This article is written by Visa Kannan, a partner at Saison Capital, and originally posted here. Republished on TheLowDown with the author’s permission.

Zomato released its full year results and hosted its first-ever earnings call with analysts. While the markets have since reacted positively to the results, there was also a lot of healthy skepticism. The Morning Context ran a piece on this and investors were tweeting about it.

In my view, Zomato really is the ultimate Rorschach Test because while the company has revealed a lot of information, the true picture still needs a ton of assumptions to be made. Based on what one’s general outlook of the market and Zomato specifically is, everyone has come up with their own interpretations and conclusions.

In this piece, I’m going to try and be as objective as possible in unpacking the results.

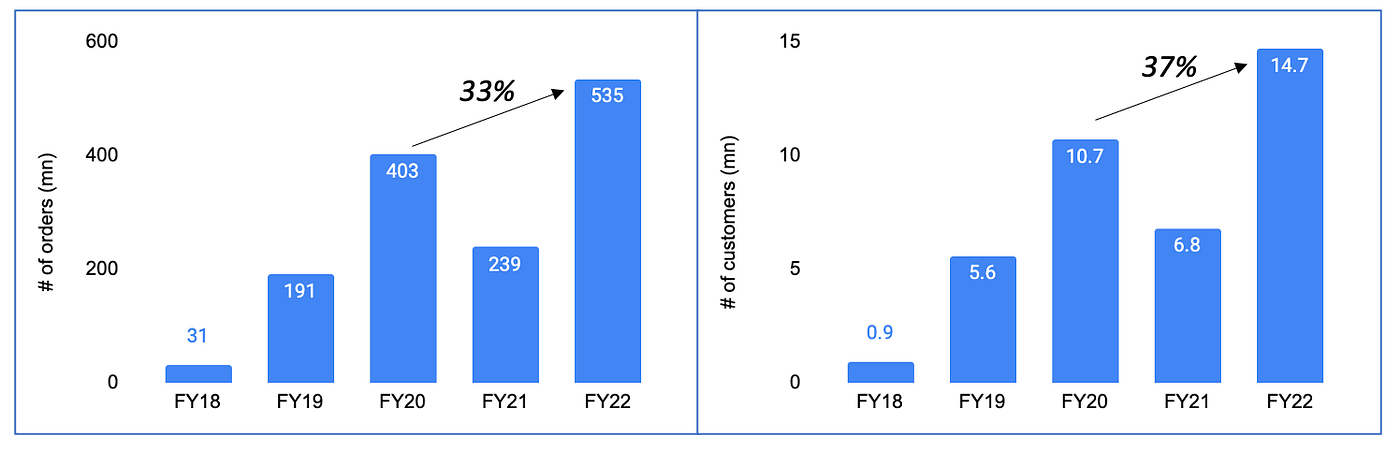

Growth: Companies at scale should be judged Y/Y

In terms of orders and monthly transacting customers, Zomato’s growth has been very impressive. FY-21 was marred by the pandemic, the start of FY-22 also coincided with the debilitating second-wave and to grow over pre-pandemic numbers despite one crippled quarter is quite remarkable.

The Morning Context has labelled growth as “sluggish” based on FY-22’s Q/Q numbers. But any business at scale should be judged by Y/Y growth. Once you do that, Zomato looks golden. Given FY-21 was a COVID-hit year, I’ve put in the Q3 and Q4 numbers from a “normal” year i.e., FY-19 (Q1 and Q2 numbers were not publicly available). Q3 growth FY-22 versus FY-19 was 97%, Q4 was even better at 118%.

The two charts side-by-side below:

Profitability: On the right track versus FY-20

There are 3 key metrics that matter for gauging the profitability of a food delivery business: Revenue Per Order, cost of delivery and promotional/marketing spend. Let’s get into each of these and see if we can determine how they have moved over the last 3–4 years.

1. Revenue Per Order (RPO)

RPO is the total margin made by Zomato at an order level. It equals basket size multiplied by the commission a restaurant is willing to share with Zomato.

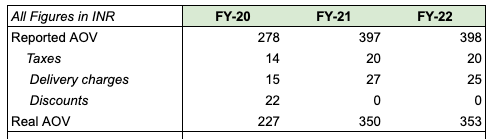

While Zomato has reported its AOV metrics, this number is inclusive of taxes, delivery charges and grossed up discounts. Based on a few assumptions, certain disclosures and accounting policies reported in the Prospectus, the AOV seems to have gone up by ~55% versus pre-pandemic levels. Detailed assumptions on all metrics here.

The fact that Zomato is looking to grow on the back of frequency as opposed to new user acquisition gives me some comfort because old users typically have higher basket sizes than new users.

A trend in the RPO number can be seen in the numbers Zomato has disclosed at various times. The prospectus states that the per-order commission in FY-20 was INR 43.6. Using the revenue numbers from the PnL the RPO is INR 63.3 for FY-21 and INR 63.8 for FY-22. So the money that Zomato makes on each order has improved by ~46% since FY-20.

However, what is concerning is that if the AOV trend and RPO numbers are correct, it means the commission % charged to restaurants has gone down from pre-pandemic levels: from 19.2% to 18.1%.

The optimistic view of this is that it could be purely pandemic related i.e., restaurants had a tough time staying afloat and needed to share less margins with the food delivery companies. The less optimistic view is that this is a sign of more competition in the space from the likes of Swiggy, the quick commerce players looking to improve basket size via “cafe” offerings and Tata Neu, which is planning to enter food delivery.

2. Cost of Delivery

From putting together various parts of the PnL, this has been the trend of Zomato’s delivery costs over the last 4 financial years:

If you don’t consider the Covid-hit year (i.e., FY-21), there has been a 13% increase in delivery fee in FY-22 versus FY-20. In somewhat acknowledging this, the shareholders letter states: “One could say that part of our progress on improving contribution margin is getting pulled back because of fuel price increase.”

3. Promotional / Marketing spends

The data certainly seems to suggest that Zomato has been able to generate significant efficiencies from marketing. Over the last 4 years, the money spent by them to generate 1 order has gone down Y/Y from INR 65 in FY-19 to INR-23 in FY-22.

I like this per order marketing spend metric a little more than the % of GOV metric, because in Zomato’s case GOV includes a bunch of line items that are not merely the cost of food and therefore complicates the numbers a little bit. This efficiency number is quite clean and clearly shows a pretty solid downward trajectory.

So What?

Putting all of this together, I’ve taken a crack at setting out Zomato’s Unit Economics. Assumptions and sources behind some of the numbers are here for those looking for the detailed view.

In my view, and this is where my subjective interpretation of the Zomato “ink blot” comes in: if you discount the pandemic year, growth and profitability are on the right track. While profitability versus FY-21 has reduced, this is largely driven by the increase in delivery costs (given increase in fuel costs and supply constraints on the availability of gig-economy labour). How Zomato navigates this will determine how its unit economics look in the next FY. One other key factor will be the competitive dynamics determining commissions.

Overall, given what I am seeing, I remain positive about Zomato’s path to profitability. I’m hoping to revisit these numbers each time Zomato publishes its results. Would love for operators to chime in with their interpretation of the results.