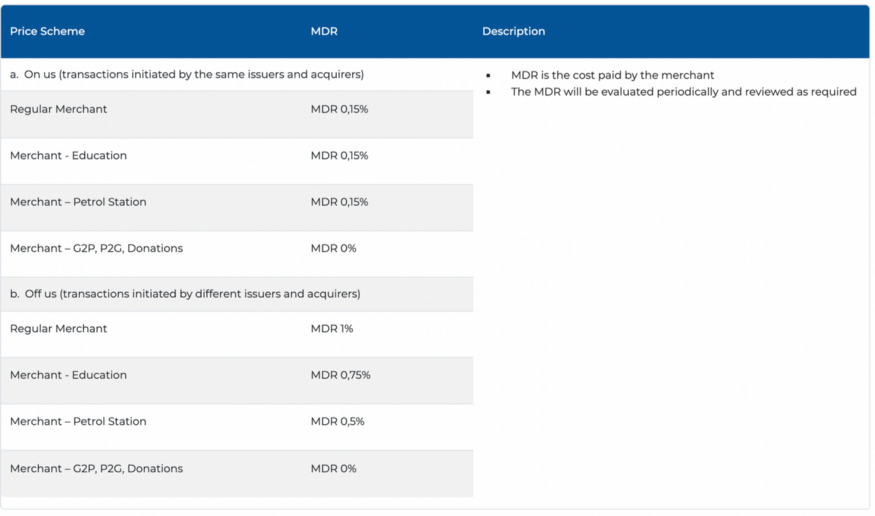

- Cost. Today, interbank transfers will set you back Rp. 4,500–6,500/transaction and will be processed by SKNBI payments in batches and not 24/7. Solving this problem is paramount to accelerate financial inclusion. Having the capability to transfer funds for free will significantly increase the value proposition of cashless by bringing it on par with existing players, cash!

. . .

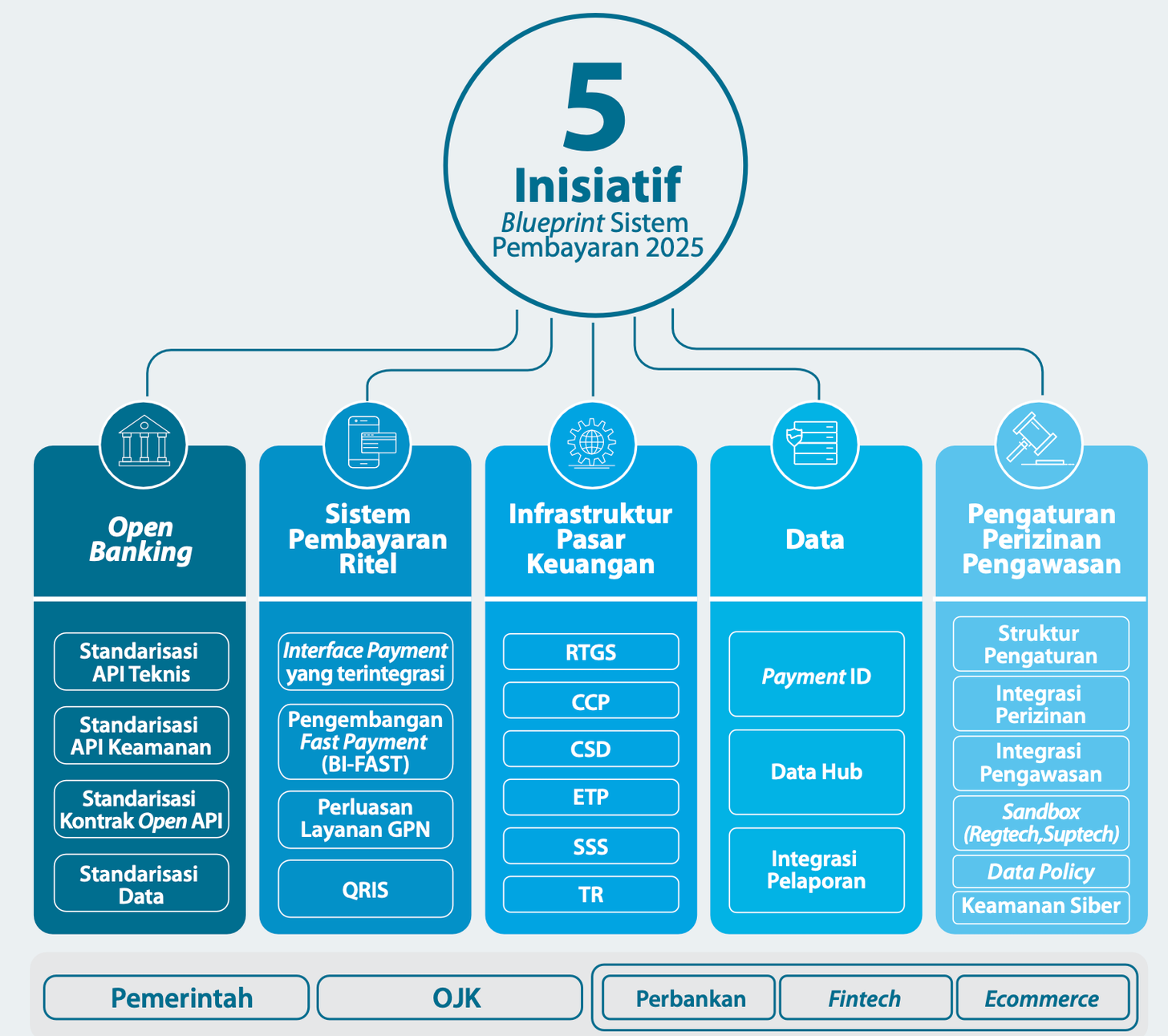

The Roadmap

- API-based Open Banking

- Standardised API Specifications

– Protocol: HTTPS

– Data format: JSON

– Architecture: REST - Standardised API Security

– Authorisation framework: OAuth 2.0

– Encryption: SHA-2/AES-256 - Standardised API Contract

- Standardised Data Format

- Standardised API Specifications

- Instant Retail Payment System

- QRIS: Standardised QR to accept/send payments (Launched in 2019)

- BI-FAST: real-time bank-to-bank settlement, eg. SG’s Fast, PH’s InstaPay, UK’s Faster Payment

- National Payment Gateway: Card-based interoperability between ATM, debit card, credit card, e-wallets via payment switches

- Universal Payment Interface: Middle-end module that glue all of the above together by providing ID proxy address & 2FA

- Financial Market Infrastructure

—

- Data Management (KYC, AML, Audit, Reporting)

- Proxy address BI-Fast, eg. SG’s phone number/UEN PayNow

- Reporting & audit

- Data Management

- Licensing, Regulatory, Monitoring

- Regulatory Sandbox

- Data Policy

- Cyber security

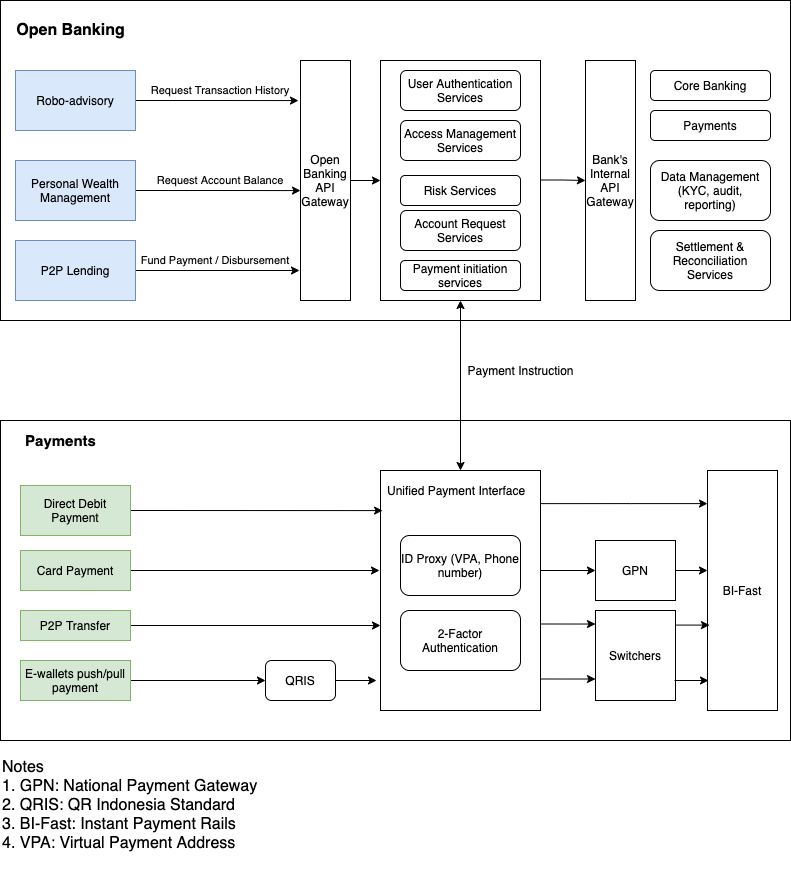

Putting All Things Together

Similar to other countries like Singapore and India, payments revolutions in Indonesia started with the idea of having an instant payment infrastructure to enable cheap & fast payments. The real benefits of all different projects is how it will collapse the payment process into a simplified and standardised like below diagram.

Some initiatives such as QRIS and GPN have simplified & standardised some of payment use cases such as pay-to-merchant (push & pull) and pull card-based transactions will benefit MSMEs by enabling unified cashless payment acceptance and low cost to process payments. With BI-FAST, now users can do peer-to-peer payment (push & pull) fast & cheap. All of these combined arguably pose an existential threat for international card schemes such as Visa & Mastercard alike.

For the government, an efficient payment system can help in executing various social payout programs such as Bansos effectively, directed, and affordable. As an effect, the barrier to adopt cashless tremendously lowered and financial inclusion will be boosted.

. . .

It is yet to be known the exact scope of all of mentioned initiatives. For BI-FAST, will fintech companies with certain license can participate? Can fintech companies partner with bank to get access to QRIS? How much transaction threshold will be processed with BI-FAST?

However, Bank Indonesia has emphasized in their 2025 Blueprint that their goal is to digitalise banks via a universal API to foster integration between Bank & Non-bank financial institutions while balancing data privacy, security, and customer’s protection.

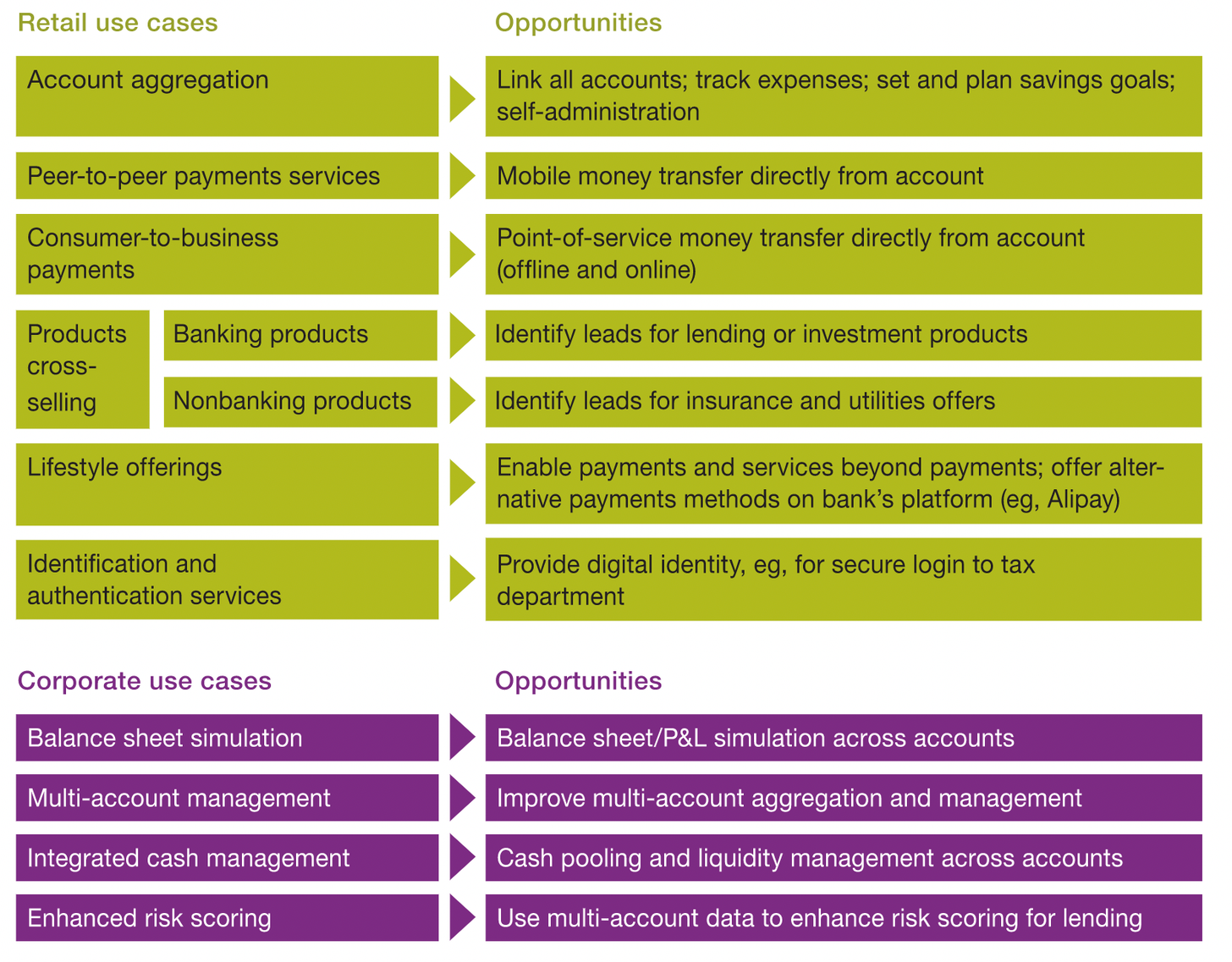

For fintech or technology companies in general, the democratisation of bank’s data poses great opportunities to create multitudes of new services & products. In the retail environment, data aggregation and instant payment will catalyse the embedded finance proliferation by further unbundling finance use cases in different value chains.

As the implementation of Indonesia’s Payment System unfold, there will be big winners and losers. With more than 17,000 islands, the biggest bottleneck remains in how to convert cash into a digitalised form. I’m optimistic that this evolution will bring waves of innovations that can truly transform Indonesian society at large.

. . .

Are there any other thoughts, features, perspectives that I miss? Feel free to reach out to me and I would like to understand more and incorporate it into future thesis.

Shout out for Mehul Mangalvedhekar and Yosua Nathanael for thoughts, inputs, and feedbacks.