Event banner")

We will be releasing our 3rd annual food delivery platform report in Southeast Asia next week.

We know that 2022 was the year of interest rate hikes. As many offline businesses reopened and investors demanded profitability, the sectors are faced with strong headwinds. Southeast Asia’s food delivery sector grew a modest 5% to reach US$16.3 billion in 2022 after two years of the Covid-driven deliveries boom.

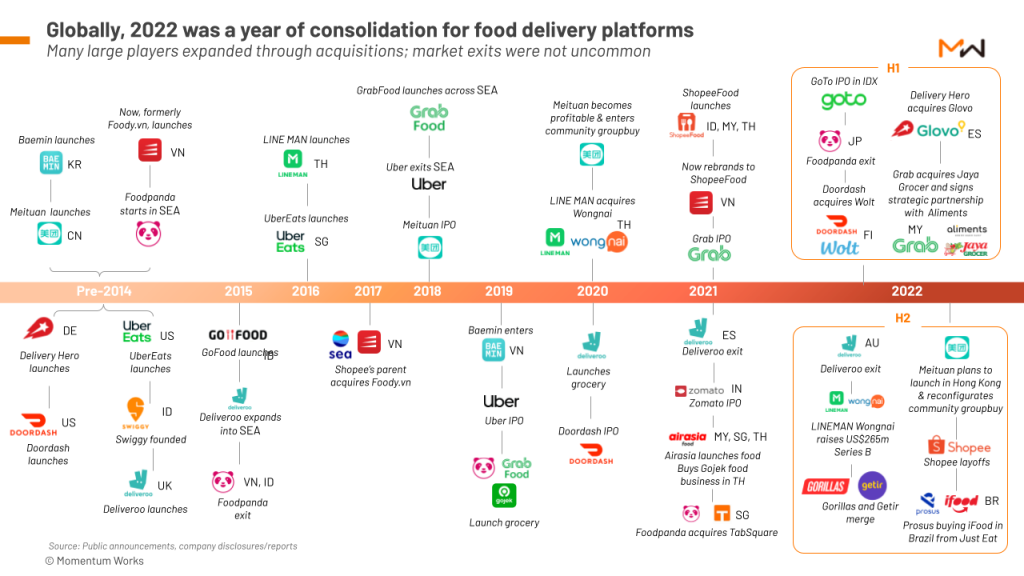

Consolidation for food delivery platforms – many larger players expanded through acquisitions, and market exits were not uncommon.

But what were the underlying trends, competitive dynamics/market share amongst key players, strategies, and of course, prospects of profitability?

We will cover all this in our upcoming briefing at our Food Delivery Platforms in Southeast Asia event on Wednesday 18th Jan, 3-4pm SGT.

Some key insights from the report that we will share:

Market leaders retain positions while larger markets declined

As offline reopens, larger markets find it hard to continue their growth while smaller markets record significant growth – a testament to the consumption power of the smaller countries.

Capturing traffic using online food discovery

Online discovery features, such as reviews and rating systems, have led food delivery platforms to realise their potential in maintaining high in-store traffic to be more relevant in the ecosystem, as dining in resumes.

Exploring revenue expansion options

Many food delivery platforms start to explore further to derive non-commission based revenue to drive growth. Subscription, advertising, financial services, and restaurant solutions are few of the offerings they are testing. One question remains: how far can they go?

Reserve your spot for the “Food Delivery Platforms in Southeast Asia” report briefing, Wednesday 18 January, 3PM – 4PM SGT.

Join us next week as we navigate the evolving sector and be part of the candid discussion with the community!