")

Riding on the growth of ecommerce in Indonesia, where GMV has ballooned to US$40.1 billion after registering 91% growth in 2020, logistics players such as J&T Express have also experienced a surge in demand. While J&T recorded 2 million packages per day in 2020, this increased to 4 million per day in 2021.

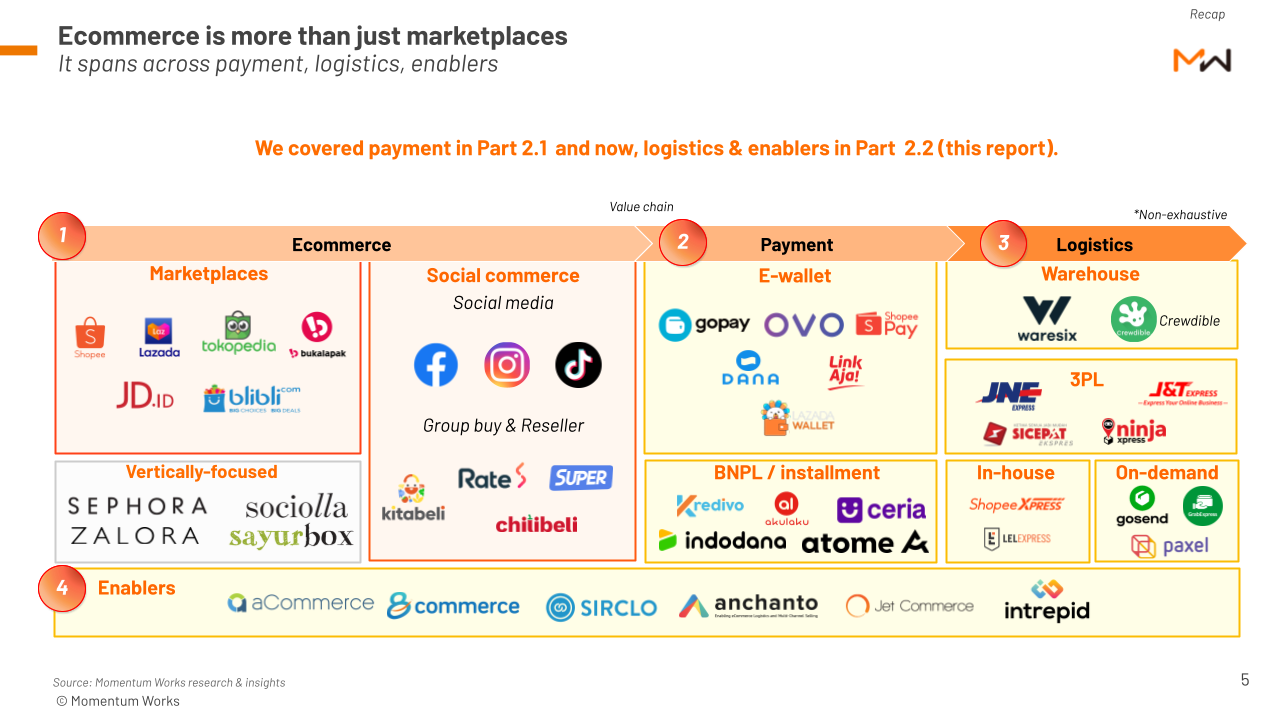

These are some of the insights in our latest ecommerce in Indonesia Blooming Ecommerce in Indonesia series. Titled “Part 2.2. Ecosystem – Logistics & Enablers“, we explored how Indonesia’s fragmented geography set the stage for the role and dynamics of different types of logistics players in Indonesia (third party logistics, on-demand and in-house).

We also looked into the ecommerce enablers, players that help brands to navigate complicated ecommerce operations, as well as help ecommerce platforms onboard more brands.

8 key insights from the report:

-

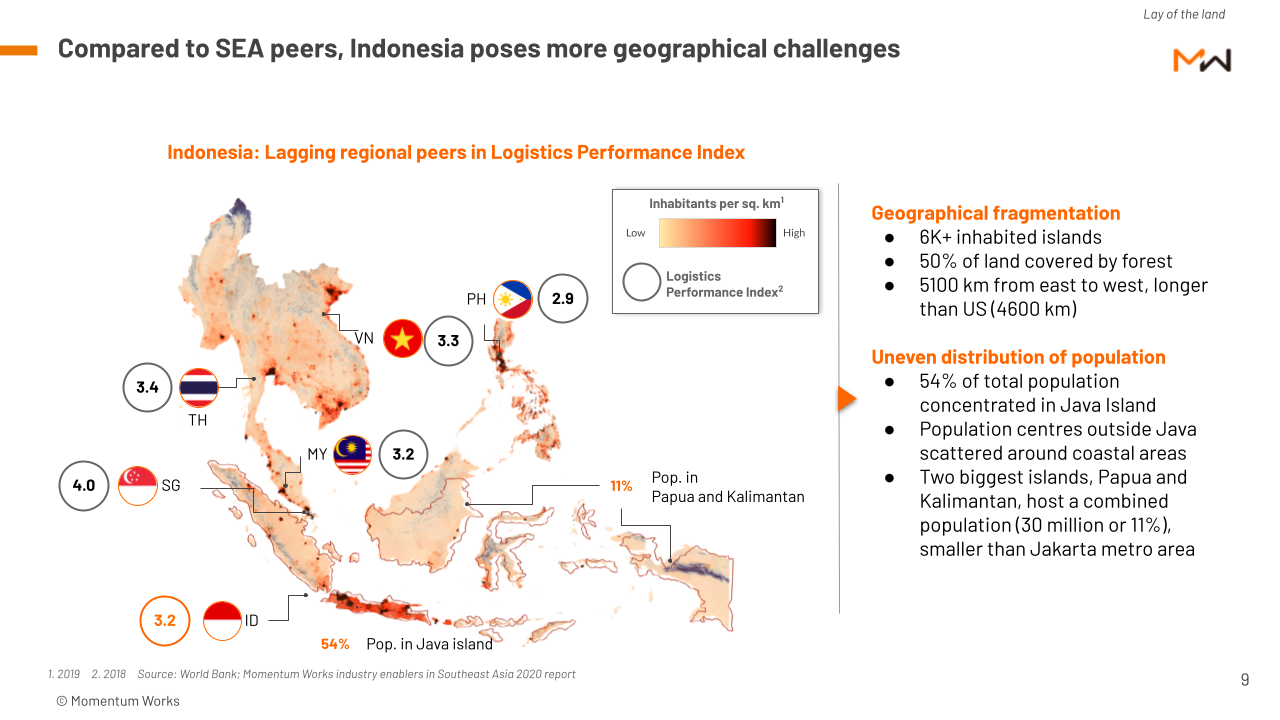

Indonesia logistics: More geographical challenges than other SEA peers

While Indonesia has more than 6000 inhabited islands, 54% of its people live in Java, with the remainder scattered across coastal areas. In terms of population numbers, the Jakarta metropolitan area alone is bigger than Indonesia’s 2 biggest islands (Kalimantan and Papua), contributing ¼ of the country’s GDP .

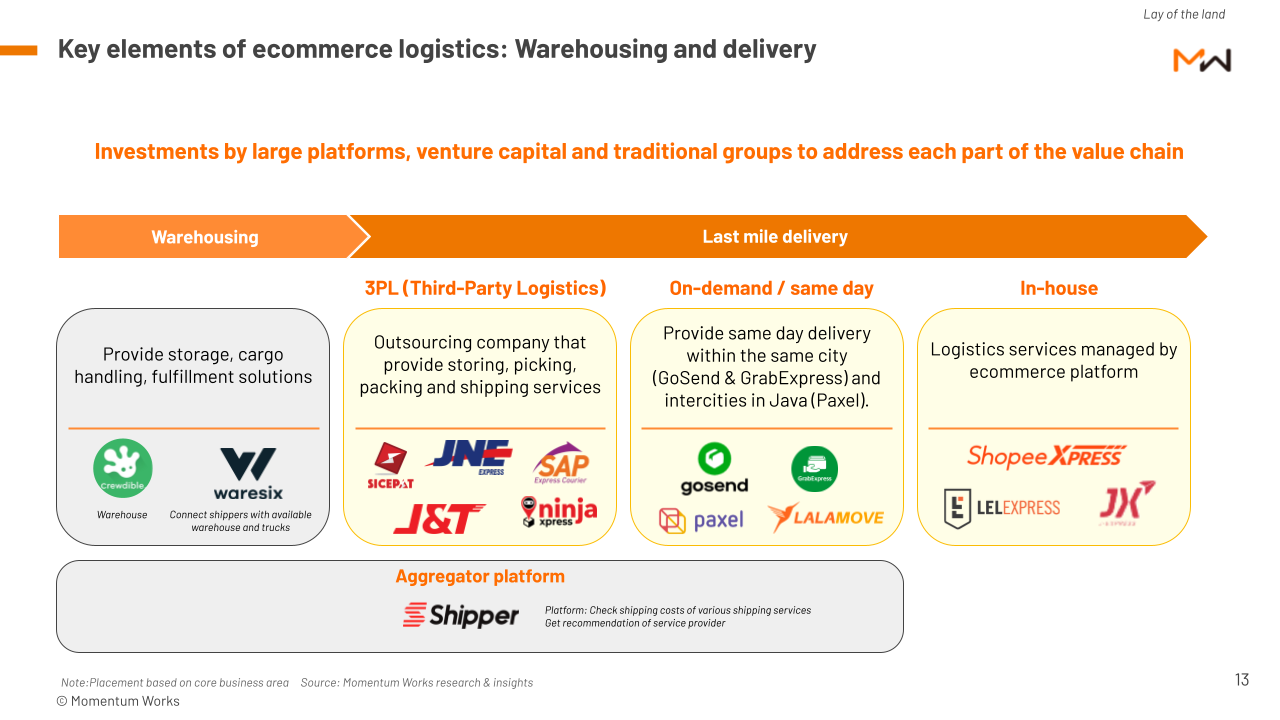

2. Key elements of ecommerce logistics: Warehousing and delivery

Warehousing and last mile delivery companies are essential components of making sure the goods that customers buy arrive at their doorsteps.

Warehousing is the storage point once the goods enter Indonesia, and there are various last mile delivery options that the supplier/ ecommerce platforms will use . These include third party logistics (3PL), on-demand logistics and in-house logistics managed by the ecommerce platforms themselves.

As you can see from the report, warehousing companies are still scarce – the barrier to entry is higher, but there are many players in the last mile delivery space. The strongest being third party logistics – J&T and JNE.

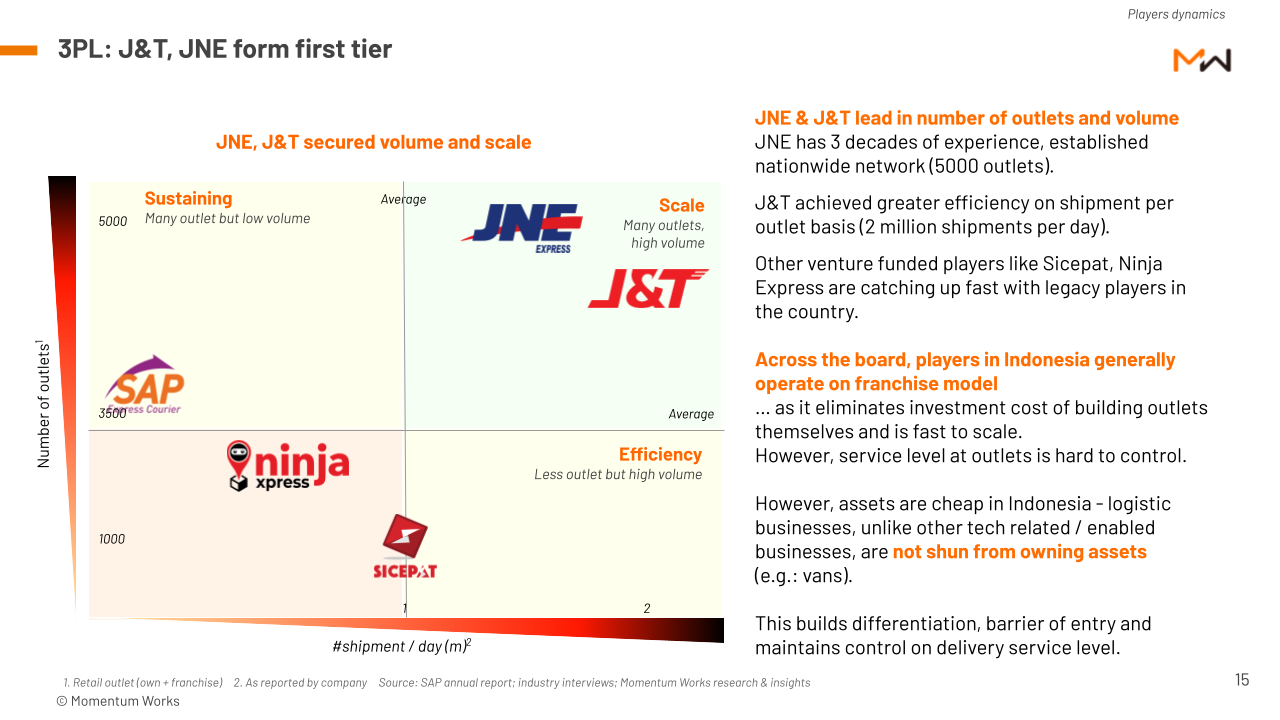

3. Third party logistics first tier players: J&T and JNE

JNE leads in terms of outlet, with 5000 outlets nationwide. J&T leads in terms of shipment per outlet efficiency with 2 million shipments per day. Most companies in this sector operate on a franchise model. It cuts their costs of building outlets while also being fast to scale.

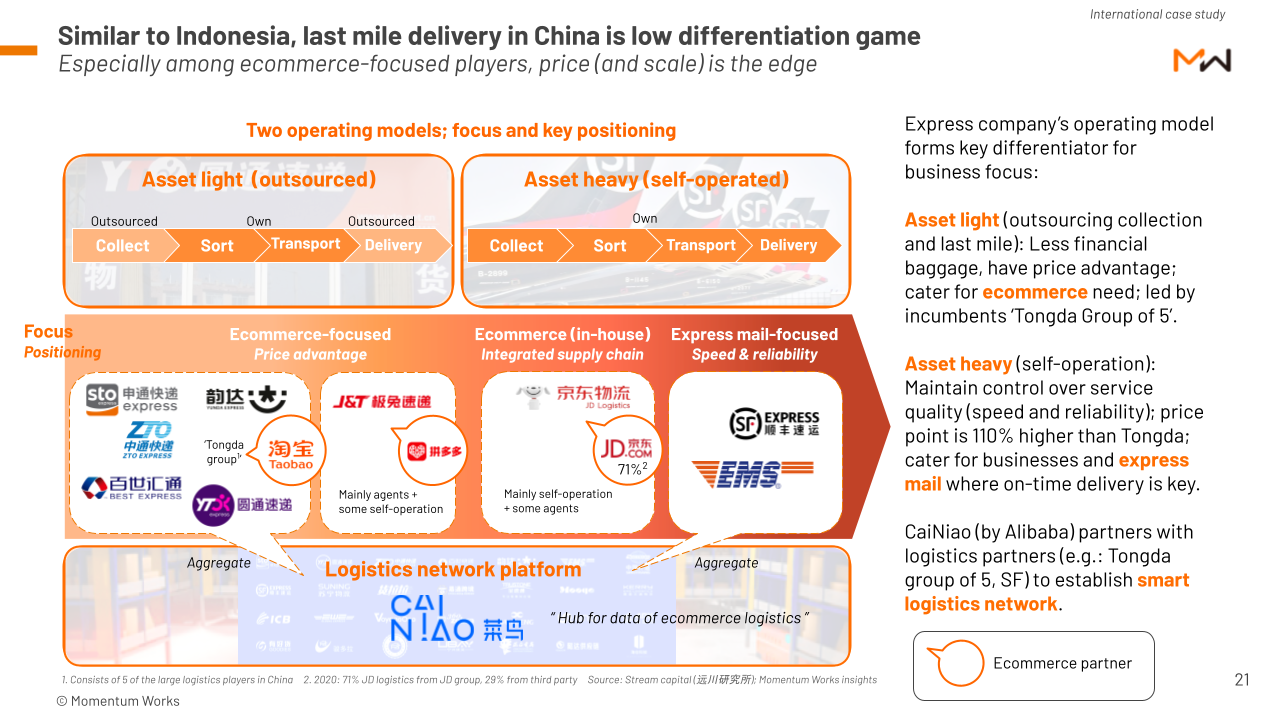

4. Last mile delivery in China is similar to Indonesia, i.e. it is a low differentiation game

In China, there are 2 operating models for delivery services: asset light model (franchise model) and asset heavy model (self-operation model).

Asset light model outsourced collection and last mile. This low cost model offers price advantage, catering to ecommerce players which need low logistics costs.

Asset heavy model built their own outlets and team for collection, sorting, transportation and delivery and ensures control over service quality.

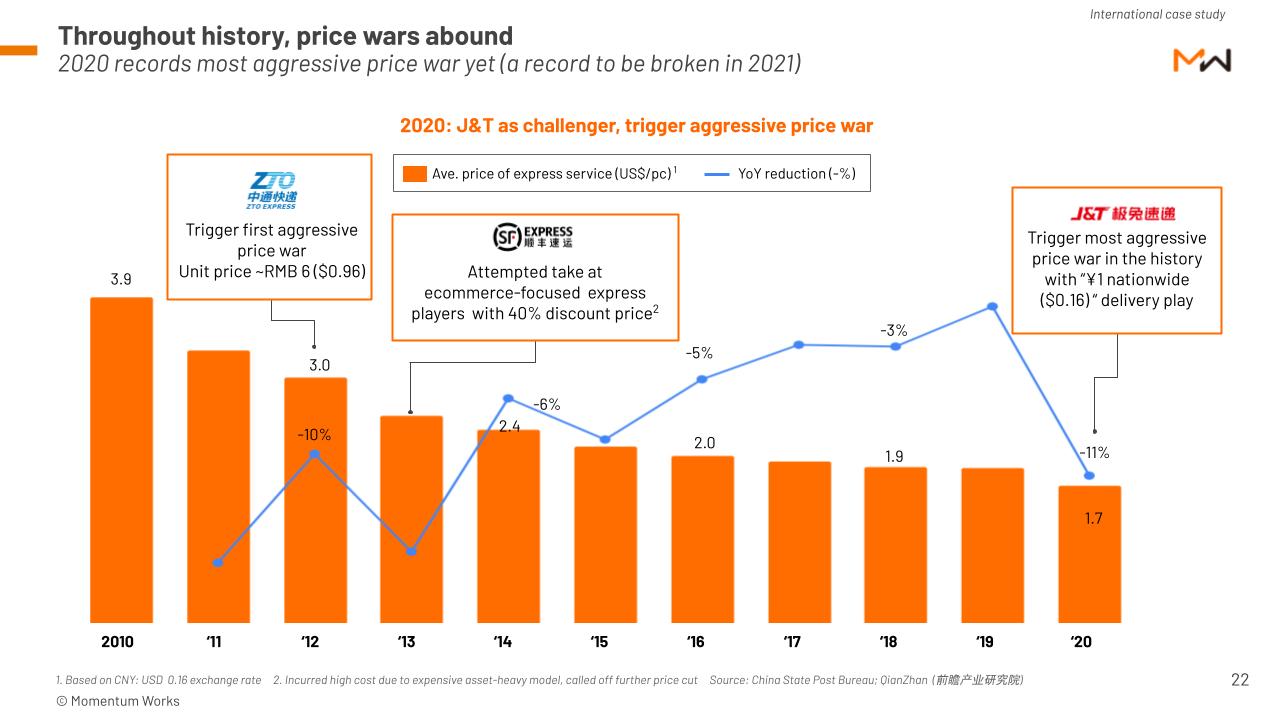

5. Throughout history of China’s logistics, price wars abound -and it is the same for Indonesia

In order to get more customers, the delivery companies have engaged in price wars. In China, 2020 recorded the most aggressive fight yet, with J&T offering nationwide delivery from Yiwu (city with largest delivery volume in China) for only $0.16/pc.

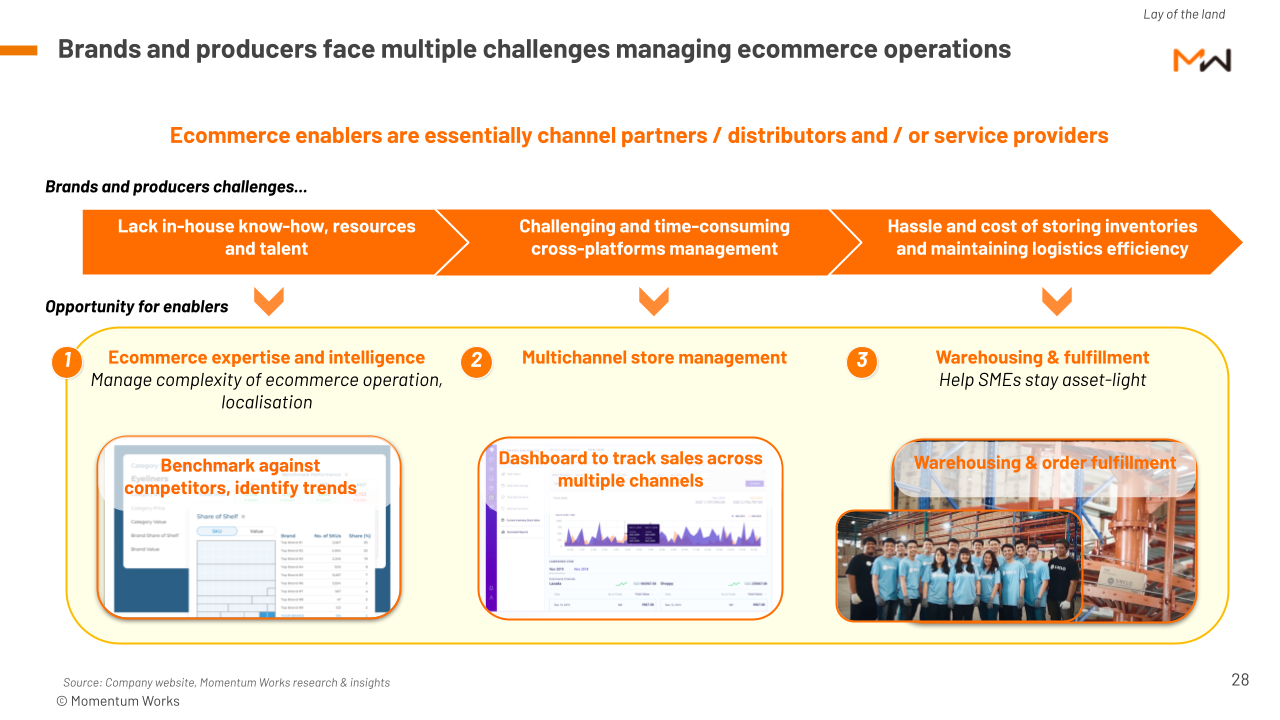

6. Brands and producers face multiple challenges managing ecommerce operations

Brands and producers often face challenges across the value chain. Ecommerce enablers are essentially providers that can help with the challenges. They can help manage complex ecommerce operations, multichannel store management, warehousing and can also help SMEs stay asset-light.

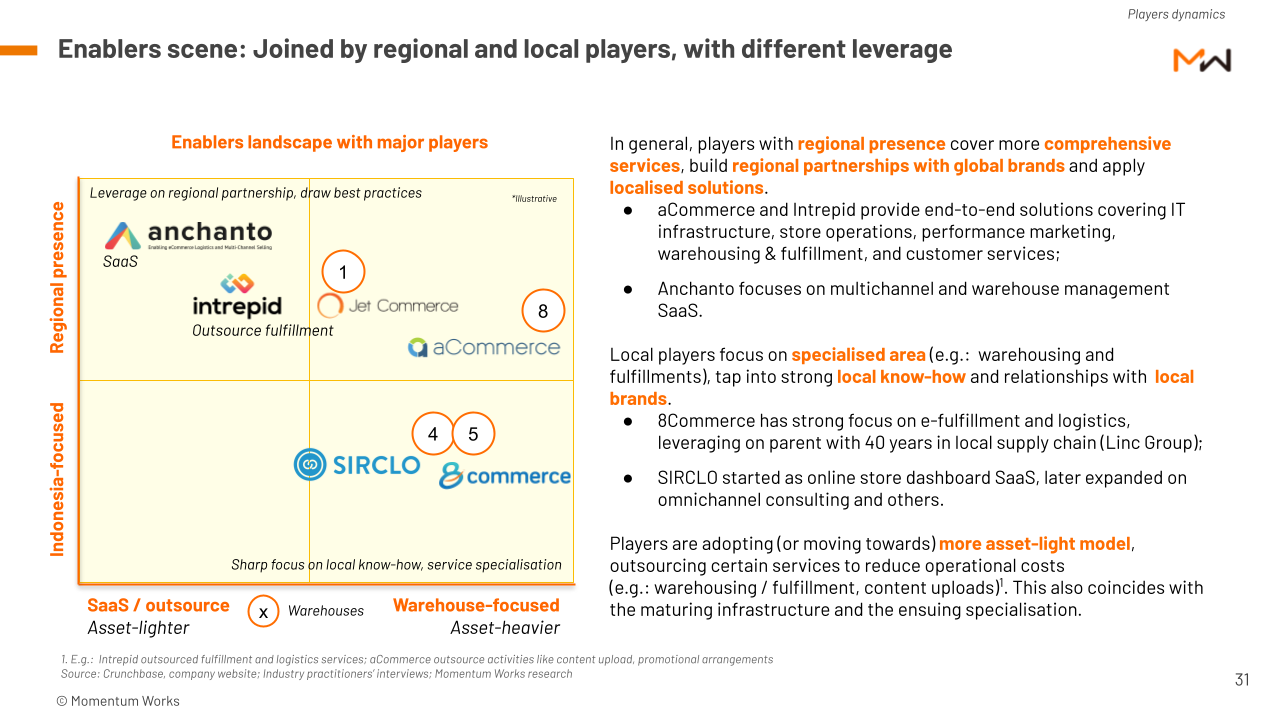

7. Enablers scene: Regional and local players have different leverage

Local and regional enablers target different customers and provide a variety of solutions and services.

Regional players like aCommerce and Intrepid provide end-to-end solutions that include IT, marketing, warehousing and customer services. Anchanto focuses on multichannel and warehouse management SaaS.

Local players like 8Commerce have a strong focus on e-fulfillment and logistics, whereas SIRCLO started with online store dashboard SaaS and later expanded into omnichannel consulting and others.

Most players are moving towards asset-light models to reduce operational costs.

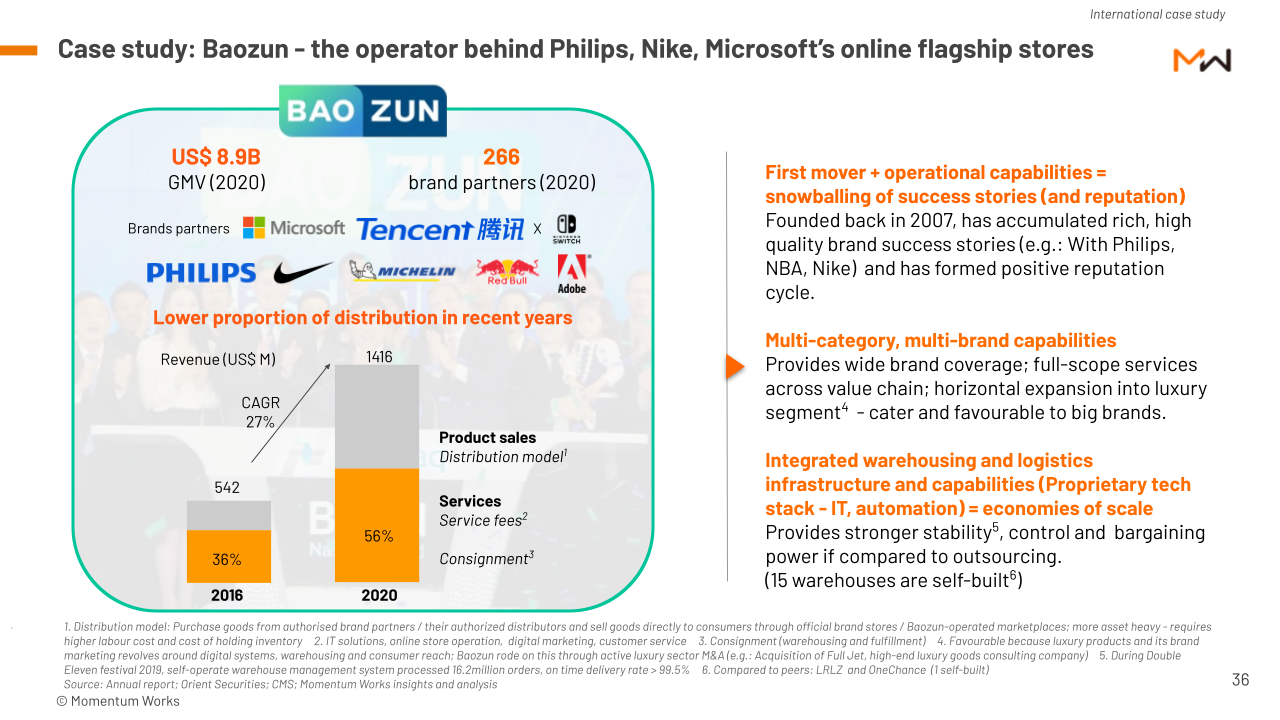

8. Case study: Baozun – the operator behind Philips, Nike, Microsoft’s online flagship stores

One of the global enablers recognized worldwide is Baozun, which has served international brands like Nike, NBA, and Philips. It provides multi-category brand coverage and full-scope services across the value chain – including warehousing and logistics infrastructure. It is one of the case studies on how an enabler can form a positive reputation cycle, and thus provide stability, control, and bargaining power.

Get the full report here.

If you have not read our other reports in our Blooming Ecommerce in Indonesia series, check out Marketplace and Ecosystems: Payments reports as well.