")

This article is contributed by a friend of Momentum Works who is a veteran of the payment industry in Singapore. It was originally written in Chinese and published on Momentum Works’s WeChat platform. The author wishes to remain anonymous – any feedback or suggestions can be channeled through [email protected]

Southeast Asia has become a focus area for all parties in the digital payment industry, and the most fierce competition in the entire payment industry is the various payment methods for consumers’ daily transactions.

The market is quite fragmented, with competition and collaboration amongst e-wallet-based mobile payment operators, acquirers, and traditional card-based issuers, as well as settlement networks.

Let’s analyze Singapore’s payment landscape as an example, and discuss the potential future direction of the industry.

1. Fragmentation and Integration of Traditional Bank Card Payment System

Traditional bank card payment systems have been established and developed earlier in the Southeast Asian market. Most markets have relatively complete payment infrastructure, such as NETS (Singapore), ITMX / TPN (Thailand), and Paynet (Malaysia). The local debit card settlement networks and the international card networks compete and complement each other. The difference in each market is mainly the penetration rates of various payment products.

Taking Singapore as an example, the local debit card settlement organization NETS was established as early as 1985, thus starting the popularization of electronic payments based on debit cards issued by local banks. After many years of hard work, Singapore now has 6 banks issuing debit card products with NETS payment functions. There are more than 120,000 merchants accepting NETS payment across the island, which basically cover all aspects of daily life.

At the same time, all six international card organizations (Visa, MasterCard, Amex, UnionPay, Diners Club/Discovery, and JCB) have established operations in Singapore. Debit and credit card products issued by local banks also generally support both the international card networks as well as NETS.

At present, nearly 30 million such bank cards have been issued in Singapore. The acceptance network for such bank card products is quite complete, and most merchants accept both NETS and mainstream international card networks as payment methods. Consumers can also choose to pay through the NETS channel or the international card network channel according to their consumption habits and preferences.

The payment system based on traditional bank cards mentioned above has actually undergone a process :rapid development → fragmentation → integration.

Take Singapore as an example. The Monetary Authority of Singapore (MAS) has promoted the unified terminal (UPOS) since 2018, which has greatly optimized the multi-terminal situation on the merchant side and simplified the difficulty that cashiers have to endure with identification of different payment tools.

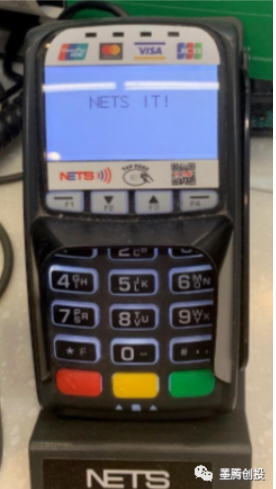

The picture below is one of the mainstream UPOS terminals of NETS, which accepts NETS, Visa, MasterCard, UnionPay and JCB at the same time. Merchants only need to select NETS or credit card at the terminal or cash register to directly process different payments. According to NETS official website data, 54,000 unified terminals have been deployed. Through this round of integration and optimization, the Singapore market has resolved many technical and operational challenges to a certain extent, driven by regulators.

Although starting from the regulatory requirements and the needs brought about by the development of the market itself, merchants continue to integrate and optimize traditional bank card acceptance, but the rapid development of e-wallet-based mobile payment has brought a new round of fragmentation process that takes QR code payment as the core。

The following picture shows a merchant in Singapore showing the various payment tools it accepts:

2. Mobile payment inevitably accelerates fragmentation

e-wallets have gradually emerged in Singapore since 2016. For example, based on the analysis of Payment Services Operators, Standards and Acceptance Networks, at present, mobile payment methods based on e-wallet are mainly divided into the following three categories:

One is electronic wallet payment based on traditional bank cards or accounts, such as PayLah! launched by DBS, Pay Anyone from OCBC, Mighty from UOB, and Unionpay from China UnionPay. Acceptance networks are generally based on unified standards and open-loop acceptance networks. For example, PayLah! uses NETS and PayNow standard QR codes, and UnionPay uses its own standard QR codes and acceptance networks.

The second is a wide range of e-wallets based on prepaid accounts, such as Dash launched by Singapore Telecom, Shopeepay from Sea Group, and so on. The acquiring side generally independently expands the acceptance network based on its own standards. Alipay and WeChat Pay should also be included in this category, but in China, it also supports binding bank cards and paying through Alipay and WeChat own specifications and acceptance networks, which have some of the characteristics of the first and third types.

The third is to realize electronic wallet payment by binding traditional bank cards, such as FavePay under the lifestyle platform Fave, which was recently acquired by Indian POS company Pine Labs. Generally, the acceptance end will also independently expand the acceptance networks based on its own standards.

It can be seen that, in addition to the traditional international card networks still striving to adhere to their own global unified standards after entering the QR code payment field, other types of wallet payment tools use their own set of payment standards and build their own acceptance networks. The fragmentation of the mobile payment market has inevitably occurred.

On the other hand, “inadvertent” competition among different local settlement networks in various markets has also exacerbated the degree of fragmentation. For example, although Singapore NETS and PayNow are both operated by the NETS Group, due to factors such as different business origins and different banks involved, NETS QR and PayNow QR are actually in a state of competition, and how to integrate them in the future is worthy of attention.

Regulatory agencies in the region have gradually become aware of this problem. Markets such as Singapore, Thailand, Malaysia, and Indonesia have seen a certain degree of integration initiated by regulatory agencies and all parties in the industry on the acceptance side. For example, the unified QR code standard SGQR (the following figure shows the various payment tools supported by SGQR in the early stage of implementation) jointly initiated and implemented by MAS and IDA (the Infocomm Development Authority of Singapore, which has merged into a new agency called IMDA).

However, SGQR pays more attention to the integration of front-end QR codes and only implements them in the field of static codes. There are still no small challenges in the integration of back-end operations and settlement. On the other hand, payment aggregators are also gradually expanding. For example, PayLah! recently reached a cooperation agreement with FavePay. PayLah! can scan FavePay’s QR code for payment, and aggregate payment service providers represented by FomoPay and LiquidPay provide better acceptance. Terminal exposure and back-end clearing services.

The picture below shows the exposure of the XNAP QR code acceptance network promoted by LiquidPay on the merchant side):

3. Challenges are coming

- It is difficult for merchants to support multiple payment tools at the same time

All parties in the e-wallet-based mobile payment industry, whether they are traditional players or upstarts in the Internet industry who have recently entered the payment field, are currently investing a lot of resources in the construction of the acceptance area. These include the acquisition of merchants and the subsidies on the MDR. Offline F&B and retail merchants in Singapore are overwhelmed by the promotion of various wallets and mobile payments. Merchants also face challenges in the management of different payment tools, and it is difficult to require merchants or cashiers to be familiar with each payment tool.

- Low usage

In fact, the development and stability of the acceptance network of any payment tool will always be inseparable from the support of its issuing end, that is, the user end. Aquiriers spent a lot of money to acquire the merchants. If they can’t get enough usage, most of the merchants will eventually choose to leave. High-quality merchants or high-quality usage scenarios cannot be acquired just by spending money, but need enough usage to convince them. If you consider the natural change of retail merchants in the market, the continuous investment in acquiring merchants again and again is obviously unsustainable.

- Source of funds

E-wallets based on prepaid accounts also need to solve the challenge of the source of funds. Even PayLah!, which is widely recognized by the market, faces similar problems. The electronic wallet payment realized by binding traditional bank cards does not have the challenge of the source of funds but often faces high costs to sustain.

- Lack of potential for cross-border payment expansion

At present, most e-wallets have invested a large number of resources in merchant acquisition. However, they can only solve the need for local payment. Cross-border payment, an important use case, still needs good solutions.

4. The future of integration

In the long run, what form the (currently) fragmented payment scenario will achieve integration is a question worth discussing. Below we also propose the future trends of the three payment scenarios.

- The acceptance network moves towards integration

One possible scenario is the further development of payment aggregators. But for that to happen, the market needs to balance the role of payment tools and payment aggregators.

Another scenario may be more likely to occur, where larger merchants only choose payment tools with market scale. Smaller-scale payment tools that lack sufficient high-quality merchants and use cases will be “forced” to integrate with other payment tools or industry partners.

- Focus on the user

Based on a certain scale of the acceptance network, e-wallet-based mobile payment players may want to focus more on the user side. A major international bank once used the “3+3” strategy to increase its market share in both issuance and acquiring businesses.

The strategy is actually to invest a lot of resources in the card issuance business in the first three years of business expansion. Starting from the third year, more resources will be focused on acquiring business and merchant card marketing to obtain a large number of merchants. The merchant acquisition network will also give further impetus to the issuance side, and the cost of the acquiring business can also be reduced due to the support of the continuous growth of the card issuance business.

Still taking the Singapore market as an example, the current mainstream wallets basically have a strong original use case and a group of loyal, stable and frequent users in this use case. Examples are ShopeePay in online shopping, and Dash in cross-border remittance. When expanding from basic use cases to a wider range, the most important and most challenging thing is to convince users why you should use your payment tool in other use cases.

The broadening of acceptance coverage is only one aspect of persuading users. After achieving a certain size of acceptance network, it may be possible to consider investing resources more focused on motivating users, because the starting point for merchants to accept multiple payment tools is often to facilitate consumers and drive more sales. Well, then bringing consumers to merchants actually means far more than simply reducing MDR or giving merchants more rewards.

The best reference case is the payment products which focus on bringing merchants more customers. A large number of users, in turn, can encourage other merchants to join the network, and keep existing merchants onboard.

- Improving convenience is the key

Convenience ranks at the top of factors considered by users in choosing payment tools in various market research. It is even higher than the rewards. Therefore, it is another important dimension to gain more users and usage. A wide acceptance network is one of the necessary conditions to reflect the convenience of payment tools. Another convenience factor comes from the source of funds – PayLah! allows direct debit because it is owned by a bank. On the other hand, Dash provides novel auto-top-up services that are suitable for its suite of product features.

Of course, the current e-wallet-based mobile payment market is still in a period of rapid change. But major trends should be clearly visible.

The same methodology can also be applied to other countries in Southeast Asia, although their respective patterns and development paths may not necessarily be the same.

Entrepreneurs may have to think harder about their strategic position in order to prepare for the next stage of development.