Last Thursday, Momentum Works held an online sharing session “In focus: TikTok Shop”, where we covered unfiltered insights on the new ecommerce insurgent from our latest report, and discussed how stakeholders are responding to it. The full presentation deck is available for download here.

There were many interesting questions from the community of participants, which we did not have time to discuss. But as promised, here are our thoughts on some of the questions we received:

1. What is your sense of how Amazon will grow? Still seem to be a small part of others?

Amazon is a very rational company – they choose markets to enter or execute growth plans based on strong logic. Its ecommerce consumer business in Southeast Asia is currently only in Singapore now, where it has significant 1P volume including groceries.

Whether they will try to expand the market depends on their assessment – but we would think that developed markets make much more sense for Amazon’s operational structure and expertise.

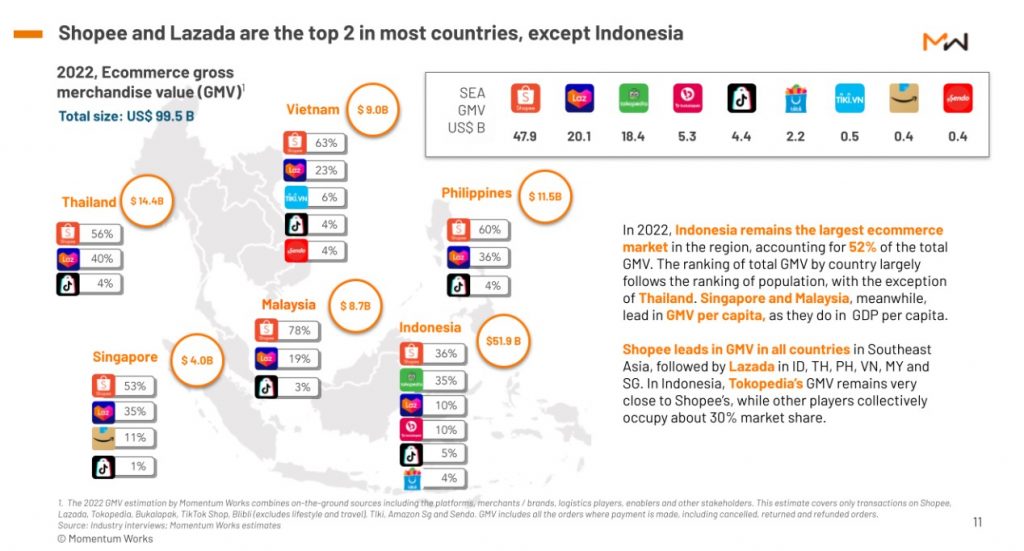

2. How about Indonesia’s specific market share? A number of players (Toko, Buka, Blibli) are only operating in Indonesia.

We had estimated the Indonesian-specific market share (2022) in our Ecommerce in Southeast Asia 2023 report (The page per se is outside the paywall). You can access the report here.

This market share would have evolved by now (August 2023) – as TikTok has grown significantly this year, while Tokopedia has been losing market share.

3. How big is TikTok’s balance sheet? Can they run these levels of losses (or more) for a long time?

According to Financial Times, TikTok parent ByteDance achieved a positive EBITDA of US$25 billion in 2022, which means they can perfectly fund the burn in Southeast Asia (and more markets).

What might change this equation? Potential adverse events that would impact their cash cow in China, or any structural/regulatory issues that could prevent them from moving money into TikTok. These seem unlikely now – what is probably more important is whether the leadership has the continuous commitment to invest in this market.

4. Why do you think Beauty & Personal Care is 7-9X bigger than Woman Fashion on TikTok? On platforms like Shopee/Lazada the 2 categories are a lot more balanced.

We believe it is a combination of different factors.

Beauty & Personal Care lends itself well to short videos. You can have various visually appealing content (that showcases makeup tutorials, skincare routines, etc.) that captures attention and encourages user interactions more readily than fashion-related videos.

The sellers, manufacturers, D2C brands of beauty and personal care products also seem to be more proactive to seize the TikTok opportunity.

Moreover, the current pool of content creators that specialize in beauty and personal care categories is much larger. They are also often more active and influential compared to fashion-focused creators.

5. What else do you see in common with products that have gone viral? For example, TikTok exclusive products, or having a set of products. Of course, price is an important factor, but are there other factors?

Price is definitely an important factor as sellers on TikTok Shop tend to offer these products at discounted prices or in value bundles.

The other common thing is the concept of virality and the randomness that comes with it. TikTok makes it possible for anything to go viral (recall the Makeba song which suddenly blew up again) and this randomness makes it difficult to predict what will happen next and how sellers should prepare/react to it. Sellers can try following trending TikTok formats to market their products and it might/might not do well – a possibility is to have multiple attempts to increase the odds, pretty much the same as gaming publishers and movie investors do.

6. How are the sales for virtual products, ie. vouchers for services/ hotels, been progressing through Tiktok Shop? Could you share some lights too?

TikTok’s current ecommerce capabilities still largely focus on the sales of physical products. Merchants offering virtual products often use TikTok for marketing purposes and will divert the traffic to an external site for users to purchase their products.

That said, Douyin has tried aggressively to sell vouchers for local services, including F&B and hotels. As far as we know, this assault on Meituan’s core business is less successful than Douyin had hoped – primarily because the redemption rate is not very high. You can listen to the latest Meituan earnings call to get some more insights.

7. Any sense of the chances of Temu entering the region?

Temu quietly launched in the Philippines on 26 August. We heard a few other markets might follow.

8. There is a lot being written about AI-powered virtual hosts in China’s live streaming ecommerce market. Any sense of how prevalent this is on TikTok in China? What percentage of sales may be through such virtual hosts?

AI virtual hosts are evolving fast – at the moment it seems that the adoption is at a smaller scale, and people see big potential in the long tail (like many manufacturers now run 24-hour live on their Taobao shop – where you typically see a very bored real human employee holding a placard while playing games on his/her phone).

That said, platforms are probably not going to endorse or promote AI-powered virtual hosts.

9. Is Meitaun doing food-related live?

Yes.

10. What are the key things (infrastructure, consumer behaviour etc.) to make brands in the USA move from marketplaces to streaming eCommerce?

Unlike marketplaces, live commerce requires more content related capabilities and talents that the brands (and their current partners) might not be equipped with.

As such, a well developed supporting ecosystem of trained live commerce hosts and multi-channel networks that support these hosts would be very important.

As we have indicated in The TikTok Shop Playbook report, the behaviour of watching video and buying things is not alien to American consumers. What is needed is for TikTok Shop to develop the content ecosystem, and convince brands to come onboard.

11. What are MW’s thoughts on TikTok expansion to Saudi Arabia? How do you view this market in comparison to the countries/regions TikTok Shop has already entered?

Saudi Arabia has an affluent consumer base which relies heavily on imported goods. Coupled with its mature cross-border infrastructure, it can serve as a decent market for TikTok to test and execute its consignment model.

We used to consult for cross border ecommerce in the Middle East back in 2017-2018 and we remember back then AoV of certain platforms could easily surpass US$90.

That said, the cross border into Saudi Arabia is now very competitive, with SHEIN deeply entrenched and Temu launching very soon.

12. Can Temu enter Indonesia? Because I remembered the cross border model is forbidden in that country

We do not think Temu should enter Indonesia in the short term – there is too much against cross border ecommerce in the current political climate in Indonesia. Whether a customized approach for Indonesia is worthwhile for Temu will depend on how the leadership sets priorities – many other things could bring more immediate benefits for Temu.

13. Is TikTok Shop showing signs of reaching growth headroom?

Yes and (more probably) no. For many users we might have reached the plateau of how many ecommerce videos we can feed them. However, there are many other ways to improve conversion – including the “shop” tab marketplace – and TikTok is actively exploring these.

The GMV is still growing, month over month.

14. So why could Tiktok be growing so fast entering the market in such a short period of time, considering Lazada and Shopee have been doing it for quite a while, is it more on the consumer behaviour side?

We have to know that what TikTok Shop has pulled off is not exactly a cold start.

Unlike traditional marketplaces, TikTok already has user traffic on its platform and does not need to dedicate as much resources and budget to acquire and retain users.

Leveraging the large amounts of time its users spend daily on the app, TikTok can easily influence consumer behaviour and trigger impulse purchases while entertaining them with a multitude of relevant video content.

This is in comparison to traditional marketplaces which need more time to build up the user base, have a much lower frequency of use and are only visited when consumers are already planning to buy something, which all results in much slower growth during the early stages.