This article is written by Visa Kannan, a partner at Saison Capital, and originally posted here. Republished on TheLowDown with the author’s permission.

Like everyone else this past week, I read the OYO DRHP (draft red herring prospectus) and I wanted to highlight 3 data points and claims that I thought were interesting – not necessarily only to call out the red flags, but just things that made me think:

1. OYO’s real job-to-be-done

The filing in one place reads: “Many of the key cities…recorded more than 40% of demand from same-city Customers”

If you think of the “job” OYO had intended to do from a customer point of view it was to bring standardization to hotels. Having the OYO stamp meant a customer travelling anywhere knew what they were getting – basic facilities, a clean room and safety. The same-city data point makes one wonder if the real job to be done here is actually one of providing privacy from crowded homes in congested cities – a private escape, at a reasonable price.

What is strange though is that the 40% number has been fairly consistent across both pre-covid and covid years. My hunch was that in a covid year this use-case (especially with kids at home from school and homes noisier than ever) would have been the primary one that OYO served. Shouldn’t a greater portion of revenue have come from this segment in a pandemic year?

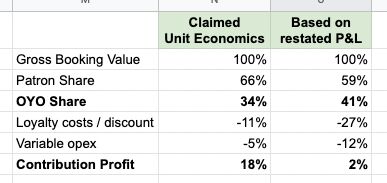

2. Unit Economics – more illustrative than real?

The filing spells out the unit economics of the business for the 2021 fiscal year on page 236 and on the face of it looks quite attractive with a contribution margin of ~18% and the claim that “investments, capital expenditure and expenses relating to the operation of such storefronts borne solely by our Patrons.”

I tried to fit the actual P&L numbers into the illustration and the unit economics don’t actually look as good (see the table in the image). 2 things stood out – the discounts, incentives, refunds portion is underestimated quite heavily and the “transformation expenditure” is missed out, in its entirety. Elsewhere in the DRHP, OYO clearly calls out that they very much bear the cost of transforming properties.

Restated, the economics of the core hotels business of OYO is likely ~2%. It’s hard enough to make any business work with such wafer-thin margins let alone a business like OYO, which has massive overheads.

3. The only top-line item that grew y/y – commissions

The OYO financial statements leave very little room for hope – a hotel business, trying to IPO in the middle of a pandemic – revenues are down 70% y/y, cost structure remains largely the same.

Curiously though, there’s a revenue item that did grow 10% y/y – commissions from bookings of vacation homes and listings. This constitutes 20% of OYO’s top-line and is a relatively new business for OYO – having started only in 2019-20 with the acquisition of a vacation homes business in Europe.

Numbers suggest that this is a market worth doubling down on – OYO includes Europe as part of its “Core Growth Markets” and it will be interesting to see how this business unit fares in the future.