Most of us can agree that the tech scene is more developed in China than in Southeast Asia. Any startup that appeared in Southeast Asia would already have had its doppelganger in China. Think Shopee and Taobao; Flash Express and SF Express; Grab and Didi.

Yet, as you scour through Southeast Asia’s biggest startups, you will soon find a surprising omission from this list. Shopback. Its status as one of Southeast Asia’s aspiring unicorns reflects the investors’ trust in its business model, so why doesn’t it have an equally well-known counterpart in China?

How does Shopback work?

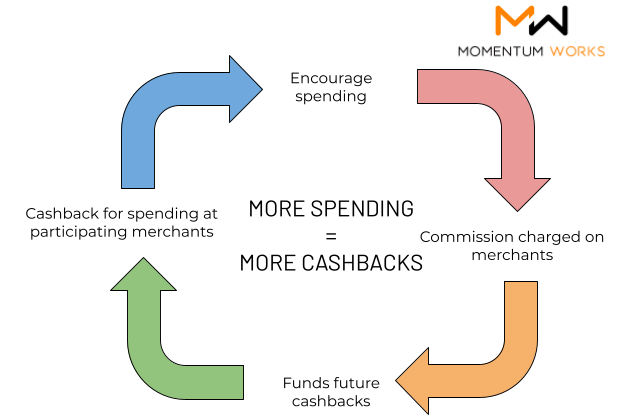

Shopback’s main purpose is to connect brands to users. Different sellers feature different promotions for different products on different platforms– most buyers would find this sheer overload in choices outright overwhelming. Shopback creates a more user-friendly search process by consolidating these brands under a centralized platform. Ergo, an ecommerce aggregator.

To attract users to its platform, Shopback mainly relies on a cashback rewards system. Users enjoy discounted prices since they receive a small percentage of their original spending when they buy from Shopback-listed merchants.

With every purchase that its users make on its site, Shopback charges a commission to the associated merchant (which is funnelled back towards its pool of cashback). Essentially, Shopback is levying a fee for their customer acquisition.

What are the prerequisites of Shopback?

For users, an aggregator only adds value if the current search process is too complex, with too many options for the buyer to compare. In other words, Shopback can only exist in a fragmented market, where merchants are selling on multiple platforms. That’s exactly what’s happening in Southeast Asia– sellers not only list their products on Shopee but also Lazada, Qoobuy … Not one site rules them all.

On the other side of the equation are sellers that are only concerned about one thing, cost. And that concern applies to customer acquisition as well. In other words, as long as Shopback’s commission remains lower than the CAC from other channels (Facebook marketing, Google ads), sellers will continue to find Shopback attractive.

Does the Chinese market fulfil such requirements?

Unlike the different battlegrounds in Southeast Asia, where several big players vie for supremacy, the Chinese ecommerce market remains long overshadowed by Taobao’s presence. Though a few saplings (Pinduoduo, Xiaohongshu) are jostling for growth beneath its shade, Taobao continues to hoard most of the demand, with the latest estimates of its market share hovering around 50%.

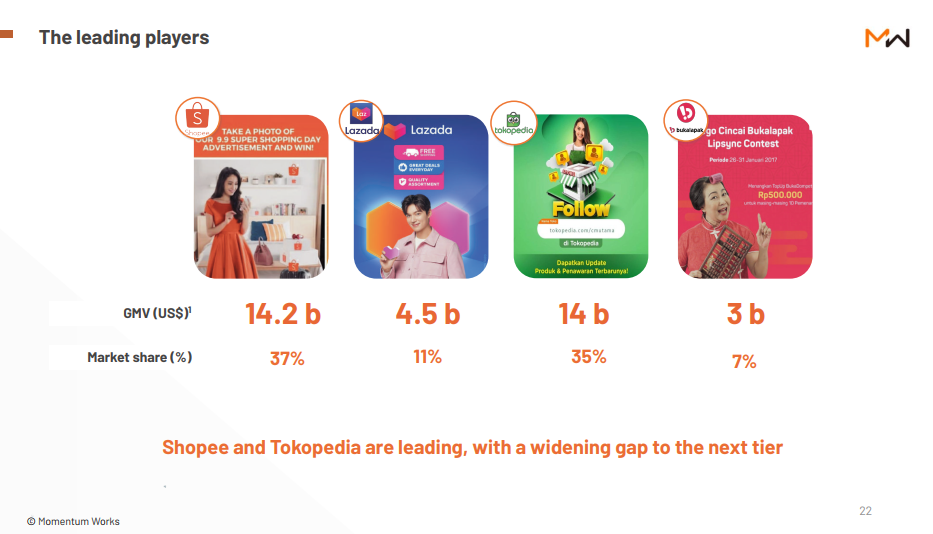

In contrast, Shopee, the leading player in Indonesia’s market, only holds 37% of its ecommerce pie:

To put it in another way, most roads in China lead to Tmall, which makes the buyers’ search path much more straightforward– but aggregators much less useful.

In a consolidated (and intensely competitive) market like China’s, entrants will also have to deal with high customer acquisition costs. It’s classic economics– when the bigger merchants monopolize traffic, other players will have to spend more to redirect traffic away from them. For a cashback platform, it means more lucrative rewards and higher customer acquisition costs.

Facing such rising costs, ecommerce aggregators could choose two possible paths, neither of which are desirable. Increase the amount of commission that they charge merchants– and risk losing them– or absorb this growing expenditure.

Yet, even if these businesses do possess such a war chest, they will face intense scrutiny due to their shrinking– and often, negative– profit margins (basically Pinduoduo). After all, no investor wants their company to end up like Jianpu Technology:

Right model, wrong place?

The math behind Shopback adds up; the company’s continued expansion into newer APAC markets bears proof of it. As such, the absence of a Shopback-like ecommerce aggregator in China points to the unfavourable environment, rather than the infeasibility of the business model.

For the investors that are putting Shopback under the microscope, the bigger question that they should be asking is whether the ecommerce market in Southeast Asia will end up like China’s. While there are similarities in buyers’ and sellers’ behaviour between China and Southeast Asia, the latter is still a motley of countries with different languages and customs.

If this market does remain fragmented, there is likely to be pockets of traffic for Shopback to grow. If it does, however, consolidate, Shopback will have to keep evolving its business model– just as it has done with initiatives such as Shopback GO and Shopee Affiliate Marketing Solutions (AMS).

Q4 2025 earnings call transcript")