The author, Fei Ruan (阮飞), Senior Investment Manager of Sinovation Ventures (创新工场), one of the leading early-stage VC firms in China. Ruan is in charge of overseas investments at Sinovation Ventures, with a particular focus on emerging markets.

Last year, because of investment projects as well as personal interest, I made a few trips to India. As my understanding of India deepens, so does my interest. I have been thinking from the angle of an investor: where are the real opportunities in India?

First impression

The first day of my first trip to India, I took a taxi alone to Connaught Place, New Delhi. The area lays in-between New and Old Delhi – to the South is the prosperous New Delhi with its polished government buildings and villas, to the North is the chaos of Old Delhi.

When I was walking through the streets to Red Fort, part of Old Delhi, the visual impact for me is obvious. Un-kept streets, roadside latrines, roaming animals, and the crowd staring at me reminded me that I do not belong.

I bumped into someone who looked East Asian – he greeted me in Korean, I did the same in Chinese, and we shook hands. It felt just that natural.

Impressions aside, when you first set foot into India you would feel the strong diversity and contractions that shape this country. The Indian investors and entrepreneurs I met during these trips shared the sentiment – it is what it is.

All these prompt you to think deeply about this country, and its opportunities.

Not as bad as you thought

India has its potential:

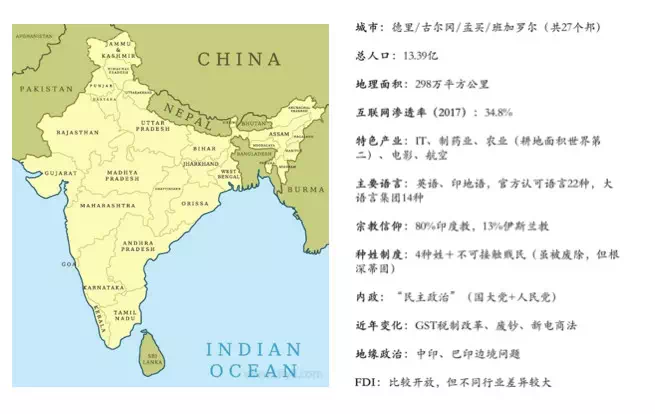

- It boasts the second biggest population (close to 1.4 billion) in the world, the largest number of people who have yet to enjoy the benefits of mobile internet, and the second largest Muslim population in the world.

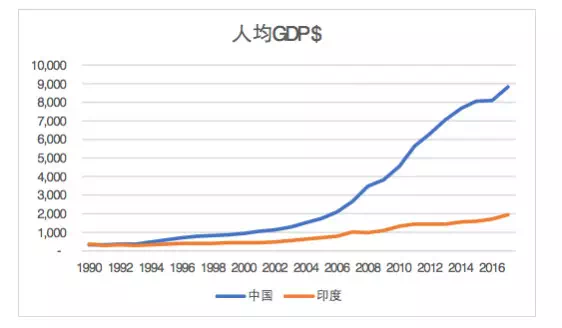

Comparing the journey of India and China over last thirty years, we in China often ignore a fact: since the reform and liberalisation in 1991, India’s GDP per capita has grown from roughly US$300 to more than US$2000 in 2018 – a 7.24% average annual growth rate over 27 years. We can’t ignore that fact, especially when China underwent such transformation as well.

- The reform is still on-going

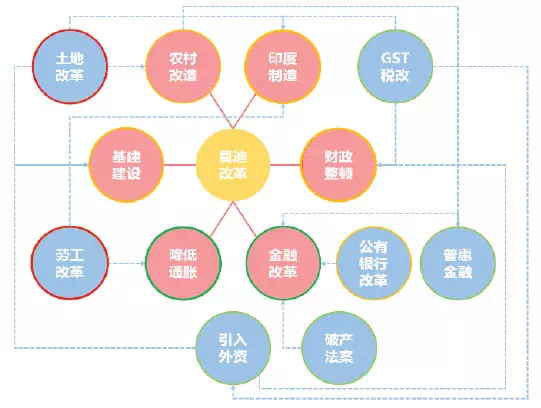

I’ve read voraciously about history and macroeconomics of India. The reform, though sometimes slow and experiencing bumps, has never stopped. Current Prime Minister Narendra Modi has actually done quite a fair bit to further liberalise the economy. Whether he can deliver bolder and more profound reforms if he secures a second term is worth watching.

The image above represents Modi’s ideas for the reform, and many of these my fellow Chinese compatriots will find familiar. We went through these as well.

It is worth mentioning the two famous episodes.

First being de-monetisation, whose proclaimed objective was aimed at the rich and money launderers: that objective has probably failed. However, an important ‘side-effect’ is the shift from the underground shadow banking system to a digital formal financial system. This not only strengthened formal banks’ role in the Indian financial system but also improved credit records of many individual Indians. The long-term effects on the Indian economy are probably very positive.

The second is the GST reform, consolidating the previous myriad of central and local value-added tax schemes into a single Goods and Services Tax. This not only solves the huge bottleneck at state borders for goods flow but also strengthens the Central Government’s control over the whole economy.

Modi has also been promoting the Hindi language, disliked by many native speakers of other languages. However, in China the state-mandated Mandarin across the country with thousands of mutually unintelligible languages – while many public opinion leaders disliked it, the policy indeed was instrumental in creating a single market.

In the long run, all these initiatives are making India more and more like a single, consolidated and large market.

- Good talent base

The elites in India have always put a high emphasis on their offspring’s’ education, just like we Chinese do. In 2015, 5.1% of the population in China (or 70 million people) had bachelor degrees or above – if you sum the number of registered students across Indian tertiary institutions, you will realise the number there could even be higher.

Each year, millions of new graduates join the workforce, many of them with science and technology degrees. This marks India apart from many emerging markets, where top talent goes into business degrees instead.

This is a significant advantage the country will probably enjoy for many years to come.

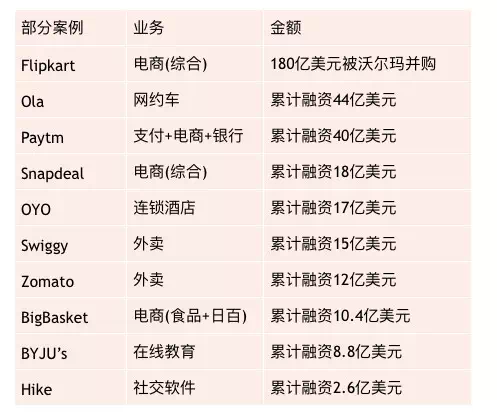

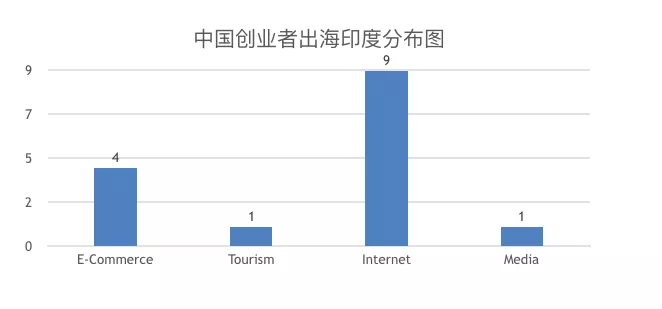

Startups in India

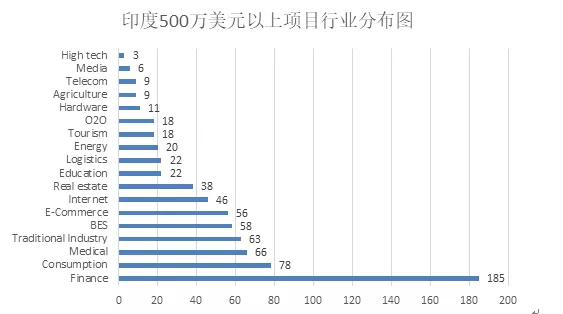

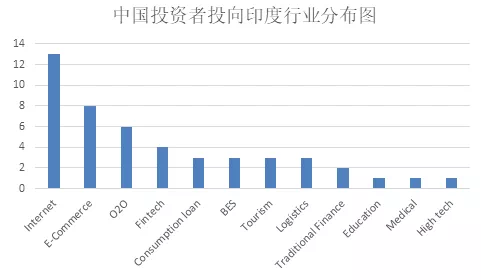

Our team did some research using primarily data from CapitalIQ but also media reports. We collected info about 728 companies which raised more than US$5 million in a single round, including 62 with Chinese founders or investors.

We labelled the companies:

These include a large number of companies in more traditional industries, including finance and manufacturing. Internet companies are mainly concentrated in consumption, e-commerce, education, logistics and O2O. A similar trait compared to China is the dominance of consumer-facing business models.

On the other hand, Chinese founders and investors are mainly interested in traditional internet, e-commerce, O2O and fintech. Among these, industrial capital led by Xiaomi, Tencent, Alibaba and Fosun is the mainstream.

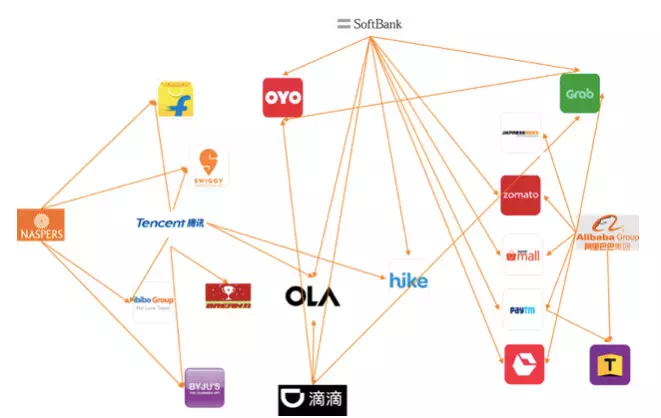

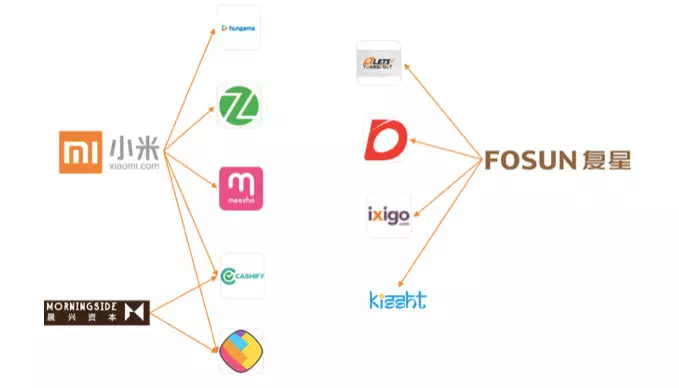

In the two graphs above, we have highlighted some major startups backed by Chinese strategic investors. Through these we have some conclusions:

- Tencent’s strategy is to invest in top companies in the respective sectors. They participate in leading companies in multiple sectors. Alibaba, at the same time, focuses on companies that are close to its core: e-commerce, logistics, payment and food delivery. In addition, Alibaba is trying to build an ecosystem on top of its investment in PayTM;

- Nasper usually goes earlier than Tencent as an investor, while SoftBank is usually later than Alibaba. In some ventures, SoftBank and Tencent made joint investments (such as in the case of Ola);

- Xiaomi has become the top-selling smartphone brand in India. Its investment strategy centres around its advantage in hardware and user base. Shunwei and Morningside, two investors closed allied with Xiaomi, follow its strategy.

- Fosun has a dedicated team for India, with its own methodology. It has made investments in logistics, OTA and finance.

Most of the Chinese entrepreneurs are focused on consumer internet. The common models include light ones such as social, community and utilities which do not require local teams or operations; another model is selling goods from China, leveraging the supply chain advantage China has.

This is similar to what Chinese entrepreneurs have been doing in other major emerging markets.

In summary, we believe:

Positive aspects of India for tech/internet:

- Demographics and increasing internet penetration

- Fast economic growth and increase in consumption power

- Strong base of good engineering talent

- More similarities to China than to the US – easier for Chinese investors to understand Indian ventures

Challenges:

- Big players in most core sectors

- Walmart and Amazon in e-commerce

- In payment, there is PayTM as well as own payment solutions of Flipkart and Amazon

- In O2O, Swiggy and Zomato are fighting a battle similar to the one between Meituan and Ele.me in China

- Ola and Uber form a duo-poly in ride-hailing.

- Strong regulations and protectionism

- Election this year is creating a negative impact on foreign companies;

- In fintech, Chinese regulators often intervene when things turn sour, while Indian regulators jump in much earlier

- The uncertainties around Sino-Indian diplomatic relations.

Where are the investor opportunities

We believe in the following opportunities:

Dividend derived from demographics

The low internet penetration rate (35%) and probably the lowest data package in the world (through Jio) mean that in the next 5-10 years a large population will have the chance to be connected to the internet.

In addition, the already connected users will spend more time on their phones because of fast-improving infrastructure and availability of content.

These factors will give a big opportunity for startups to fill the massively growing screen time. Of course, how they can effectively capture that in the face of bigger competitors remains to be seen.

On the other hand, because of the huge wealth gap in the society, the masses will take a while to be consumers especially paying consumers. So when we analyse the potential of the internet population, we should put the timeline to be at least 10 years.

For more current business models, we should not treat the market size as the population of India, probably half of that or even less.

Opportunities coming from the urban-rural structure of the society

- Platforms for multilingual and multicultural nature of the country: statistics say that there are 180 million English speakers, 200+ million Facebook users and about 270 million Whatsapp users.

Currently, major internet products mainly use Facebook and Google to reach out to their customers. However, these two have limited reach to the rural and small-town masses, many of whom have yet to be exposed to the depth and width of product offerings their city counterparts are.

Sharechat is an example of outreach to that demographics and we see more opportunities in reaching out to this population.

- Products: With GDP per capita of 2000 USD, India is in need of a massive amount of consumer goods. Things like air conditioners, washing machines, fridges and air purifiers etc. will see a surge in China, just like it did in China many years ago, when the GDP per capita was at similar levels.

There are two opportunities here: first is the upgrade for urban elites from basic brands to premium brands, second is good quality products with basic brands penetrating to other classes of the society.

Opportunities derived from improving infrastructure: for example, parcel delivery logistics depend on the development of roads and e-commerce, while property platforms depend on the number of urban dwellers living in residential blocks.

Copy China to India: finding areas in China where you have successful and leading players, which are yet to be developed in India. Of course, this is not pure copy, inspiration and adaptation probably is a better approach.

Will India be the next China?

While in many ways India’s startup ecosystem resembles that of China, the macro environment is very different.

Every time I was in India, local entrepreneurs will tell me where India is compared to China (the most common phrase heard is “India is like China 10 years ago”). I understand where they are coming from – this makes it easier for Chinese investors to understand and appreciate the realities in India. Many even say “My product is India’s version of China’s XXX”.

Rightly so. Both being developing countries with a large population, India and China bear a lot of similarities as far as the internet is concerned. Many leading Indian startups are indeed adapting Chinese models.

One example is the growth story of PayTM:

- January 2014, PayTM launched its wallet app. At that time, about half of the Indian population did not have bank accounts, while the credit card penetration was lower than 5%. More than 90% of the population pay their daily expenses in cash – a fertile but tough environment for PayTM to crack in;

- In 2015, Alibaba and Ant Financial invested 815 million USD into PayTM;

- In October 2015, PayTM launched its QR pay, and started fostering adoption at small merchants and customers;

- November 2016 – demonetisation happened. In a society where POS and credit card penetration was low, cashless societies equal mobile phone payment. Some data suggest that within one month, active users of PayTM grew from 10 million to 160 million;

- April 2017 – PayTM user base surpassed that of PayPal and reached 220 million, with more than 3 million transactions every day. That makes it the third largest digital wallet in the world;

- June 2018, monthly transactions hit 4 billion USD, with 1.3 billion transactions.

It seems PayTM is now the leading player in the payment war in India. However, compared to Alipay, which grew out of the already big and successful Alibaba ecosystem, payTM grew its use through offline use cases and without e-commerce payment as strong support. Neither Amazon nor Flipkart support PayTM.

So to make its strategic position stronger, PayTM built PayTM mall. At the same time, it acquired a lot of companies in the payment ecosystem to try to build its own sphere.

We believe that as long as the overall direction of reform and liberalisation continues, India will remain attractive to good startups and international capital. On the other hand, we have to realise that China’s path is unique and almost impossible to replicate.

So for Chinese investors, we need to have more patience in India.

In China, when the market takes off, as long as the VCs bet on the macro right, they make money. In India, you need to be much more careful and selective to get good returns.

As an experienced investor, I believe that opportunities come amid major changes. That is why I find emerging markets, in particular, India, very charming.

For those who do not know us, Sinnovation Ventures is a 10-year-old VC fund and we are now paying a lot of attention to good startups in emerging markets.

You are welcome to contact us 😉