")

Southeast Asia tech investment reached a new high in H1 2021. And over the course of the past two years especially, we have received so many different enquiries from various investors on how to exactly see Southeast Asia, its diversity, consumption power, and various strategies of different startups.

They have seen all the numbers, read all the reports. However, there are some fundamental issues on which many still could not agree with each other.

Following a report and briefing on Tech investment in Southeast Asia H1 2021 with our friends at Cento Ventures, we want to summarise some of these fundamental perspectives about Southeast Asia, for international investors and key industry stakeholders.

This report will provide fresh perspectives on Southeast Asia, answering some key questions:

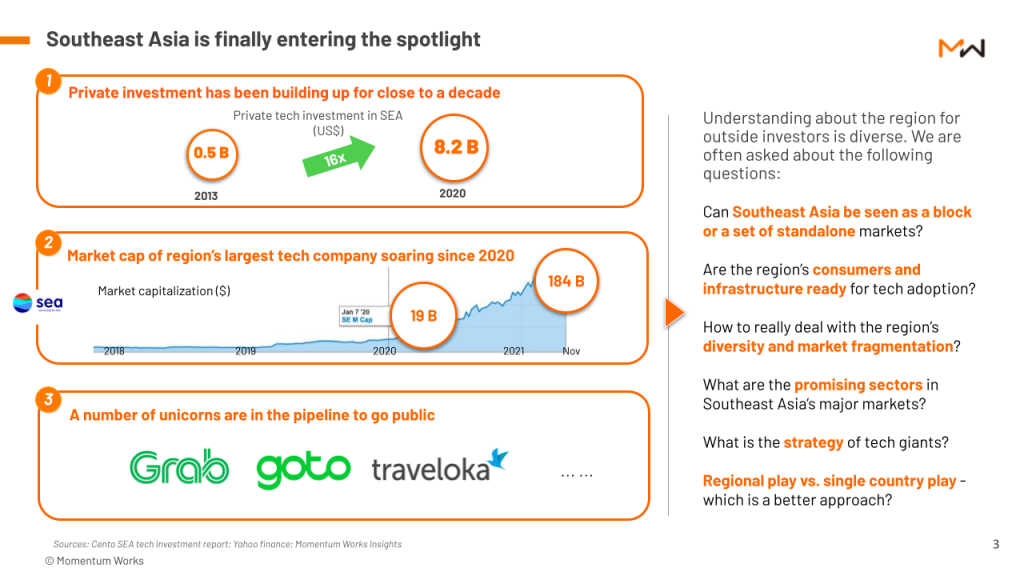

- Can Southeast Asia be seen as a block or a set of standalone markets?

- Are the region’s consumers and infrastructure ready for tech adoption?

- How to really deal with the region’s diversity and market fragmentation?

- What are the promising sectors in Southeast Asia’s major markets?

- What is the strategy of tech giants?

- Regional play vs. single country play – which is a better approach?

Here are some of the perspectives from the report. For more, you can acquire a copy here.

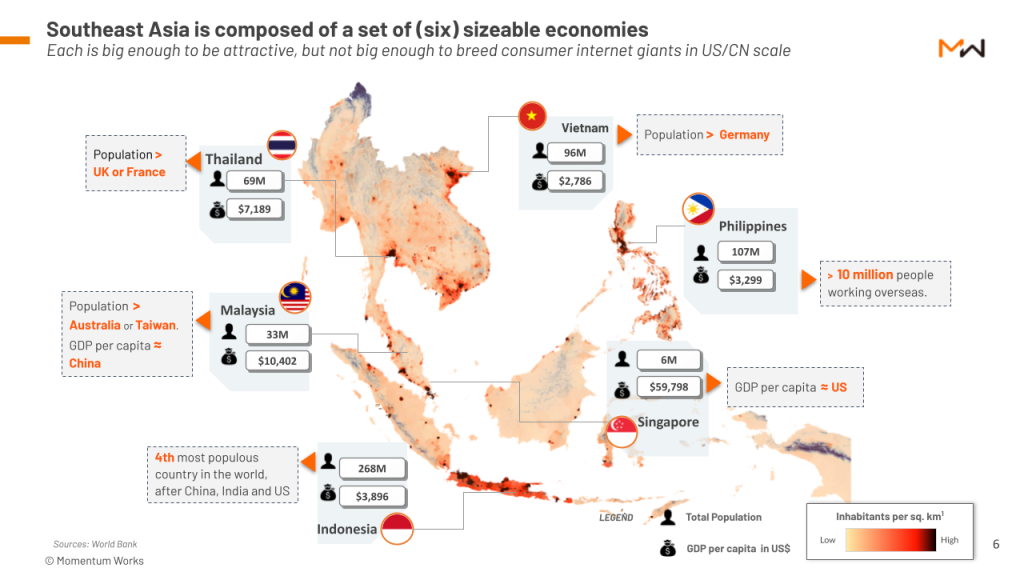

Perspective #1: Southeast Asia is a set of sizeable economies where megacities play a key role.

7 megacities in Southeast Asia (Greater Jakarta area, Manila, Ho Chi Minh City, Hanoi, Bangkok, Kuala Lumpur and Singapore) contribute 1/3 of Southeast Asia’s business activities and consumption.

This presents a key battleground for large tech players. The dynamics are different from the US or China where networks of large cities exist. Any major tech player will need to hold on to the megacity, and ideally a number of megacities to create a defensible strategic position.

Expansion from megacities to smaller urban areas is relatively easy, the other way round is very difficult.

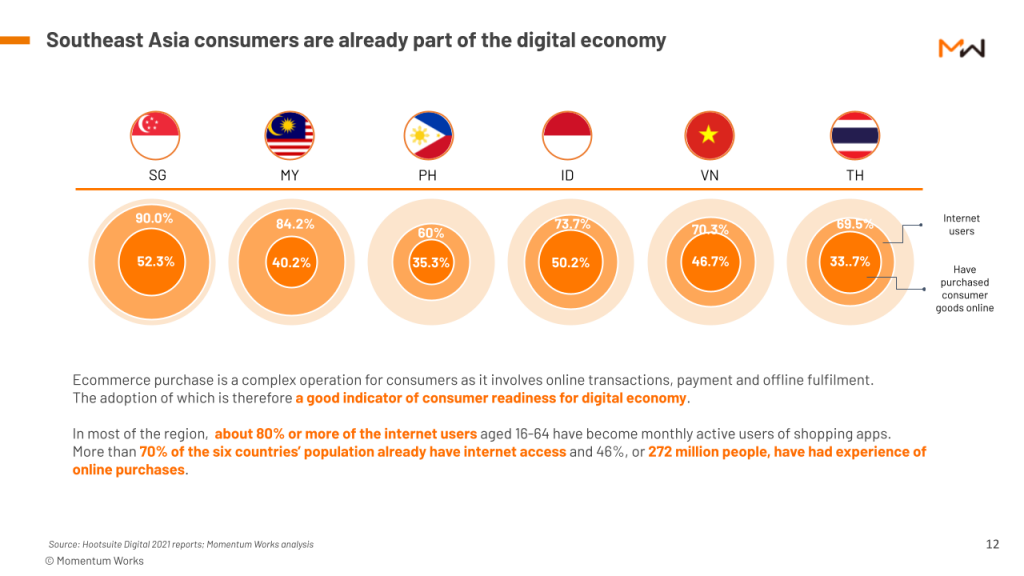

Perspective #2: Southeast Asia’s young, urban consumers are already part of the digital economy.

Southeast Asia’s population is digitally ready: more than 70% of the six largest economies are internet users, and 45% (272 million people) have made online purchases.

So the bigger problem is not whether people have access to the internet or how to make payment yet, but whether you have the right products and services for the variety of consumers with different personas, and whether they are willing and able to pay for such products and services.

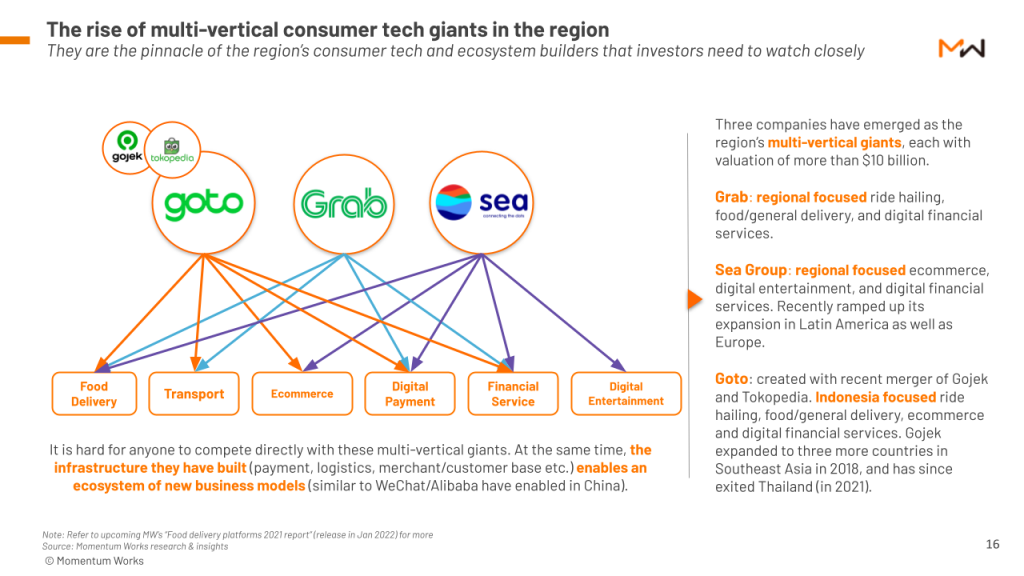

Perspective #3: Rising giants are competitive in slicing the market.

Whilst each country in Southeast Asia has its own characteristics, the major opportunities in the region are fairly consistent around consumer tech (e.g.: ecommerce, local services, mobility, digital payment, financial services).

These sectors often attract multi-sector giants (e.g.: Sea Group, Grab, Goto) to invest vast sums to seize market share.

The infrastructure these giants have built, including payment, logistics and merchant / customer base, can enable an ecosystem of new business models (similar to Wechat / Alibaba has enabled in China).

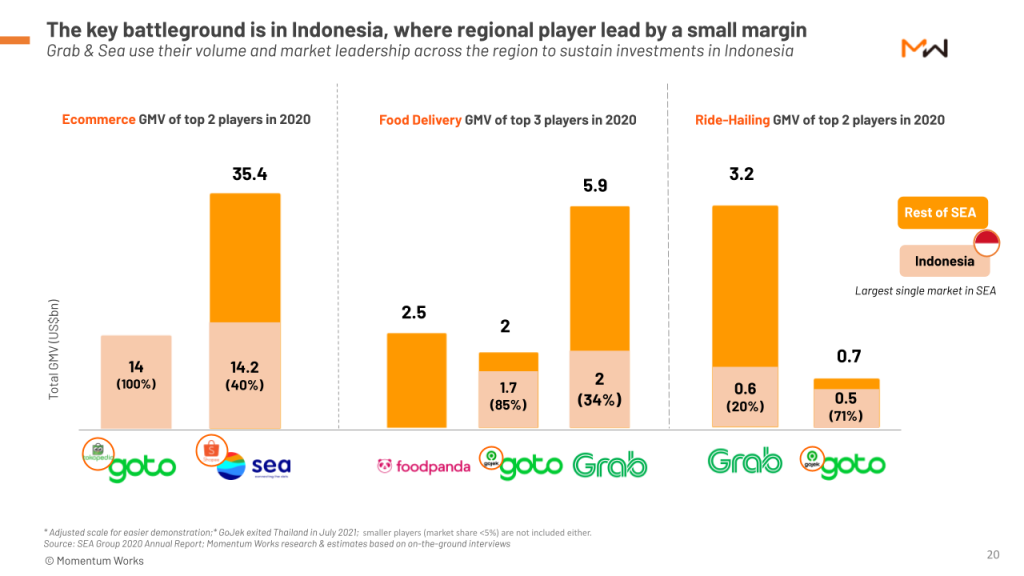

Indonesia, being the largest market by population housing 268M people, is the key battleground among big players.

Regional players like Sea group and Grab lead by small margin (in both regional and country level), tapping into their advantages in scale and leadership across the region.

We dissect more in the report on how regional giants and single country-focused country leaders compete, in a fiercely competitive environment; and what do leaders of each type need in order to win.

Our perspectives

- After a decade of investment and infrastructure building, and with the unfortunate event of prolonged Covid-19 pandemic, Southeast Asia’s booming tech sector has reached a crossroad: for the first time, outside investors, including the public market investors, are presented with multiple large size opportunities from the region.

- The emergence of multi-vertical consumer tech giants – Sea Group, Grab and GoTo – as public companies gives a new set of dynamics in the region moving forward.

- They will seize some of the major opportunities in the region, depriving direct competitors the chance of growing big. At the same time, these giants provide infrastructure for other sectors / opportunities that a whole ecosystem of new business models can flourish.

- As explained in this briefing, Southeast Asia’s diversity and management complexity serve as natural barriers – or moat – for new players to expand across the region; yet the consistency of opportunities across markets and the close proximity of the region’s commercial centres make regional tech plays attractive.

- It is probably necessary too – as we can see from the current competitive dynamics, even in the largest market of Indonesia (40% of the region’s population), the local champion GoTo is currently on the defensive against assaults from regional leaders Grab and Sea.

- The duo, after going through the tough journey of regional dominance, commands economies of scale, easier access to capital and talent, as well as the strategic depth / moat as explained in this report.

- That said, as the experiences in China have demonstrated, in a developing market when the landscape seems settled, the improvement of infrastructure and ecosystem education open up new opportunities for disruptions. Investors should be on the close lookout for the dynamics with the giants.

- Therefore, expect more opportunities ahead.

Access the report

You can get the above and more from a copy of the Southeast Asia investment opportunities report here.

By the year end, we will also be launching a report focused on tech investment comparisons between Southeast Asia and Latin America. Subscribe to our newsletter to stay tuned.

As usual, we welcome burning questions, enquiries and sharing at [email protected].