Will Delivery Hero – the Germany-headquartered global food delivery group sell Baemin, the leading South Korean platform it acquired in 2021?

Korean media reported on the sale attempt on 3 February, citing sources from investment banks. According to the report, Delivery Hero appointed J.P. Morgan late last year as sell-side advisor for Baemin and has since begun exploratory conversations with potential buyers globally.

Potential bidders mentioned include China’s Meituan, Singapore-based Grab, and U.S. mobility platform Uber. Domestically, Korean internet giant Naver has also been cited as a potential bidder.

Delivery Hero is reportedly valuing Baemin at between US$4.9-5.6 billion, implying a multiple of slightly over 10x annual operating profit.

From Startup to Cultural Icon

Baemin’s full name is Baedal Minjok (배달의민족), which literally translates to “the nation of delivery”. It was founded in 2010 by Kim Bong-jin (김봉진), an unconventional tech founder who actually came from a design background, having previously worked as a web designer at NHN (now Naver). Under Kim’s leadership, Baemin grew rapidly into South Korea’s dominant food delivery platform.

A side note, after the Delivery Hero acquisition, Kim and his core team spent time involved in the management of Delivery Hero’s Asian platforms – including Foodpanda. It was then the pink panda mascot, Pau-Pau, was unveiled. Compared with foodpanda’s earlier mascots, Pau-Pau definitely resonated more with the region’s cuteness-seeking consumers.

David Oh, a former C level executive of Baemin, wrote, “In its prime, Baemin was more than just an app; it was a cultural phenomenon. Known for its kitschy, quirky, and lovable brand identity, it was a purpose-driven company that breathed with the ecosystem – deeply understanding the delicate balance between merchants, users, and logistics partners. Its unique culture made it the undisputed top choice for Korea’s brightest tech talent.”

Kim himself was also widely respected within the company and across the ecosystem.

In 2019, riding the momentum of Korean capital and corporate expansion, Baemin entered Vietnam.

However, Vietnam’s consumer behavior and purchasing power were fundamentally different from South Korea’s, and without sustained investment, any market share gained can be quickly eroded. Baemin ultimately pulled out of Vietnam in 2023.

Delivery Hero Enters the Picture

In 2020, Delivery Hero announced the acquisition of a controlling stake in Baemin for US$4 billion. The transaction immediately attracted regulatory scrutiny in South Korea. To secure approval, Delivery Hero had to divest Yogiyo, then the country’s second-largest food delivery platform under its ownership. The Baemin acquisition dragged on for a year and was finally completed in 2021.

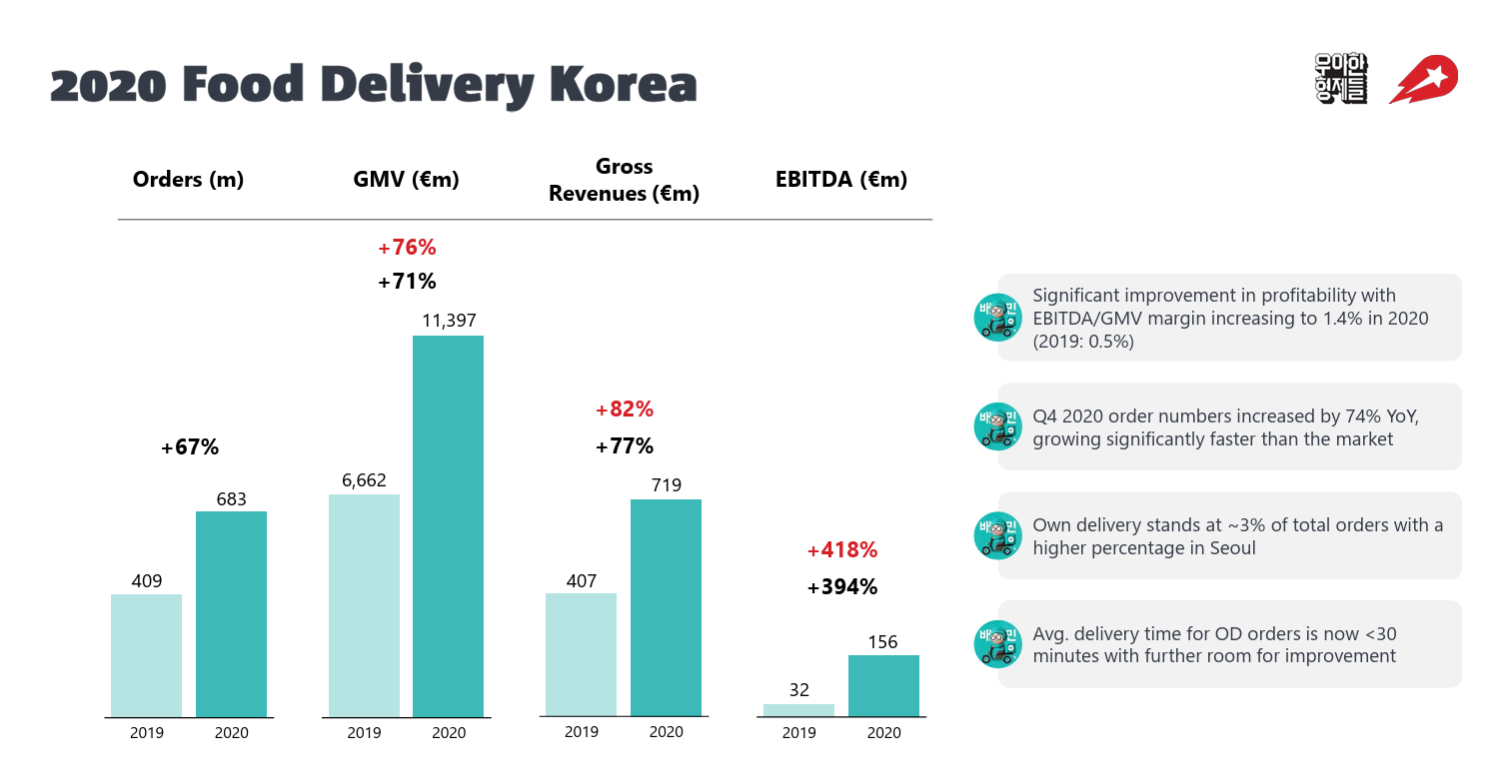

At the time of the acquisition, Delivery Hero disclosed Baemin’s financials. In 2020, Baemin’s Korean food delivery business generated €156 million (about US$137m) in EBITDA, but losses from quick-commerce operations and the Vietnam expansion largely offset overall profitability.

From that point on, Baemin gradually shifted from a country champion to a regional business unit executing a global strategy. Decision-making chains lengthened, response speed slowed, and sensitivity to local competitive dynamics diminished.

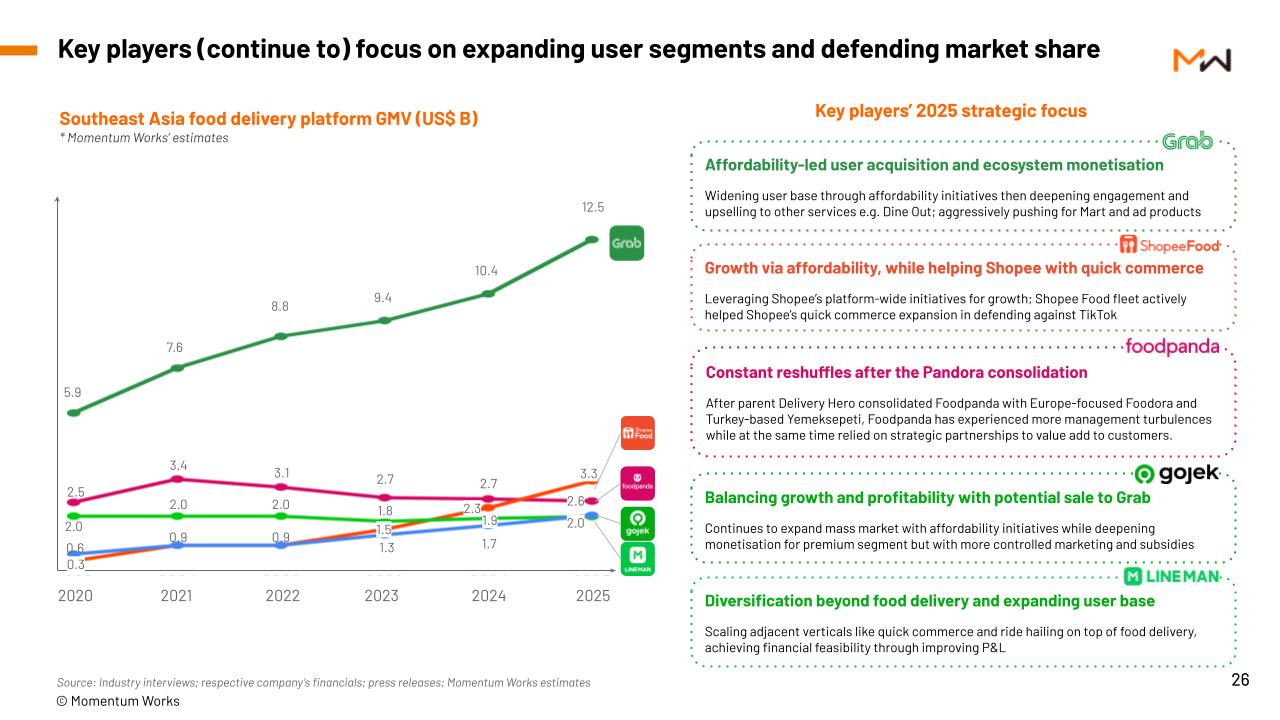

Meanwhile, profits from Korea were increasingly used to subsidise loss-making markets elsewhere. In Southeast Asia, Foodpanda’s market share fell from 22% in 2021 to 11.5% in 2025, with ShopeeFood overtaking it in 2025.

Since the acquisition, Delivery Hero has extracted roughly US$700 million from Baemin through dividends and share sales. At the same time, Baemin’s domestic market share has come under growing pressure from Coupang Eats, backed by Korea’s dominant ecommerce platform.

As Korea’s ecommerce market saturated – and faced growing pressure from Temu and AliExpress – Coupang doubled down on food delivery at home while also expanding into Taiwan to extract growth.

Relations between Baemin’s local management and the headquarters of Delivery Hero in Germany have reportedly been strained. After the founding team departed, the new leadership showed limited enthusiasm for executing certain HQ-driven initiatives, such as shifting self-delivery merchant fees from subscription models to commission-based pricing.

In 2025, Delivery Hero brought in Austin Kim from Turkey to push through execution in Korea – the same executive who had previously helped Alibaba’s subsidiary Trendyol build local services (Trendyol Go).

An interesting side note: Austin Kim, who grew up in Turkey, happen to share the exact same Korean name “김범석” (Kim Beomseok) as Coupang founder Bom Kim.

Delivery Hero and the Loss of Its Narrative

Across the global food delivery ecosystem, nearly all platforms have endured the same down-cycle over the past few years – but outcomes have diverged sharply.

Uber rebuilt its narrative around cash-flow improvement through synergies across mobility, delivery, and advertising, and its share price recovered first. Meituan remains volatile thanks to the expensive quick commerce war against Alibaba, but the market has not fundamentally questioned its operational capabilities. DoorDash and Grab faced some pressure, yet still command valuation premiums as regional leaders.

Delivery Hero, by contrast, remains stuck in a narrative vacuum: high leverage, limited flexibility, and no clear next-chapter story. The market has responded accordingly through its share price.

The collapse of Delivery Hero’s stock over the past five years has now begun to constrain its strategic options. Baemin has emerged as a potential divestment candidate primarily to lock in liquidity for the debts (mostly convertible bonds) coming due. At current share price levels, both conversion and equity issuance have effectively ceased to be viable options.

Going further, the challenge for Delivery Hero is that, across its global portfolio, only 3 platforms are meaningfully profitable: Baemin in Korea, HungerStation in Saudi Arabia, and Talabat across parts of the Middle East.

In late 2024, Delivery Hero attempted to sell Foodpanda Taiwan to Uber, only for the deal to be blocked by regulators (on Christmas day!). The consideration at the time, including an Uber investment into Delivery Hero, totaled US$1.25 billion – even if that transaction had gone through, it would not have been enough to fulfill its debt obligations.

Meanwhile, HungerStation and Talabat are now facing mounting pressure from Meituan’s Keeta, which has launched across the Gulf countries.

What does this imply?

The divestment of premium assets might be an inevitable outcome of a roll-up platform built through acquisition, now cornered by the end of a cycle.

If the transaction proceeds, it should be seen more as a signal than the end. For Baemin, it could mark a reshuffling of brand destiny. For Delivery Hero, it may represent an implicit acknowledgment that the model of rapid global scale-building through M&A has entered its reckoning.

Over the past decade, global food delivery thrived on capital, consolidation, and scale narratives. In the decade ahead, only 3 things will truly matter: stable cash flow, operational competitiveness, and whether capital markets still believe you can tell the next story.

Baemin retains the first two, while Delivery Hero is paying the price for losing the third.

The final question, then, is who takes Baemin next.

Meituan still has missions at home, with overseas focus centered on the Middle East and Brazil. Grab could expand beyond Southeast Asia – but the price tag of Baemin is almost its entire net cash liquidity. Naver, as a native Korean player, may face fewer regulatory hurdles, though it would still need to articulate a compelling internal rationale.

For Baemin, however, the buyer’s identity may not be the most important question. Whether Meituan, Grab, Uber, or a domestic player, the real dividing line is whether the acquirer has both the capacity and the willingness to turn Baemin from “a mature asset” back into “a brand with a soul.”

That is not a problem financial models can solve. It is a question of organisational design, local autonomy, and long-term patience.