Last Friday, we hosted an exclusive online briefing on our latest report, Rise of Digital Banks in Indonesia, and had the pleasure of sharing our report findings and insights with an amazing crowd of more than 100 attendees from banks, investment, the tech scene and beyond.

The report, which we published a few weeks ago, has been quite well received. We have received scores of specific enquiries on the report, from investors, traditional banks, tech players as well as a few new digital banks still in stealth mode.

In this briefing, we highlighted the key report findings, compared Indonesia’s rising digital bank industry with those of Brazil and Singapore, and shared our own predictions of what to look next for the industry as well.

We also addressed more than 20 questions raised from the audience, some of which we will share in our next TLD blog post. Here is a recap of some of the key points shared in the briefing part.

Enjoy!

- Digital bank picking up traction in 2020

While the first notable digital bank in Indonesia appeared in 2016, digital banking activities in Indonesia flourished in 2020 with big tech players flowing in (i.e. Jago and SeaBank), driven by Indonesia’s accelerating fintech developments, as well as the continuous regulatory push for consolidation of the banking sector.

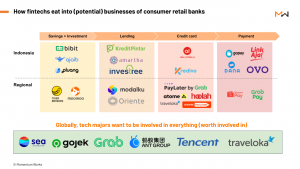

2. Penetration of fintech players in the digital banking realm

A non-exhaustive list we compiled to illustrate how digital banking fits into the entire fintech ecosystem in Indonesia and beyond, and an outlook on existing players that are currently sharing the pie.

Tech majors are aggressive competitors – while we believe they won’t get their hands dirty on every single aspect of the banking business, they certainly are looking at the most profitable ones, and are probably keen to keep those outside the purview of licensed banks they have acquired.

How do traditional banks fend off the competition? Well, the first step is to understand who these competitors are, what their objectives are, what their organisational strengths and weaknesses are, and how they structure their talent base. Only then you know how to respond properly.

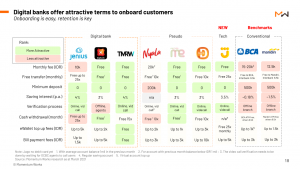

3. Overview on the performance of current players

Digital bank players are now all aggressively onboarding customers through lucrative offers, while some larger conventional banks have joined the race by launching digital only subsidiaries. Consumers, who are mostly urban youth, are shopping around trying every solution. In the long term, customer retention will be the major factor to watch for.

Since our report’s publication in March, Bank Jago has launched a new product – here we have added their offerings to the comparison as well:

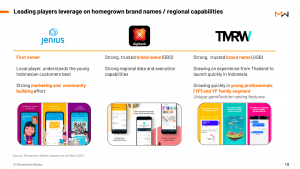

As for user acquisition in 2020, Jenius is still leading, with Digibank and TMRW not far behind. BCA and the tech players might be the largest black horses in 2021:

4. Jenius, Digibank and TMRW – top 3 players in the market

Jenius pioneers in the user base and community rapport, but lags behind on product front and customer service. Digibank and TMRW enjoy more regional banking and talent resources, but questions remain on how to allocate them well and balance out the demand for localisation in Indonesia.

Regardless, the next step for all three will be to balance user growth and consumer expectations, via enhancement on four dimensions – mobile product, price, features and customer service.

Do note that more competitors are on the horizon – they need to work hard to keep the lead they currently have.

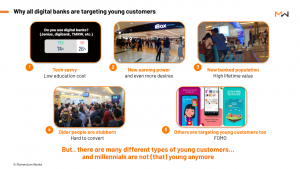

5. Young customers as the key battleground

All leading players are targeting the young segment, we believe these are the key reasons:

However, as mentioned above, young people have not formed loyalty yet – and it will be a tough fight amongst all the leading players to retain more customers for the long term and in a sustainable way.

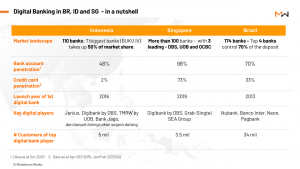

6. Global benchmarks – comparing Indonesia, Singapore and Brazil

In digital banks, we have heard so much about what is happening in the UK, Germany or even Finland. However, we feel that Singapore and Brazil and two very relevant and useful benchmarks for digital bank development in Indonesia.

Singapore is widely considered as a benchmark of what “developed fintech ecosystem will look like” within Southeast Asia, and leading Singapore banks are themselves participants in Indonesia’s booming digital bank sector. At the same time, Brazil is very similar to Indonesia in terms of demographics and level of development:

All three markets have a certain degree of concentration in the banking sector, and embarked on digital bank development at various stages. Brazil is moving faster, offering some valuable lessons/experiences for Indonesia’s digital banking sector.

All three markets have a certain degree of concentration in the banking sector, and embarked on digital bank development at various stages. Brazil is moving faster, offering some valuable lessons/experiences for Indonesia’s digital banking sector.

For example, how Nubank managed to acquire 22 million customers with no marketing spend. They instead invested heavily in tech and customer experience, which is paying off. We have a number of good friends working at various digital banks in Brazil and other Latin American countries – and in future we will organise more sharing with Southeast Asian counterparts.

An interesting fact about regulators is that Brazil’s central bank is in Brasilia, about 1000 kilometres away from Sao Paulo, where most major banks have their headquarters.

Indonesia might see something similar when the capital is eventually moved to Kalimantan from Jakarta.

And as usual, Singapore’s regulatory moves will be watched (and sometimes followed) closely by the region’s other regulators:

7. MW’s predictions looking forward

Some of you might know that we have a pretty good track record in making predictions for Southeast Asia, since December 2017. These are some of the predictions we did over the last few years that are related to fintech development in Indonesia:

Based on the research findings and our real insights from the ground, we think the following might happen in the digital banking sector in Indonesia:

Based on the research findings and our real insights from the ground, we think the following might happen in the digital banking sector in Indonesia:

Final word

We’ve been getting lots of questions and insightful feedback from our audience, both before, during, and after the briefing. Since our time was limited, we weren’t able to get back to everyone and cover every ground in great length (sadly).

However, we’d still like to seize the opportunity and answer your questions as detailed as we could. So stay tuned – we’ll be publishing another article dedicated to the Q&As from this report and briefing – all your questions answered!

In the meantime, feel free to drop us an email anytime at [email protected] should you have any questions about the report, the briefing, the industry in general, or just want to say hi. Would love to hear your thoughts as well!

All the best!!