")

This article is contributed by a Singapore-based investor who has previously lived in Europe, with slight editing from TLD. The author prefers to remain anonymous.

Mobility-as-a-Service, or MaaS, is a cool concept that is often touted as the solution to the traffic problems in urban areas.

Over the last couple of years, a number of (mainly European) companies have come to Southeast Asia in an attempt to expand their business. Some companies in Asia have jumped onto the bandwagon.

The rationale seems obvious too – the region is fast growing, and the major capital cities are facing severe loss of productivity due to the traffic. The only exception, Singapore, spent a lot of effort to make sure the city is smooth, from Electronic Road Pricing (ERP) to Zero Car Growth policy.

However, MaaS DOES NOT work in Asia, at least for the coming decade or two.

The MaaS Holy Grail

Wikipedia gives a pretty good definition of MaaS:

“… a shift away from personally-owned modes of transportation and towards mobility provided as a service. This is enabled by combining transportation services from public and private transportation providers through a unified gateway that creates and manages the trip, which users can pay for with a single account. Users can pay per trip or a monthly fee for a limited distance. The key concept behind MaaS is to offer travelers mobility solutions based on their travel needs.”

The concept first came about seriously in Scandinavia. To date, the main players are UBiGo of Sweden and Whim of Finland.

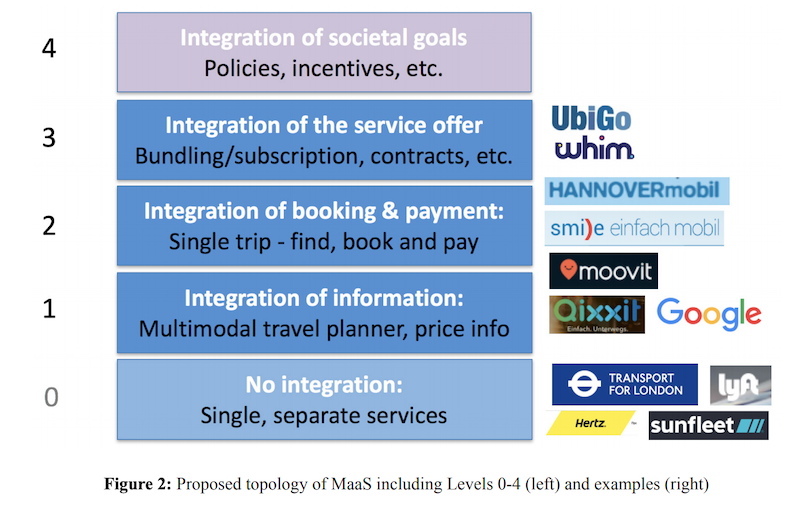

The scholarly research about MaaS is largely European-based too, with the four integration stages in a Swedish paper often cited by MaaS proponents across the world:

And obviously, stage 4 is the ultimate goal, which no one has attained yet. UbiGo and Whim are at second level, with subscription service bundling multiple modes of transportation.

Key assumptions

From an investment point of view, MaaS is attractive as well. Assuming a city of 5 million, where half of the population spends $40 per month on commute – that’s an annual market of $2.4 billion. If you assume a take rate of 5%, that means revenue of $120 million.

And that’s just for a medium-sized city. There are many cities of that size or beyond in Asia.

However, there are a few key assumptions:

- There are multiple modes of transportation, from trains, buses to shared bicycles and shared cars;

- The public transportation needs to be good enough to be the backbone of such a network;

- Payment, data and technological infrastructure is good enough to allow such integration to happen;

- In addition, a whole settlement network needs to be negotiated and implemented if you allow people to customise their packages;

- There is incentive from different parties, including the policy makers, transport mode owners, and commuters to adopt.

Why it DOES NOT work in Southeast Asia

The first three will basically rule out most of the emerging markets. And you can reasonably expect that the relevant public infrastructure will take at least a decade or two to take shape.

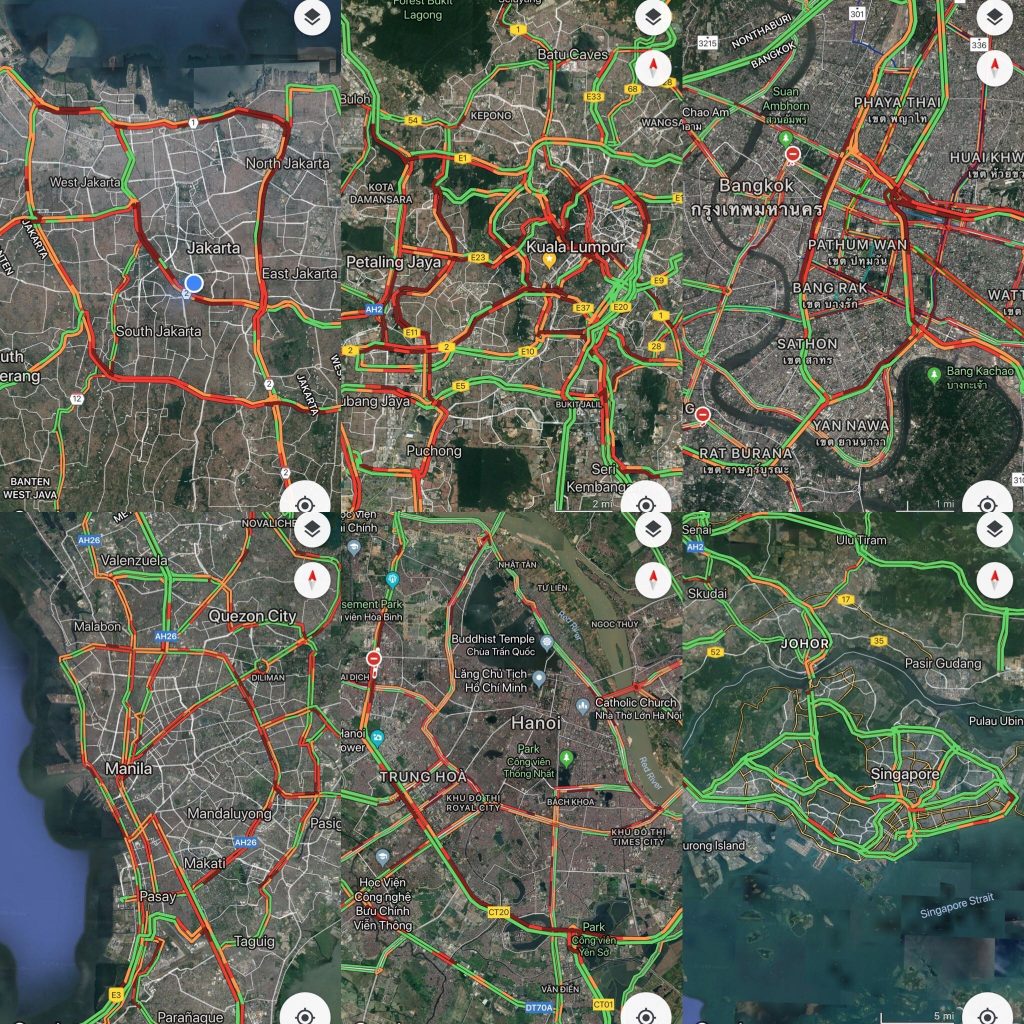

In the meantime, in places like Jakarta, Bangkok and Ho Chi Minh City, the wide availability of motorbikes form one of the most important transportation nodes.

Companies like Grab, which provide on demand booking of transport, makes much more sense than a complex integration from a third party that has little value to consumers who use no more than two modes of transport.

Even in the much more advanced market of Singapore, the modes of transport people usually take would not be more than three, making any MaaS service largely redundant unless the subscription would lead to a good discount.

But why would the authorities and operators give a good discount, since car ownership is low anyway?

The only value of offering such a service, in our opinion, is to obtain transaction data (you need payment integrated to be able to do so), which in turn allows the service provider to offer advertising, lead generation and even financial services.

In that regard, Grab is already doing a pretty good job, leaving little room for a third party, unless backed by the transport operators, and with the public transport integrated. Even that, the company needs a lot of work to realise the perceived benefits.

Not easy in Europe, as well

Even in Europe, MaaS is not smooth sailing.

While there is a strong incentive to reduce urban congestion and be environmentally friendly, it is not easy for the politicians to rally behind the cause beyond giving lip service.

First, that involves planning, negotiations, public communications, pilot etc. That easily takes years (beyond the election cycles) – and why would you do that if there are other ways (like making more shared bikes available) that can win you votes as well?

And, if your public transport is subsidised, would you allow the MaaS players to resell the tickets at a profit?

Therefore, it takes years of lobbying and hard work to make it work. I would not see any reason why non-strategic investors will have that patience.

If the numbers I heard are correct, neither UbiGo nor Whim has profitability in sight yet.

The likes of Grab are already far ahead in that regard.