The increasing household expenditure and the underdeveloped consumer lending industry create huge demand and growth potential for consumer finance in Indonesia. While hundreds of players are rushing in because of the clear opportunities, underlying risks must be weighted to ensure long-term success. This article, split into two parts, aims to provide readers an overview of consumer finance market in Indonesia, and to help investors and corporate innovators in their business evaluation.

Indonesia at a Glance

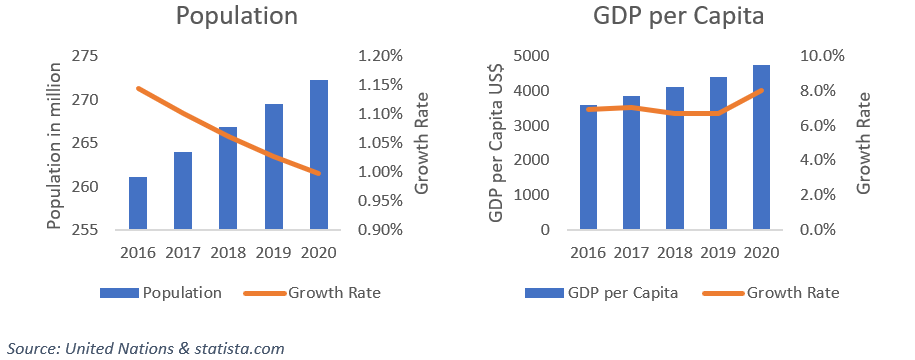

Indonesia is the largest economy in Southeast Asia by GDP (US$932 billion) [1], and the biggest market by population (264 million) [2]. While the population is expected to grow at over 1% annually [2], the GDP is expected to maintain the growth of 5% annually [3]. GDP per capita is US$3,859, and is expected to grow at a range between 6% to 10% annually for the next 5 years [4].

A growing labour force is expected to fuel income and spending in the near future. The total labour force in Indonesia is 129 million, about 49% of the total population, and has been growing at 1.5% annually on average [5]. The average household expenditure increased by 25% in 2017 year over year [6].

Digital Penetration in Indonesia

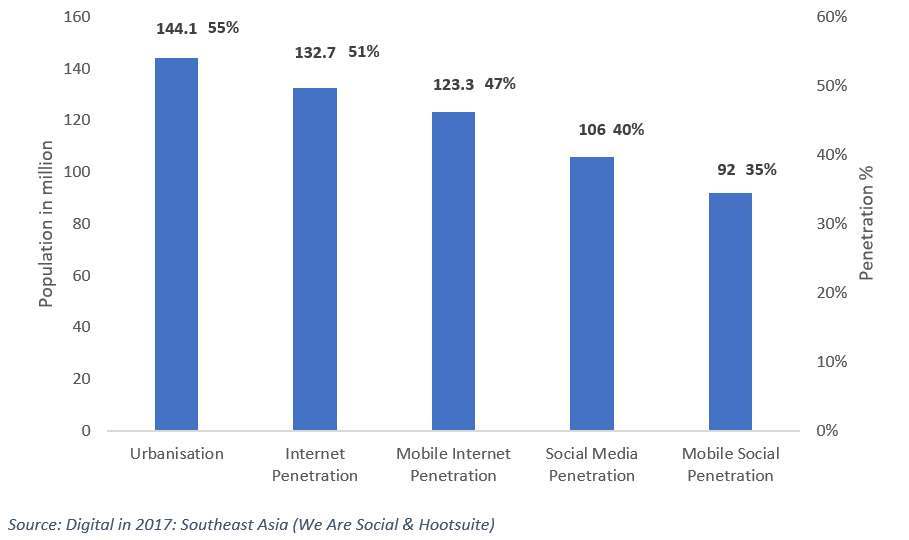

According to the report of Digital in 2017: Southeast Asia, urbanization in Indonesia sits at 55% with the annual rate of urbanization at 2.3% [7]. Indonesia has 132.7 million internet users, indicating a 51% internet penetration. At the same time, the growth is strong. In 2016 alone, new internet users climbed to 45 million, indicating a growth of 50% in a single year. Mobile internet penetration aligned closely with internet penetration, standing at 47%.

Social media is widely adopted by internet users with more than 100 million social media users (around 40% of total population) whereas mobile social penetration is at 35%. Both social media users and mobile social users had a huge growth in 2016, at 34% and 39% respectively.

Consumer Income and Spending Behaviour

Households are on the path of growing income. Upper- and middle-income households have been growing fast for the past few years. The number of households with a high annual income of more than IDR 120 million (Approx. US$8,900) is about 24 million, and is expected to grow at 5% annually [8].

The spending patterns among households differ by income level, especially for high income households. These high earners spend (as a percentage of income) much less on food and beverage, but more on welfare and savings, leisure and holidays, and credit card Instalments. They also spend more on household appliances, digital and electronics products.

Although the rate of penetration is decent in internet, mobile and social media, digital media has a comparatively insignificant place among the preferred sources of information for products. Indonesians place their trust mostly on TV advertisements, in store promotion, friends, relatives and colleagues, and outdoor ads. Such insights reveal the challenges and direction of communicating with consumers in Indonesia.

Consumer Finance Market

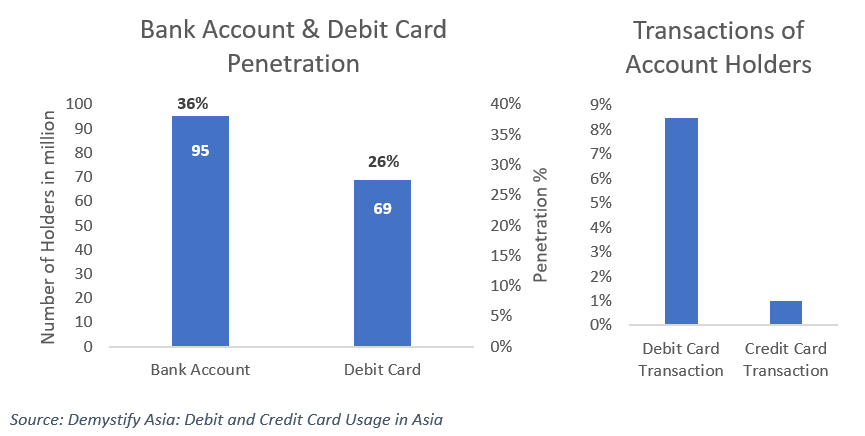

Penetration of traditional financial services (offered by banks and other institutions) is rather low. Only 36% of the population have bank accounts, while only 26% of the population own debit cards. Among those accounts, only 8.5% use debit cards and 1% use credit cards for transactions [9]. Bank branch coverage per 100,000 people is only 17.39, one-sixth of that in Europe [10].

The percentage of adults who have a registered mobile money account is even lower, at 0.7% [11]. However, the awareness of mobile money services has increased from 8% in 2015 to 15% in 2016 [11]. In contrast, “arisan” (a form of Rotating Savings and Credit Association in Indonesian culture, a form of Microfinance) seems to be one of the preferred financial service provider for unbanked population. It is reported that 22% of Indonesian adults have used an arisan [11].

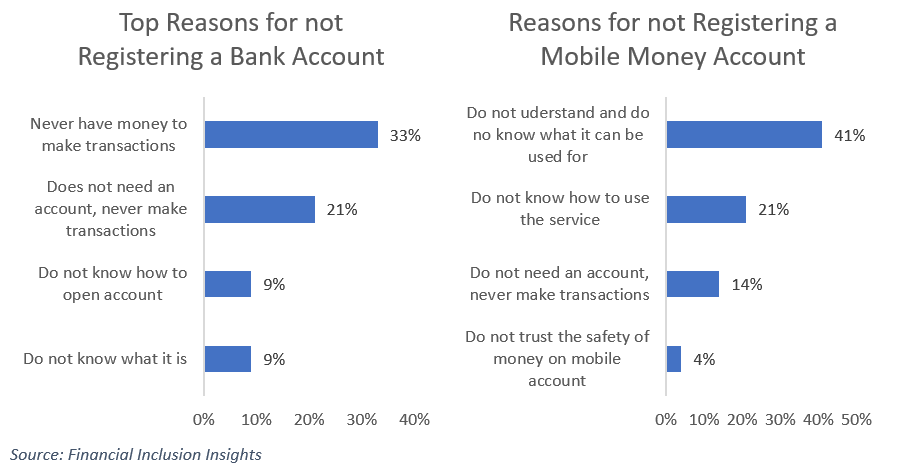

The reasons for both not registering a bank account and not registering a mobile money account associate with: the insufficient funds to do so, the lack of need for transactional services offered, and the knowhow of opening accounts. While mobile money account posts an additional challenge of consumers’ trust in the service providers.

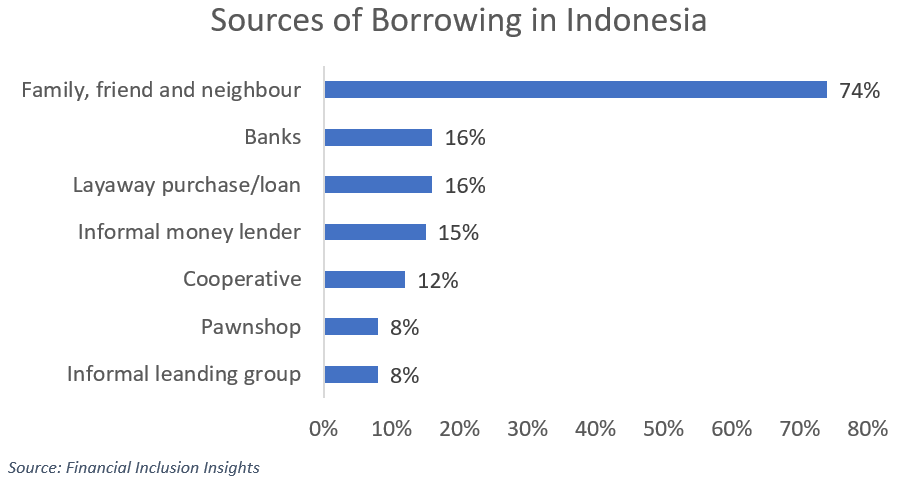

While the penetration of traditional financial services is low, the demand for loans is high. About 48% of Indonesian adults have ever taken a loan [11]. However, the majority of the transactions are on informal channels as listed below:

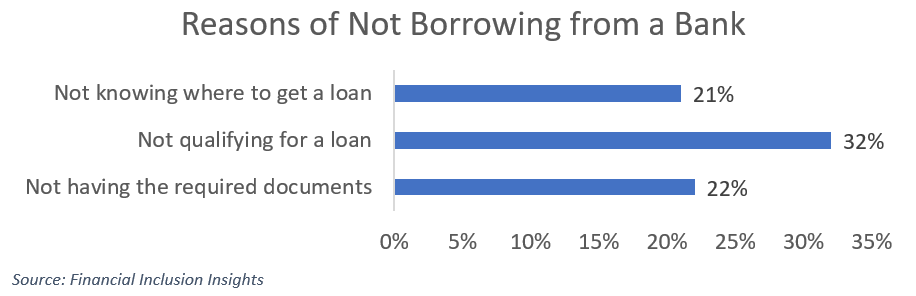

The reasons of not borrowing from a bank are: not having the required documents, not qualifying for a loan, and not knowing where to get a loan.

In Part 2 of this article, we will explore the regulatory environment, identify key players, analyze opportunities and risks, and give recommendations to investors and foreign companies.

References

- World Bank Data: Indonesia GDP (current US$)

- United Nation Population Prospect 2017: Indonesia Population

- Indonesia: Gross domestic product (GDP) in current prices from 2012 to 2022 (in billion U.S. dollars), www.statista.com

- Indonesia: Gross domestic product (GDP) per capita in current prices from 2012 to 2022 (in U.S. dollars), www.statista.com

- World Bank Data: Indonesia, Total Labour Force

- Deloitte Consumer Insights: Embracing bricks and clicks in Indonesia 2017

- Digital in 2017: Southeast Asia

- Deloitte Consumer Insights: The evolution of the Indonesian consumer 2016

- Debit and Credit Card Usage in Asia, www.demystifyasia.com

- Indonesia Turn to E-Payment Services as the Sector Takes the Lion’s Share in Local Fintech Market, ww.fintechranking.com

- Financial Inclusion Insights – Indonesia Wave 3 Report FII Tracker Survey 2017