The recent rapid growth of ecommerce in Indonesia has fascinated many. Since we launched Blooming Ecommerce in Indonesia Part 1: Marketplaces, we have received many enquiries, questions and further insights from relevant stakeholders. Thank you!

In Blooming Ecommerce in Indonesia Part 1: Marketplaces, we talked about the rise of key marketplaces, whose collective GMV grew 91% to US$ 40.1 billion in 2020; Shopee has overtaken Tokopedia to become the largest marketplace in Indonesia.

In Part 2.1: Ecosystem – Payment, we discussed the reasons behind marketplaces’ drive to own their own payment, and the current landscape of different payment options including wallets and Buy-Now-Pay-Later (BNPL).

In Part 2.2: Ecosystem – Logistics and Enablers, we explored the growth of logistics across Indonesia, as well as the ecommerce enablers ecosystem. In particular, we shared how the Jakarta Metropolitan area (Jabodetabek) accounts for the destination of 60-70% of ecommerce delivery volume in the country.

Social commerce as a new growth engine?

As the Jabodetabek is becoming saturated, with external customer acquisition becoming expensive, what’s next for players to seek further growth? Would you see a repeat of what happened in China – where a number of social commerce models exploded, with some succeeding and others perishing?

In Momentum Works’ final instalment of Blooming Ecommerce in Indonesia report, we extend on this story, by diving deep into how social commerce comes into play, key models, key players as well as learnings we can draw from international players. We also looked into cross border ecommerce developments in Indonesia.

We will conclude Ecommerce in Indonesia series through an online briefing on Friday Aug 20, where we share more and answer your burning questions about the ecosystem and what’s next for the space.

Few key insights from the report:

1. Social commerce = Social relationship (online / offline) + commerce (literally)

Indonesians are socially active, online and offline, powered by close-knit community ties. For businesses, this provides touch points.

Indonesians are socially active, online and offline, powered by close-knit community ties. For businesses, this provides touch points.

Social commerce taps into just this. Using one person, either through social media content, or their ties with the community, to share about product information.

This allows platforms, both big and small, to extend growth by:

- Making current ecommerce users spend more, by pushing more content on what to buy next

- Reaching out to untapped segments (e.g.: Rural) through agents

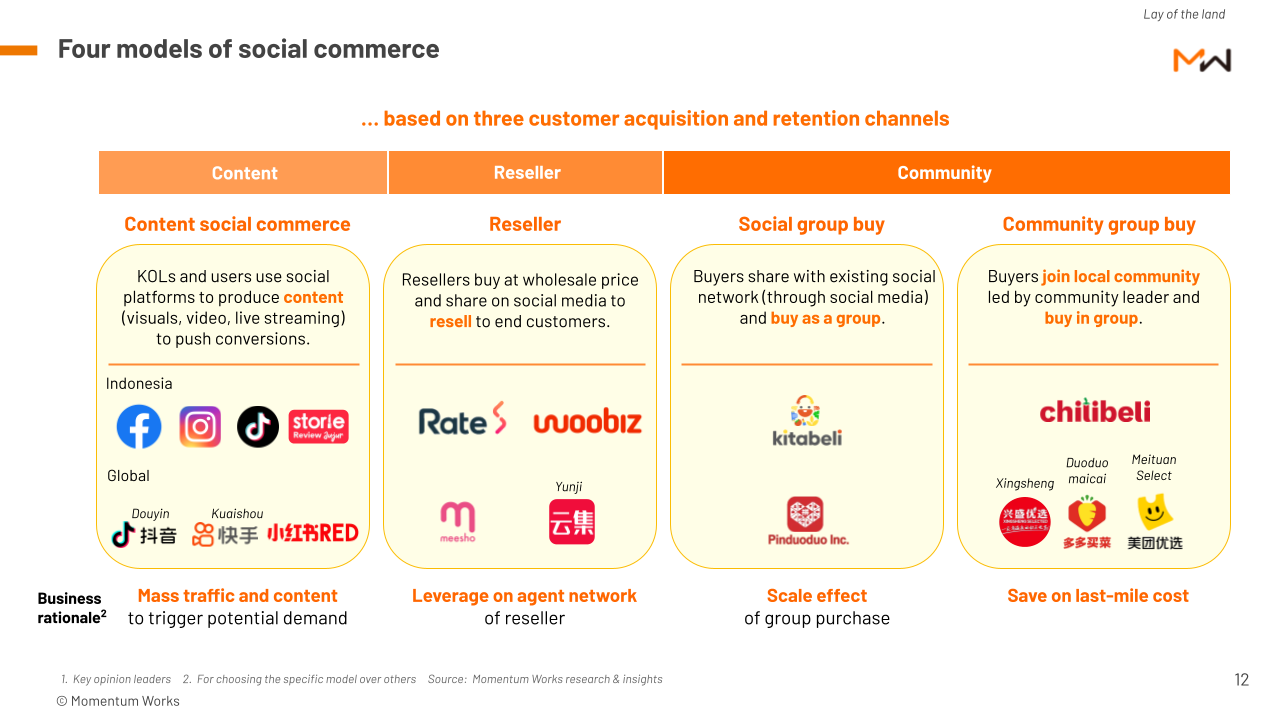

2. Four types of social commerce models:

- Content social commerce: KOL or users produce content (feed, videos, live streaming) on social media to push for potential conversions.

- Reseller: Reseller buys at wholesale price and resell to end customers (earning margin).

- Social group buy: Buyers buy in group (for cheaper price).

- Community group buy: Buyers join and buy together with the neighbourhood group; goods will be delivered to the group leader, who collects orders and will arrange last mile delivery to end customers.

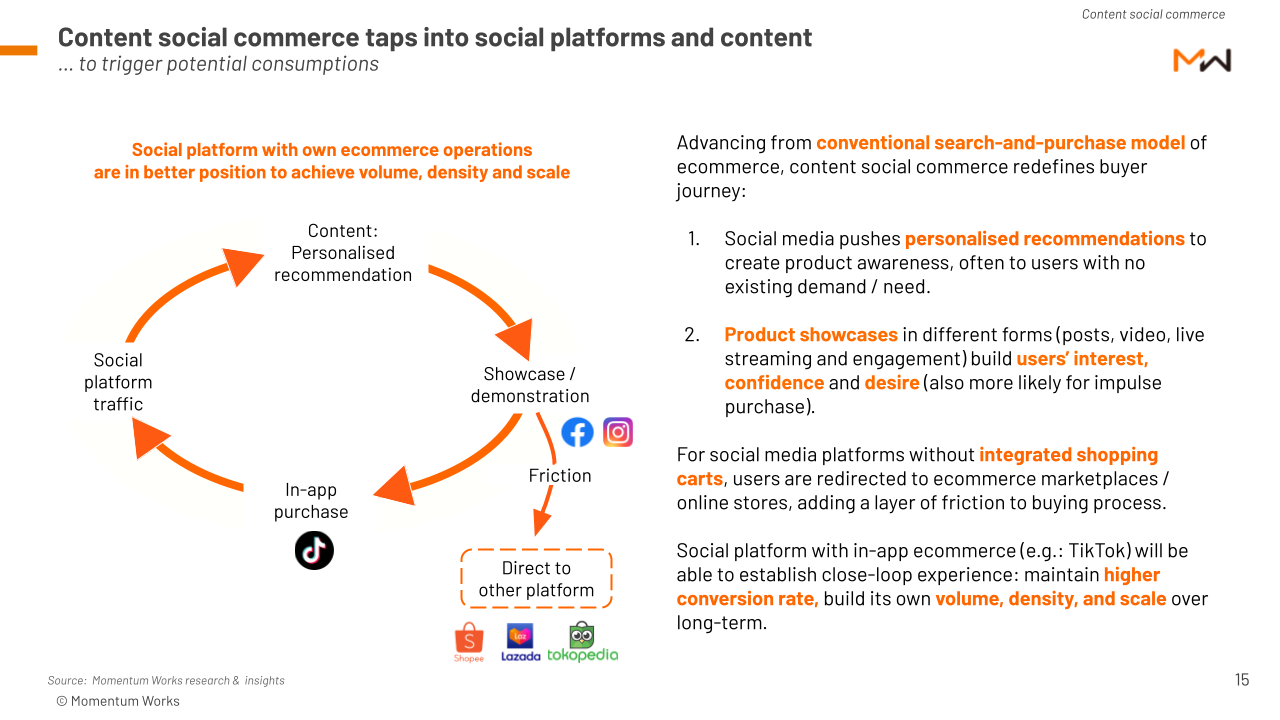

3. Content social commerce: Social platforms have different ecommerce focus (and capabilities)

Facebook and instagram are the largest social platforms in Indonesia, with ~200M and > 100M monthly active users respectively, including bots. However, both mainly act as online catalogues and divert traffic to ecommerce sites / manual fulfilment.

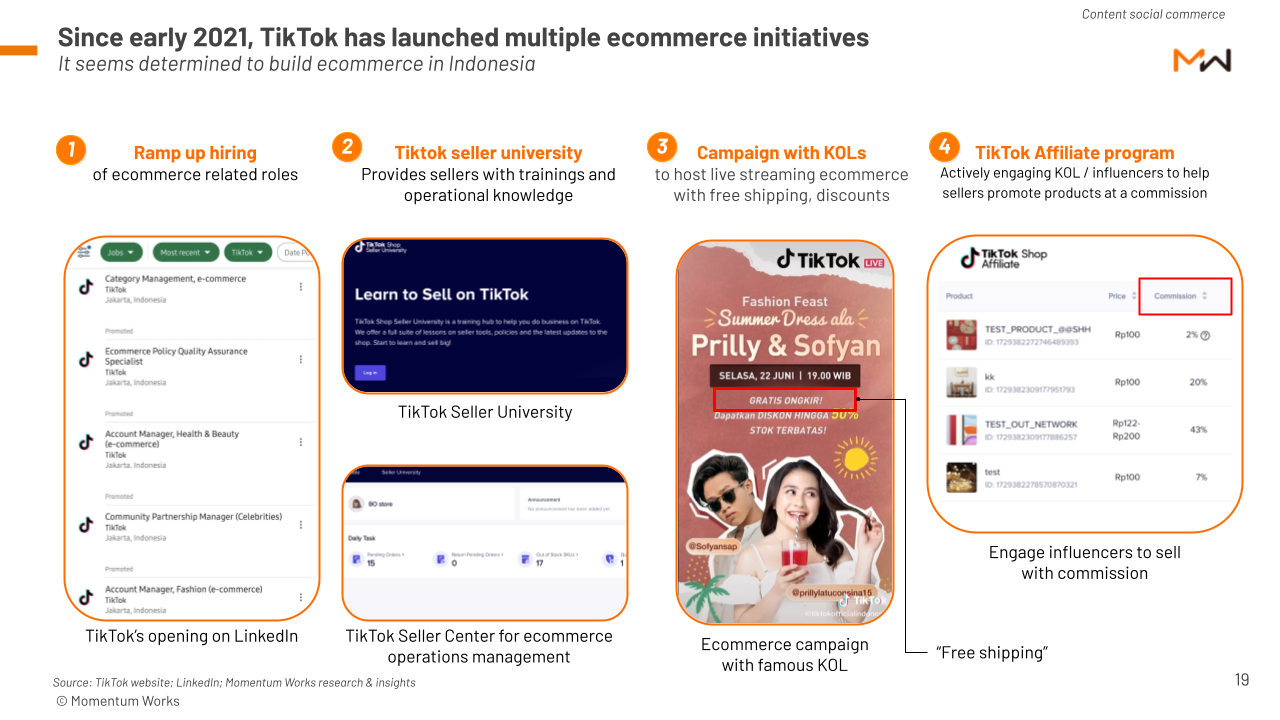

TikTok on the other hand, has been ramping up its ecommerce operations to allow direct checkout within TikTok itself, with payment and fulfilment capabilities.

This, if executed well, will provide higher conversion rate, help TikTok build its own volume, order density and scale over the long-term. It can also completely change the influencer ecosystem and turning marketing costs into commission.

With learnings from China Douyin and its ambition, TikTok can be a serious disruptor in Indonesia. We talked about TikTok’s recent initiatives (and potential challenges) in detail in the report.

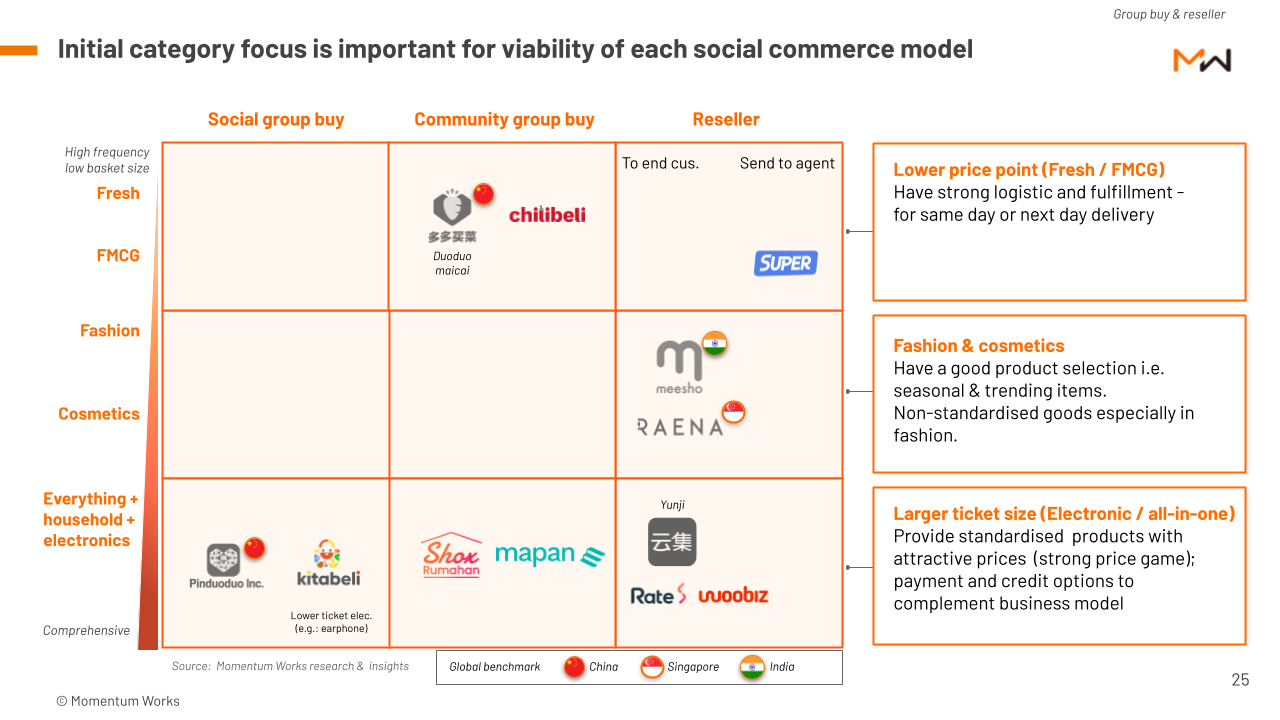

4. Group buy and reseller: Each model has its own sweet spot in terms of categories of products, supply chain and focus demographics

Each product category, from smaller ticket, fast moving products like fresh and FMCG, to fashion / cosmetics, and higher ticket electronic products, have different strategic focus.

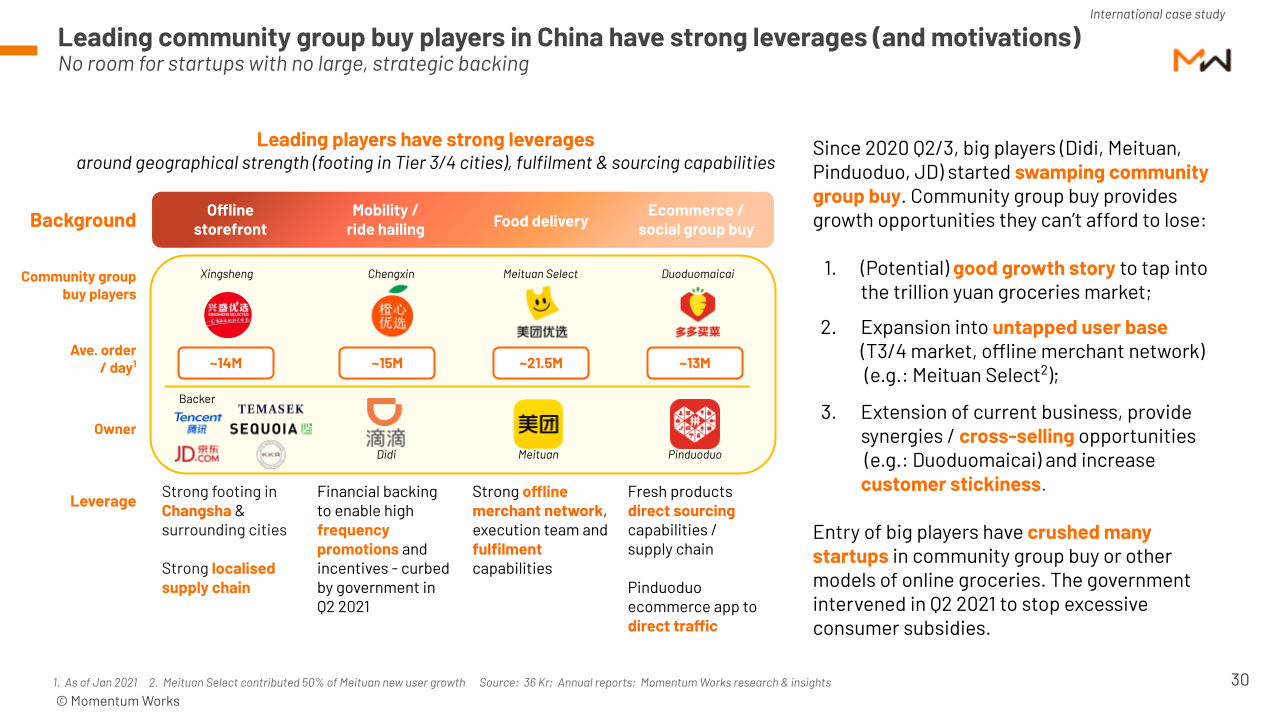

5. Lessons from China: Leading community group buy players have strong leverages

Four players currently leading the race are backed with strong backers and parents. (Didi’s operations might fall apart post the company’s recent challenges with Chinese regulators).

They are also building a strong core: Deep integration with a unique supply chain, their own captive audience, strong fulfillment capabilities, and most importantly, strong team, leadership and execution.

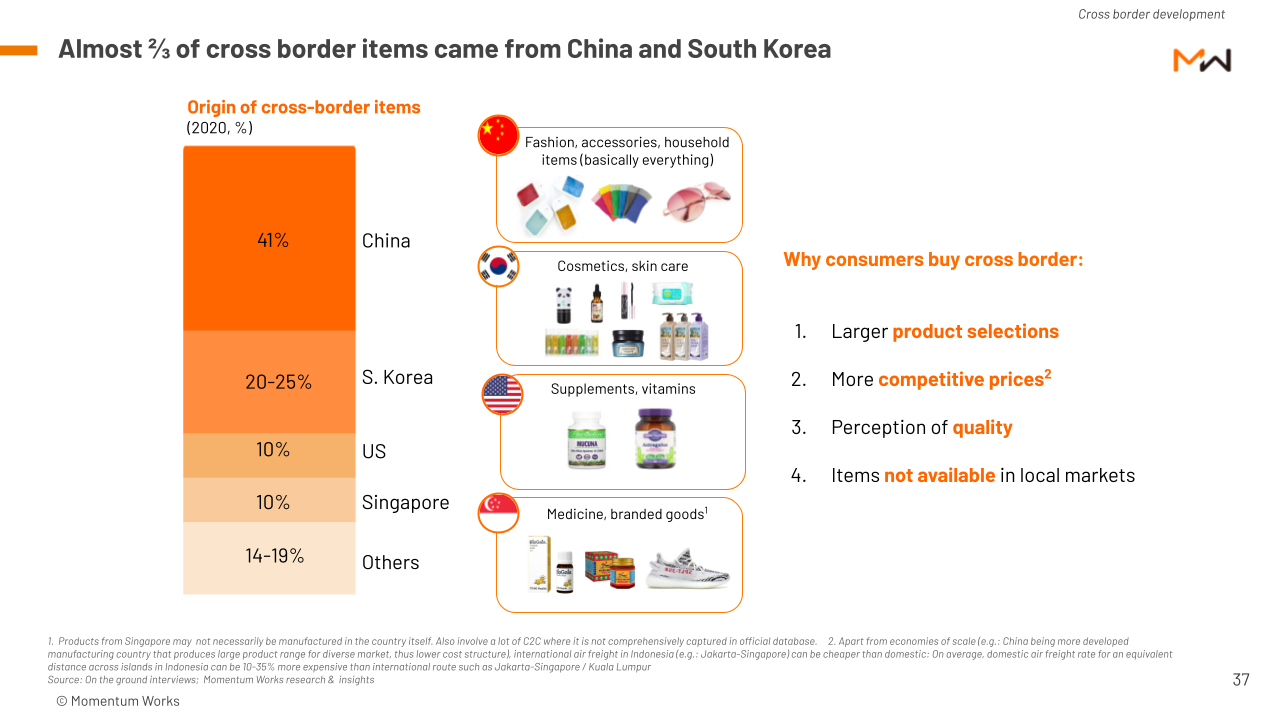

6. Cross border ecommerce in Indonesia exceeded US$ 4.5B in 2020

Cross border ecommerce constituted more than 14% of total ecommerce volume in 2020, or US$ 4.5B. We believe the real number might be much higher, which we will discuss in the report.

Among that, 41% of the goods came from China (where people buy basically everything); followed by South Korea (20-25%).

Access the report

The report is available for industry players, ecosystem stakeholders as well as investors and people who work in the ecommerce industry in general. Check out the report here.

We welcome questions, enquiries and sharings – you can email [email protected].

Also, see you at the briefing!

4.0")