Yesterday, US food delivery market leader DoorDash announced the winding down of Deliveroo and Wolt operations in four countries: Qatar, Singapore, Japan, and Uzbekistan.

DoorDash completed the acquisition of UK-based Deliveroo in 2025. It had bought Finland-based Wolt earlier in 2022.

This time round, the exit of Deliveroo in Singapore caught the attention of many around us, as Momentum Works is Singapore-based and we have been following the sector in Southeast Asia closely for many years.

Deliveroo has been operating in the country since 2015, although in recent years it has largely retreated into focusing on the more premium sector, instead of competing for the mass market with market leaders Grab and Foodpanda.

Some thoughts here:

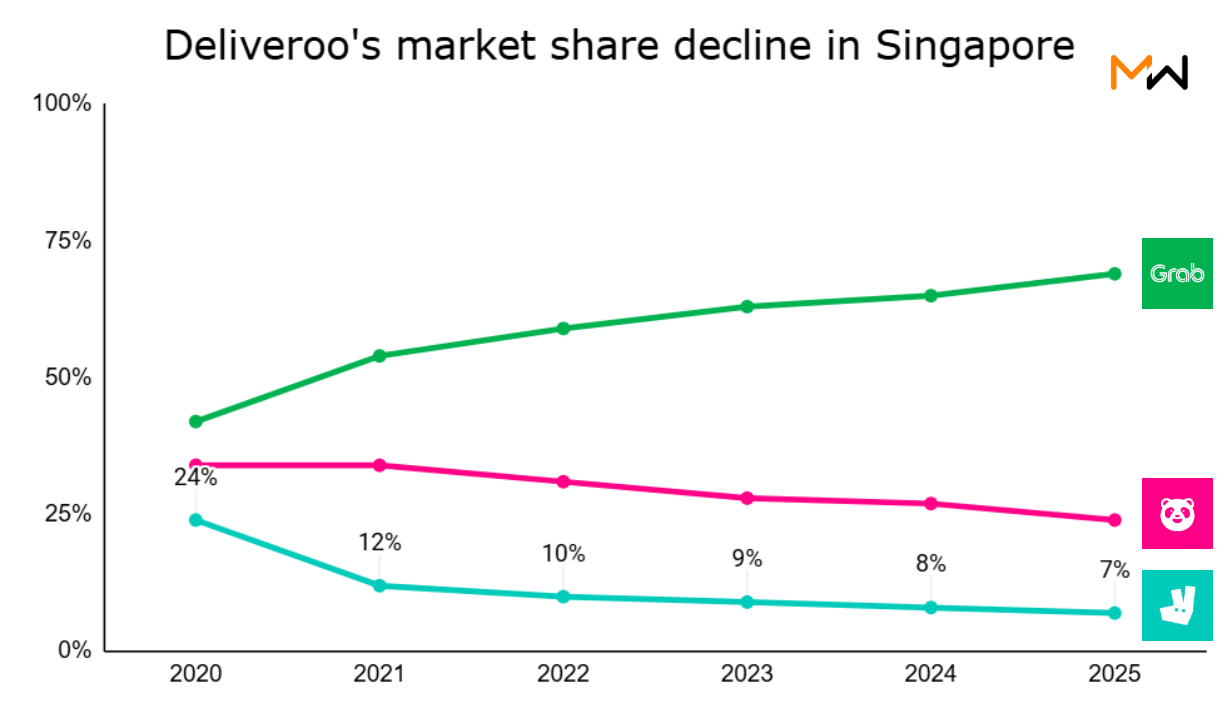

- This is not a surprise at all. We have been tracking the market share of key players in Singapore, where Deliveroo gradually declined from 24% in 2020 to 7% in 2025. While Deliveroo had built a loyal base of premium users and secured some exclusive merchant relationships, such positioning alone is rarely sufficient in a scale-driven platform business. Given its existing density and operational leverage, Grab is structurally well positioned to capture a meaningful share of the displaced demand;

- In fact, after Deliveroo’s withdrawal from Hong Kong in April 2025, some industry observers were already speculating whether Singapore would be the next. We do not know what was the exact reason why Deliveroo kept the Singapore market – but evidently some strategic decision needed to be made. For food delivery platforms, subscale positions decay over time. You either invest to win density – or you exit. There is no steady middle ground;

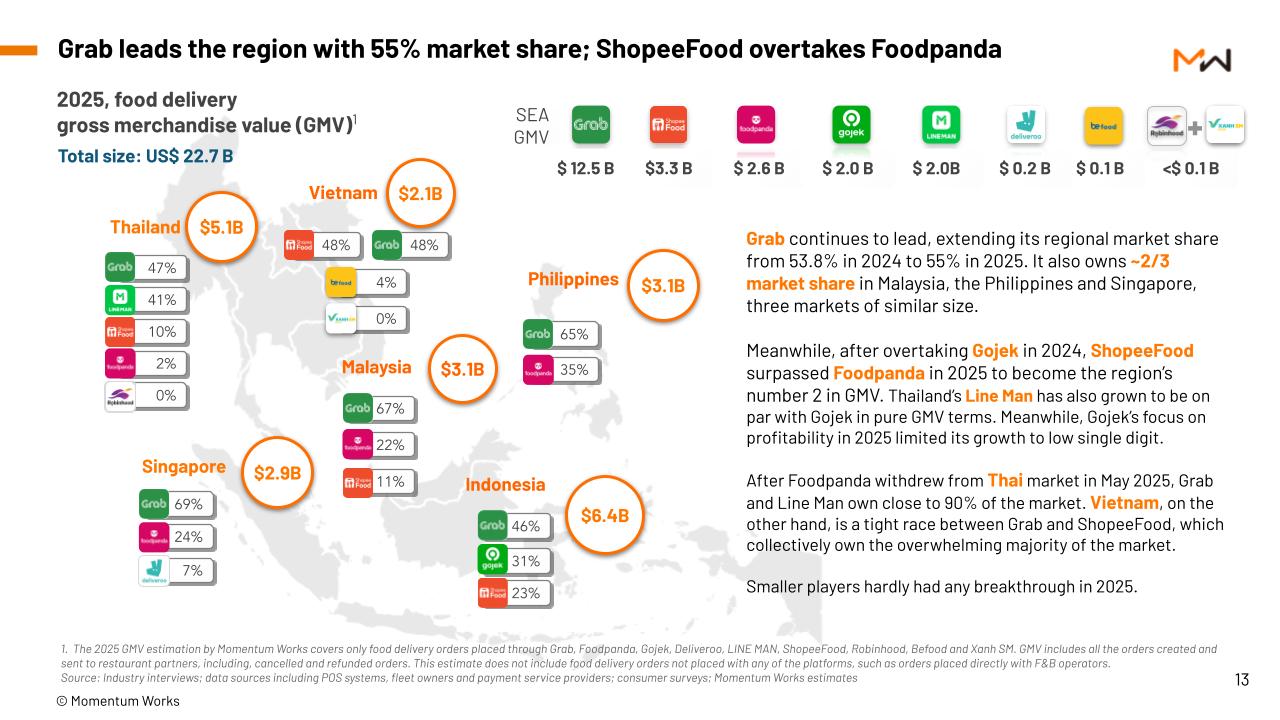

- Singapore is by itself not a small market – we tracked a total food delivery platform GMV of US$2.9 billion for 2025. That is 44% of Indonesia’s GMV – despite Singapore having only around 1/47 of Indonesia’s population. Of course, Singapore has its own set of challenges, notably the restrictions on foreign labour that could work as delivery riders;

- The market landscape in Singapore has been stable with Grab gradually extending its roughly two-thirds market share. It would take tremendous investment, or a vastly more efficient operating model, to disrupt the current landscape. It is pretty clear that DoorDash doesn’t think Deliveroo has that chance in the country;

- Singapore is not an isolated case. It is part of a broader portfolio rationalisation across global food delivery platforms;

- Will China’s Meituan enter the market? Or would ShopeeFood, which became the 2nd largest food delivery player in Southeast Asia last year, decide to launch in its home market of Singapore? We do not think such a large-scale launch in Singapore is likely this year as both companies have other, more pressing priorities;

- Another question is the fate of Foodpanda – which has lost quite a bit of market share in Singapore as well as across Southeast Asia, but nonetheless remains a sizable player. Earnings of DeliveryHero, Foodpanda’s parent, this Friday (27 Feb) might provide some clues. DeliveryHero’s attempt sale of Baemin, its profitable asset in South Korea, would give Foodpanda more room to breathe if executed successfully – but running operations across continents with limited operational synergy is a tough challenge for DeliveryHero, as well as for Deliveroo;

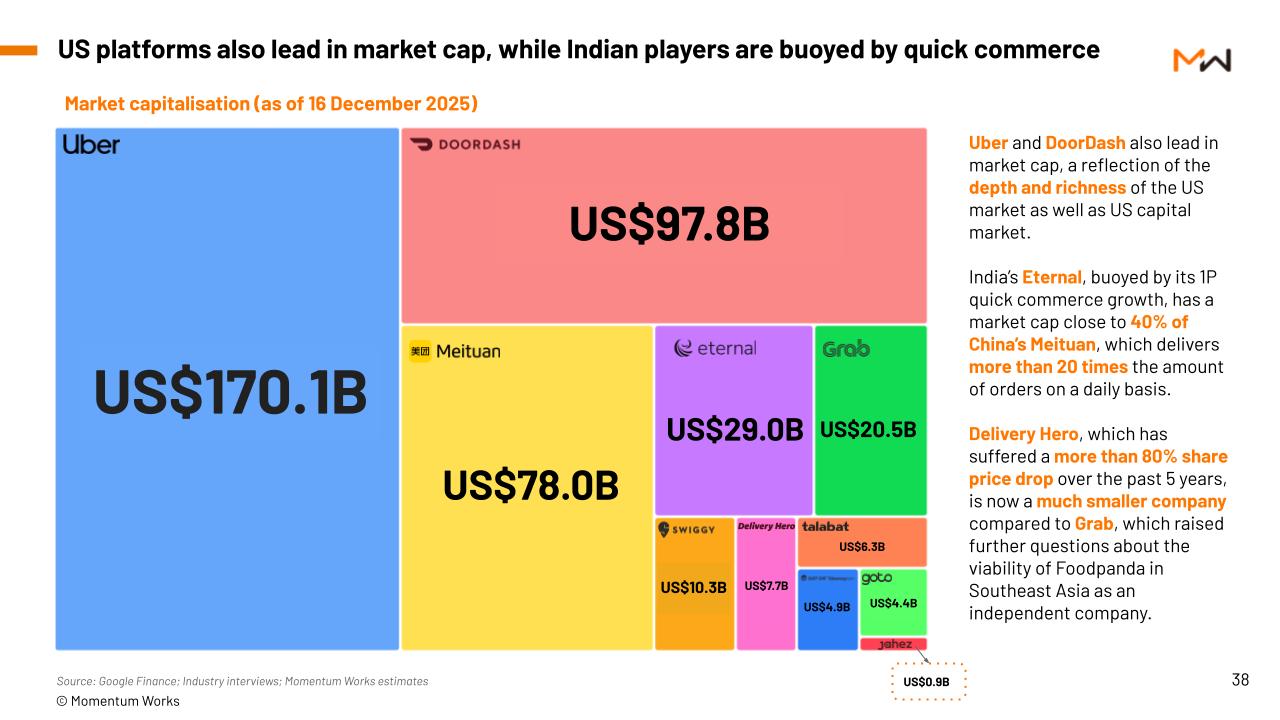

- We can’t say the same would be easier for Meituan (which is expanding in the Middle East and Brazil through Keeta) and DoorDash (having bought Deliveroo and Wolt). A scaled home market creates financial strength and operational muscle. But it also creates organisational inertia – standardised playbooks, centralised decision-making, and difficulty adapting to local nuance.

In any case, the rationalisation of global food delivery portfolios will continue to happen. The U.S. platforms have a significant advantage in terms of financial power, Chinese players including Meituan have refined operations in a way not seen elsewhere in the world, while Indian and Southeast Asian players have adapted their playbooks to strong local market circumstances.

The next phase of global food delivery will not be about expansion. It will be about portfolio discipline, capital efficiency, and operational localisation.

But there is another variable quietly reshaping the equation: Chinese F&B chains going global.

Many Chinese chains grew up in a hyper-competitive delivery market. They are used to platform-driven traffic, high operational intensity, livestream-led promotions, and data-driven menu iteration.

In overseas markets, these habits do not simply disappear. They either push local platforms to adapt – or create openings for Chinese platforms to enter alongside them.

When capital discipline from U.S. players, operational muscle from Chinese platforms, and local defensiveness from Southeast Asian incumbents intersect – we may see a reset of what “normal” looks like in food delivery.

Not every global champion will survive that test.