Last month, Momentum Works CEO Jianggan Li was invited to the Credit Suisse Speaker’s Corner. It’s a regular event that Credit Suisse hosts for their institutional clients in Asia and USA. The fireside chat topic was “ ASEAN Internet experts insights sharings – A deep dive into the digital economy” .

Varun Ahuja, VP of Credit Suisse Asia technology research team, hosted Jianggan at the event. Varun asked lots of pretty sharp questions over one hour, and Jianggan gave his detailed views. The questions and answers were so interesting and compact that we’ve decided to split the Q&A into 2 blogs.

In part 1 of the Momentum Works -Credit Suisse fireside chat, we deep dive into ecommerce, take rate, online grocery commerce and learnings from China.

Questions and answers have been tweaked for the ease of reading.

1.There has been a lot of interest in the ASEAN internet ecosystem recently with many companies looking to go public. How do you see the ecosystem evolving over the next 3-5 years?

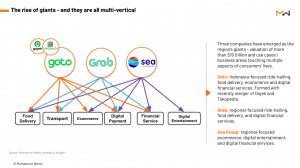

COVID-19 certainly accelerated the adoption for many industries. At the same time the ecosystem seems ready in terms of infrastructure, funding, talent etc. One thing worth noting is that opportunities in SEA are very similar across all markets, and mostly concentrated in the following 6 areas: ecommerce, fintech, local services, consumer brands, B2B, logistics. The evolving dynamics between the three giants: SEA Group, Grab and GoTo are also interesting to watch in the coming years.

- What is your view on ASEAN e-commerce market? Post the strong growth in 2020, how long runway do you have in terms of growth for the sector?

Southeast Asia is at an early stage in the development of a few areas. China offers interesting and useful lessons for SEA – the two regions are similar in stages of development and share to a certain extent the common supply chain.

There’s growth potential in a variety of areas. Based on the Momentum Work’s ecommerce in Indonesia report series, we see:

- Players are squeezing into the 2nd tier cities and rural areas.

- Brand games are becoming more prominent among players.

- On groceries, community group buy becomes a trend.

- Many players are also expanding into local services (food delivery etc.) and digital financial services

Ultimately, everyone is turning into an “everything store”. The key question is: will this growth be sustainable?

- Do you subscribe to the general view that there has to be one dominant player in the sector (like in China) to make money?

China did have a dominant player, but with the ascent of Pinduoduo as well as the real time commerce of Meituan – the dynamics are constantly changing.

In Southeast Asia, from a general glance there might be one dominant player, but chances are that some players will be carving out their niche to expand business areas, and gradually stand out in targeted sectors.

I believe strong companies with growth strategies will keep looking for growth opportunities, such as Grab’s expansion in digital financial services etc. It’s just a matter of time for the infrastructure to mature and business to take off.

- China’s ecommerce market has seen a lot of disruption over the last 3-4 years – social commerce, live commerce, influencer etc. How do you see these trends in ASEAN? Have the established players learnt from China and adopted their business models?

We see this emerging, yet it is too early to tell how it will evolve. Shopee and Tokopedia are experimenting with live commerce, though not yet to Chinese standards; Tiktok is experimenting with seller university; Facebook is making global announcements on live commerce; and on the ground people are investing in social commerce too.

However, there still lacks a clear classification on the model. In our upcoming report on Indonesia social commerce, Our definition of social commerce includes the below three aspects: 1.Content-driven; 2. Social + community group buy model; 3. Reseller base. Fundamentally it is customer acquisition at lower cost – as the infrastructure matures, whoever has lower CAC will have structural advantages over competitors.

In TikTok’s competition with Facebook in live commerce, both companies will struggle with priorities. Geography is a big challenge – can they both do something so far away from their home markets? They also have to decide where to direct the traffic – to advertising or ecommerce.But allowing influencers to directly monetise through commission will change the dynamics – and also how marketing budget is allocated.

- What is your take on the online grocery market which has witnessed a lot of traction recently?

Shopee has made into Indonesia’s online grocery market, but whether it will take off is yet to be seen. Groceries are notoriously difficult to tackle, as we see from the performance of various players in China. The fundamental challenge is how you can handle wastage, supply chains disruptions, and the price fluctuations that come along.

Essentially, players do have opportunities in the following 2 areas, and they’ll have to choose carefully which one to tap into. The first is the supply chain, and the second is the consumer facing part. We believe the second is largely taken up by the giants such as Grab and Shopee, and isn’t easy for new joiners to share the pie.

- Take rate: China has one of the lowest take rates (3-5%) globally while in other markets it is much higher (high single digit to low double digit). How do you see the take rates progressing in ASEAN?

If you look at Alibaba numbers, commission is 16% of revenue, and the so-called “customer management” – which is essentially marketing services, constitutes 46% of revenue. So the company is a customer traffic company rather than an ecommerce company – in this way I think Alibaba is different from Amazon etc. This raises an interesting question – shall we even care about take rate that much?

The situation in Southeast Asia is still difficult to see, as many platforms do not give clear take rates. I personally think the leading players from SEA are blessed to be able to learn from both Amazon and Alibaba- and to implement it better than both in the region. Will be interesting to see how Shopee will evolve as it matures.

7.Another key question from the investors is on profitability. When do you see the sector turning profitable? Further, how do you view the promotional activities? Will the GMV come down after the platforms stop subsidizing it (any learnings from China)?

Shopee is a great example to answer this question. I personally think Shopee’s free shipping is key to its profitability: (1) Cost is capped ; (2) It drives the flywheel ; (3) And it is executing it consistently.

Pinduodo is the only Chinese player that offers relevant learnings on ecommerce to SEA players, as the likes of Alibaba and JD were of a previous generation where customer acquisition costs were not that high, and subsidies not needed. In regards to GMV – GMV is inflated. Of course it will come down, but the question is to what extent? Fundamentally the answer comes down to whether you believe in ecommerce in Southeast Asia.

On food delivery

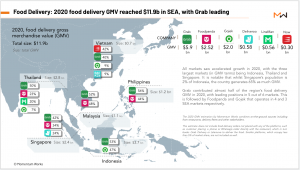

- The food delivery segment has witnessed strong growth post COVID. What is your view on the unit economics of this segment? How do you see it evolving over the medium term given Shopee’s entry here?

Each country is different, with exception of SG, where there is no labour shortage, and Grab is leading the overall market. I don’t see the numbers on unit economics, but I do think that Meituan provides a good reference point, which is below US$8 per order.

Shopee still has a lot to learn. They can learn it – but the bigger question is how much would that be a priority for them, especially now with their expansion into LATAM. All in all, it’s much harder for companies to crack the region, but if they do, it is a strong moat. You can check out more detail in our MW Food Delivery platform report.

Please stay tuned – Part 2 of the fireside chat will be released soon!