Stripe’s valuation just hit $US95 billion after their recent funding, making them the most valuable startup in the US (and the third in the world, after Ant Group and ByteDance).

The company built a hugely successful payment gateway business with the initial focus on ease of integration. A few of my colleagues were amongst the first batch to integrate credit card payment on mobile, and they told us a lot of horror stories pre-Stripe, where merchant approval could take months (often because payment gateways did not understand your business model), and simple bug fixing involved engineers sitting across three continents (an undertaking on which the sun never sets)…

Anyway, thus far the success of Stripe is based on processing credit cards and debit cards – in countries where the penetration of these is high.

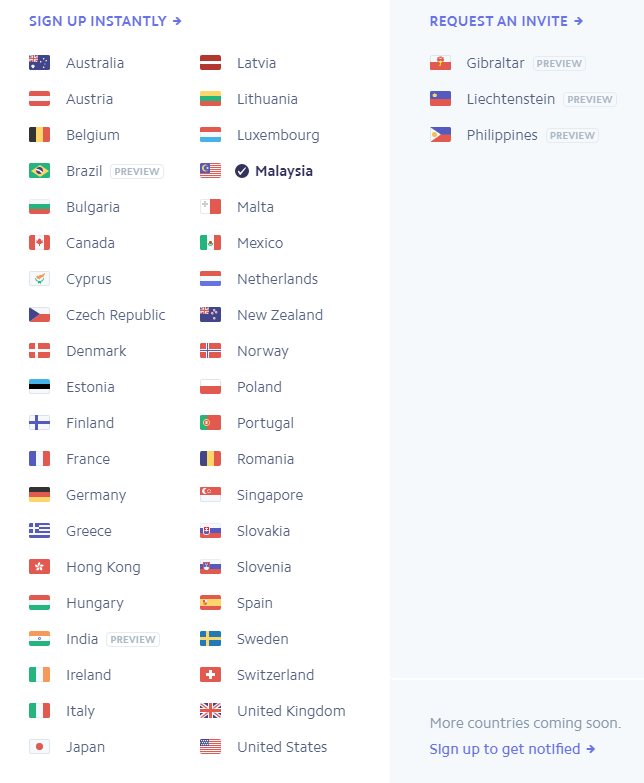

With the latest funding, a key expansion initiative is to enter emerging markets. It has launched a ‘preview’ version of services in Brazil, India and the Philippines. And Indonesia seems to be under the radar too.

Bahasa Indonesia language version is already available on the web site – they are probably in private beta right now, with the actual rollout expected pretty soon. However, Stripe isn’t exactly new to the Indonesian market as they launched an interbank transfer pilot project there back in early 2020.

And if you trust LinkedIn, Stripe also has a (sole) employee in Jakarta:

The trillion rupiah question is can they replicate their success so far in an emerging market environment – Indonesia in particular?

We have observed a lot of European, American and Chinese tech firms entering large emerging markets – while there are some success stories, failures are more common. Succeeding in such expansion is no easy feat – each large market is unique, with its own ecosystem and diverse set of interests.

It takes time and commitment to understand, expand and operate in a large emerging market. Let me explain a bit:

How localised is the product?

Currently the countries that Stripe are in have one thing in common: high credit/debit card penetration rates. Indonesia on the other hand, like most emerging markets have really low credit/debit card penetration; every 100 Indonesian possess 7 credit cards; versus every 100 Singapore residents, who hold 161 cards.

In 2016, when Stripe first entered Singapore, their target customers were those with credit cards. As at today, their current repertoire of payments have expanded a bit but seems quite geared towards developed countries like China or Singapore:

You would notice that many of the above ‘wallets’ are from reputable international firms, and often just an intermediary processing (still) credit and debit card payments.

If Stripe is to succeed in Indonesia, they’ll need to ensure their product can support payment methods offered locally.

This brings us to… the local payment gateways

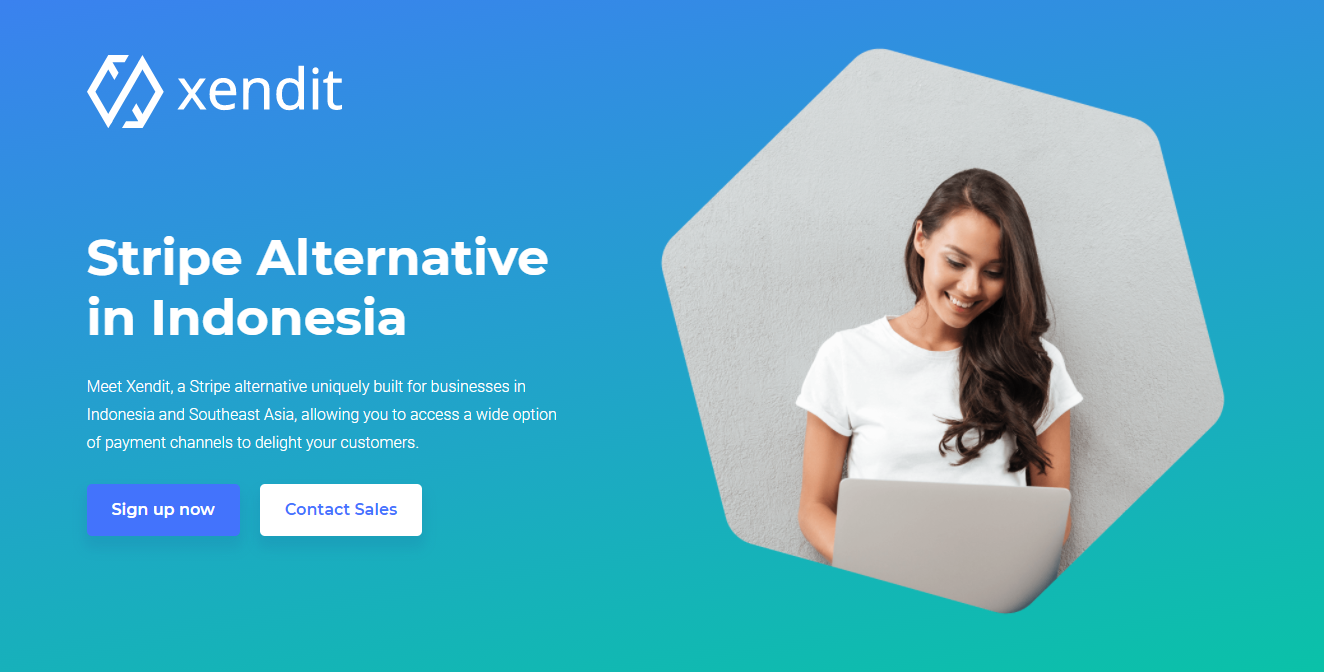

The payment scene in Indonesia has been growing fast in the last few years – together with the rapid growth of fintech, digital banks, ecommerce and digital economy in general. Key players that have been active in the market are Doku, Midtrans and Xendit.

Xendit, in particular, will be a serious competitor for Stripe – it is referring to itself as a “Stripe alternative” in Southeast Asia:

Xendit claims that you can create your own Xendit account within 5 minutes and accept payments. That is also in line with Stripe’s key value proposition of fast and painless integration.

The company now processes more than US$545 million transactions each month – that is not a small number for Indonesia.

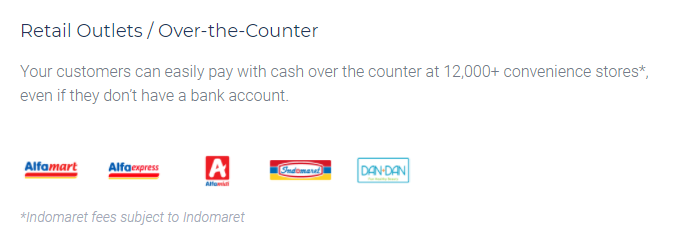

Xendit works with the biggest banks in Indonesia, cater to the key local e-wallets (Alipay and Googlepay are not part of these), credit cards/ debit cards and even buy now pay later partners.

In addition, Xendit also integrated offline payment methods, through convenience stores:

Onboarding these service providers, merchants and partners is no easy task. It involves not only just signing them up (for that any new player with a deep pocket can just poach BD managers of existing players), but to ensure that all the integration, settlement, reconciliation and customer service are done smoothly.

Do not expect every payment method to be as sophisticated, painless and straightforward as VISA/Master.

To excel and compete effectively, Stripe would need to open up to no VISA/Mastercard holders, this of course can be done but would take effort.

Do note that Xendit is also well capitalised for the market they are in – they just raised more than $60 million series B, led by Accel and announced a few weeks ago.

Traveloka beat international online travel agencies in Indonesia partly because of localised payment methods/acceptance. Would Stripe be able to crack this?

Organisation and leadership – The bigger challenges

We believe it could – ultimately given enough attention, commitment and hard work, the issues with local integration can be resolved. Local teams can be hired and local customers grievances properly addressed.

While Stripe is willing to go big in Indonesia – the volume there would probably not be very big for a while, especially compared to large, mature western markets. How much attention would you put in solving problems that are incomprehensible to product and business teams at the headquarters?

Alibaba expansion into Southeast Asia serves as a tale for caution. With an organisation centralised in Hangzhou, Alibaba (together with Ant Group) parachuted executives from its headquarters into the local countries, into Lazada and various Ant JVs in the region. And one by one, we saw the executives fall – each with their own stories but they all go back to the issue of local understanding, and commitment.

Even if they excelled individually, would the organisation and its leadership be able to give the whole support whenever needed, bearing in mind that the volume will be comparatively small for a while?

Of course, Alibaba’s business model is much more complicated than Stripe’s, and requires much more local operations. However, the broad categories of fundamental challenges are quite similar.

Conclusion – Lots of learnings from first movers

We have many Momentum Works community members that are using Stripe across the world. One of them from an emerging market told us that “Stripe is great for getting card payments up and running, but I’d probably use something else alongside for better coverage of local payment options”.

Stripe has a great warchest after its latest funding. It’ll need to be wise in determining how it wants to tackle the emerging markets.

In fact, sources tell us they’re in Indonesia through a deal with a local player which might be a smart move to jump through all the hoops we mentioned above.

However, let’s hope Stripe takes in the many cautionary references of emerging market expansions along the way – Lazada (owned by Alibaba) people management and Amazon’s demise in China.

We could also watch Stripe’s entry into Brazil, where the competition of payment gateways, as a Momentum Works community member puts it, is like “a fight with knives in the dark room”. Whatsapp Pay already learnt their lesson there.