The mobile payment market in Vietnam is in what we call a Wild West phase, and there is still the opportunity for any given player to become the dominant one. However, there are plenty of challenges.

Cash is still king

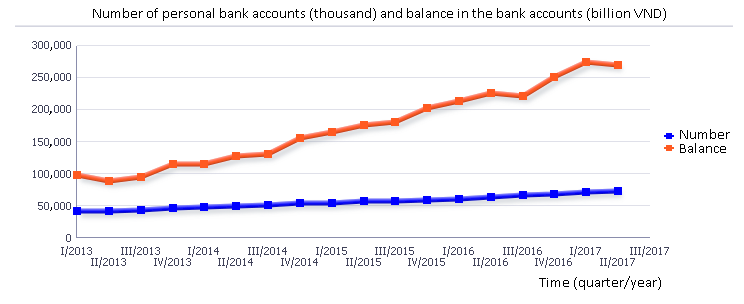

Bank account ownership in Vietnam is still low at 59% of the adult population (aged over 15), according to result of a survey by the State Bank of Vietnam – the country’s central bank revealed on December 7, 2017 at the Vietnam Retail Banking Forum 2017.[1]

This is an increase from the 31% figure as estimated by the World Bank in 2014.[2] However this number is still lower than the world average in 2014 of 62% according to World Bank data.[3]

Chart 1: Number of personal bank accounts (thousand) and balance in the bank accounts (billion VND) by the quarter (source: SBV) (VND1 billion=US$44,000)*

*The number counts multiple accounts by one individual.

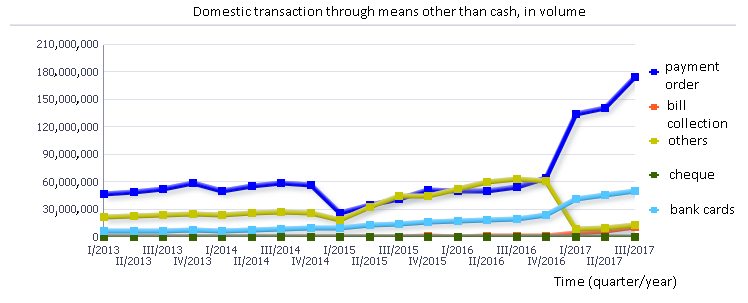

In terms of number of transactions, payment using a bank card is slowly gaining popularity, seeing the most significant increase so far in the first quarter of 2017.

Chart 2.1: Domestic transaction through means other than cash, in volume (source: SBV)

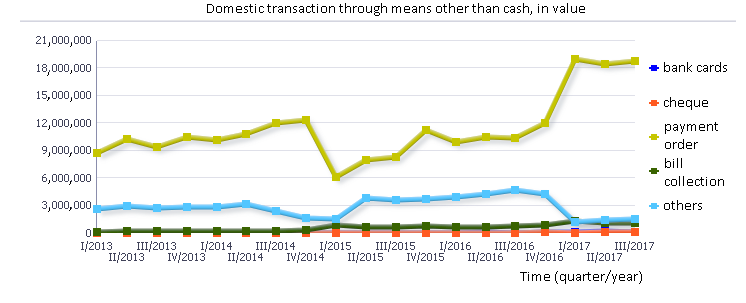

Chart 2.2: Domestic transaction through means other than cash, in value (billion VND) (VND1 billion=US$44,000) (source: SBV)

Others include bill of exchange, promissory notes, domestic letter of credit, SMS Banking, Mobile Banking, Phone Banking, Internet Banking, transfer from Current Account,…

In terms of value, bank cards still account for a small percentage, while transaction through other means decreased.

Chart 4.1: Transaction through ATM/POS by volume

![]()

Chart 4.2: Transaction through ATM/POS by value

![]()

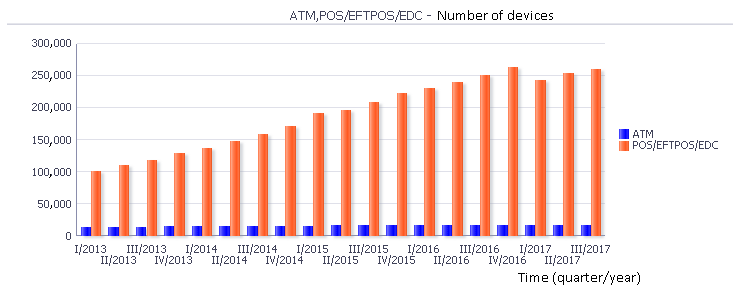

Chart 4.3: Number of equipment ATMs/POSs

The number of bank accounts and thus debit cards increased, as well as the number of ATMs, but most people use their debit cards to withdraw cash at the ATMs. At the 2017 annual conference of the Vietnam Bank Card Association, the association revealed the statistics that 86.81% of transaction value through domestic debit cards is to withdraw cash. Cash withdrawn per ATM per year rose from VND60 billion (US$2,634) in 2012 to VND106 billion (US$4,653) in 2016.

Transaction value per POS in 2016 rose by 6 per cent on year, compared to 20% per ATM.[4]

One of the reasons for people’s reliance on cash is the fees attached with using debit and credit cards. Banks charge a fee to merchants allowing card payment based on value of the transactions. Some merchants pass it on to customers even though the law forbids that.[5]

Only in December 2014, the two biggest card alliances in Vietnam, Smartlink and Banknetvn (consisting of 35 and 19 banks respectively) merged to become the National Payment Corporation of Vietnam (NAPAS), with the aim to allow all POSs and ATMs to accept all cards by all the banks without users having to pay (high) additional fee. [6] At the moment 40 banks are in the NAPAS system and the additional fee has been decreased, in some cases to zero.[7]

State of mobile payment

At the moment, the mobile payment market is fragmented, with numerous players providing the same services, with their own separate alliances of stakeholders (users and merchants), and none of them being a dominant player.

Banks’ mobile banking apps have the basic functions including checking balance in bank account, transferring money within one bank and among banks, and payment of utility bills, phone top up and credit cards. Some banks’ mobile banking apps allow QR payment at merchants that these banks have an agreement with. As of December 10, 10 banks namely BIDV, VietinBank, Agribank, Vietcombank, ABBANK, SCB, IVB, NCB, SHB, Maritime Bank with 7 million customers united in a QR system of their own. This is 10 out of 35 domestic banks and 51 foreign banks with operation in Vietnam.[8]

Wallet apps, which either connect to user’s bank account at some banks they have relationship with and Visa/Mastercard/JCB cards or allow top up from banks they don’t or in the form of cash, allow transfer to other users of the same app, payment of utility bills, phone top up and payment to some merchants and credit card-issuing banks and consumer finance companies they have a relationship with, and QR payment at merchants they have a relationship with.

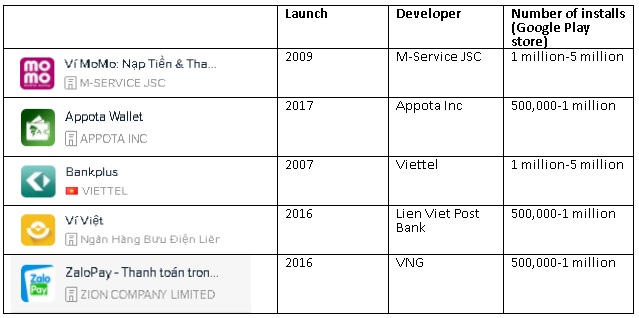

Chart 5: Ranking of wallet apps in Vietnam, according to App Annie, ranking retrieved on Dec 04, 2017

*can be used by feature phones

**for distributors of Viettel products (game cards, phone top up cards) with functions particular for them such as management of agents under them.

***These four apps allow you to put money in your phone account, and buy game cards or give money to your friends’ phone and game accounts

****for people in South Korea to transfer money to people in Vietnam

Chart 6: Overview of top 5 payment apps

In the top 100 finance apps, besides the 20+ mobile banking apps provided by the banks, there are 23 payment apps, which means a sea of choices for users.

As assessed by Can Van Luc, advisor to the board of Bank for Investment and Development of Vietnam, the biggest bank in Vietnam in terms of total assets, none of them is popular enough to achieve economies of scale. And then the micro division of the market into partnerships and alliances, with different QR systems, make users feel inconvenient and thus hesitate to use.[9]

Government policy and regulations

In terms of policy, the government always say that they want the country to go cashless. On December 30, 2016, the Prime Minister signed Decision 2545/QD-TTg to ratify the project to develop cashless payment in 2015-2020.[10] The decision names multiple targets for the end of 2020.

Chart 7: Vietnamese government’s 2020 cashless targets

| End of quarter III/2017 | End of 2020 target | |

| Currency (paper money) in circulation as part of money supply | 11.47% | <10% |

| Number of POS | 260,187 | >300,000 |

| Number of transactions through POS | 39.4 million | ~200 million |

| Percentage of population over 15 with bank accounts | 59% | >=70% |

According to the decision, the government will optimize the legal framework for cashless payment and issue some policies to incentivize cashless payment at government agencies and businesses.

Currently, third-party payment service providers are defined as organisations other than banks that are licensed by the State Bank of Vietnam to provide third-party payment service, and are regulated by Decree 101/2012/ND-CP and Circular 39/2014/TT-NHNN.

The decree details the process of applying for a license and requirements that service providers need to meet including to have a charter capital of at least VND50 billion (US$2.2 million), that the legal representative and employees have to have “professional capacity”, the technical infrastructure has to meet the SBV’s requirements, and requirements on the internal process of carrying out the service, among others.[11]

The circular details requirements on the rights and responsibilities of stakeholders in the payment process and regular reporting for service providers. Notably, the e-wallet service provider cannot issue credit, or pay interest on the balance or any action that would result in the increase in the value of money stored in the wallet. In addition, the topping up or withdrawal from the e-wallet has to be carried out through the customer’s bank account.[12]

Where opportunities lie

Companies of diverse fields are investing in e-wallet apps.

Standard Chartered and LienVietPostBank pumped money into Momo and Viviet. Conglomerate FPT, which has presence in retail, software development, and content, launched the FPT Wallet (Senpay) in 2016. SEA has Airpay.

Content provider VNG,VTC have ZaloPay and VTC ePay. All the three major telecom service providers, namely Viettel, Mobifone and Vinaphone have their own apps, Bankplus, Vimo and MegaCard respectively.

New players have also emerged. In November 2017, Ant Financial, Alibaba’s financial services arm, signed a memorandum of understanding with NAPAS that will enable Chinese travelers to use Alipay throughout Vietnam via NAPAS member banks and its intermediary payment service networks, and in the future those who hold cards issued by NAPAS bank members in Vietnam will be able use Alipay to make purchases across Alibaba Group’s e-commerce websites, including AliExpress and Taobao.[13]

Also in November, China’s Tenpay Payment Technology announced its cooperation with the e-wallet service provider VIMO to launch WeChat Pay e-wallet service in Vietnam to make it convenient for Chinese tourists to pay for goods and services here in the country.[14]

As there is no dominant player yet, investors can try injecting money in one of the existing players to help it strike up as many partnerships with banks and stakeholders, such as merchants, as possible in order to create the network effect. However, it may take many years (and lots of investment) until a couple of dominant players remain.

Challenges

As players explore opportunities, it’s important to keep in mind the challenges.

Awareness is one of them. In September, Samsung unveiled Samsung Pay in Vietnam. Thomas Ko, Samsung Pay’s Global General Manager, said the only hurdle is consumer awareness, and that stakeholders including banks, government agencies, and companies have to join in to raise awareness of the advantages of using mobile payment. [15]

Legal is another. According to Ko, Samsung Pay is not a third-party payment service provider but currently the Vietnamese legal system only covers third-party payment service providers, causing “confusion for both Samsung Pay and partners” in the process of rolling out Samsung Pay.

A senior official from Sacombank said that consumers are still not convinced of the safety of cashless payment.8

Mobile internet is still not popular enough. For those who do have data, the experience is not optimal. As of January 2017, according to Wearesocial, percentage of mobile connections that are broadband (3G and 4G) is 30%. Average speed is 3,419 kbps. To put in perspective, the respective figures for Singapore is 99% and 8,521 kbps.[16]

Conclusion

We recommend that any player who wants to enter the Vietnamese payment market should pay attention first to the challenges, including those that are quite out of their control such as infrastructure and legal framework.

—

Reference

[1]https://kinhdoanh.vnexpress.net/tin-tuc/ebank/ngan-hang/ngan-hang-nha-nuoc-59-nguoi-dan-co-tai-khoan-ngan-hang-3681227.html

[2]https://blogs.worldbank.org/voices/vietnam-s-financial-inclusion-priorities-expanding-financial-services-and-moving-non-cash-economy

[3]http://datatopics.worldbank.org/financialinclusion/

[4]https://www.sbv.gov.vn/webcenter/portal/vi/menu/trangchu/ttsk/ttsk_chitiet?leftWidth=20%25&showFooter=false&showHeader=false&dDocName=SBV286994&rightWidth=0%25¢erWidth=80%25&_afrLoop=218625263829000#%40%3F_afrLoop%3D218625263829000%26centerWidth%3D80%2525%26dDocName%3DSBV286994%26leftWidth%3D20%2525%26rightWidth%3D0%2525%26showFooter%3Dfalse%26showHeader%3Dfalse%26_adf.ctrl-state%3D16k3864jgg_299

[5]https://tuoitre.vn/ca-the-van-bi-thu-phi-586827.htm

[6]http://baochinhphu.vn/Thi-truong/Sap-nhap-2-lien-minh-the-lon-nhat-Viet-Nam/216704.vgp

[7]https://timo.vn/blog/thu-vien-timo/tong-hop-ngan-hang-thuoc-he-thong-napas/

[8]http://ttvn.vn/kinh-doanh/thong-nhat-chuan-qr-code-cho-he-thong-ngan-hang-huong-di-cho-thanh-toan-di-dong-tai-viet-nam-42017812194942889.htm

[9]https://vepf.vnexpress.net/tin-tuc/ly-do-khien-nguoi-viet-con-ngai-thanh-toan-qua-di-dong-3665735.html

[10]https://thuvienphapluat.vn/van-ban/Tien-te-Ngan-hang/Nghi-dinh-101-2012-ND-CP-thanh-toan-khong-dung-tien-mat-152166.aspx

[11]https://thuvienphapluat.vn/van-ban/Tien-te-Ngan-hang/Nghi-dinh-101-2012-ND-CP-thanh-toan-khong-dung-tien-mat-152166.aspx

[12]http://www.moj.gov.vn/vbpq/lists/vn%20bn%20php%20lut/view_detail.aspx?itemid=29722

[13]http://vneconomictimes.com/article/banking-finance/approval-given-to-alibaba-s-online-payment-platform

[14]http://english.thesaigontimes.vn/57052/WeChat-Pay-e-wallet-launched-in-Vietnam.html

[15]https://vepf.vnexpress.net/tin-tuc/thanh-toan-khong-tien-mat-viet-nam-dang-thay-doi-rat-nhanh-3670816.html

[16]https://www.slideshare.net/wearesocialsg/digital-in-2017-southeast-asia