Luckin Coffee is making a comeback – it has relisted on Nasdaq and is launching in Singapore. But do you know what happened to Luckin’s founder Lu Zhengyao and former CEO Qian Zhiya?

After leaving Luckin Coffee over the massive financial fraud scandal, they have recently launched a new coffee brand – Cotti Coffee (库迪咖啡) in China. Cotti Coffee opened its first store in October 2022, and as of February 2023, it had 232 stores in China.

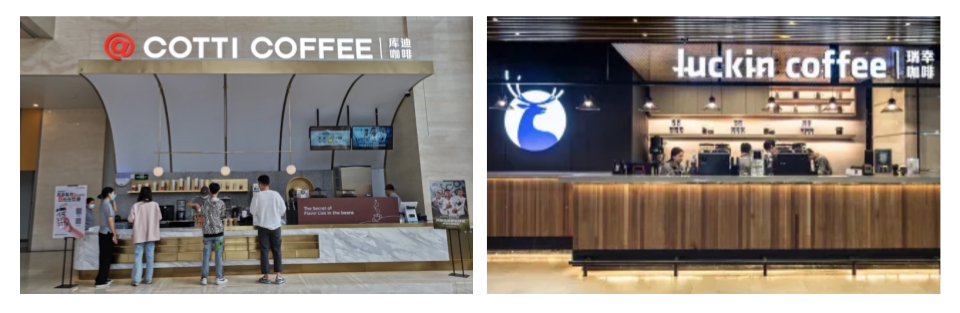

A search on the Chinese lifestyle review platform Xiaohongshu will give you some sense of Cotti’s look and feel:

Those familiar with Luckin will notice Cotti is very similar to Luckin (as well as other similar brands).

Cotti with Luckin’s DNA?

As opposed to TOMORO (a coffee chain started by logistic giant J&T), Cotti Coffee has been very open about its ties with Luckin. You can see Cotti’s marketing messages featuring “by the founder of Luckin” message:

Cotti Coffee adopts a similar product line and strategies as Luckin Coffee:

-

Similar product and pricing

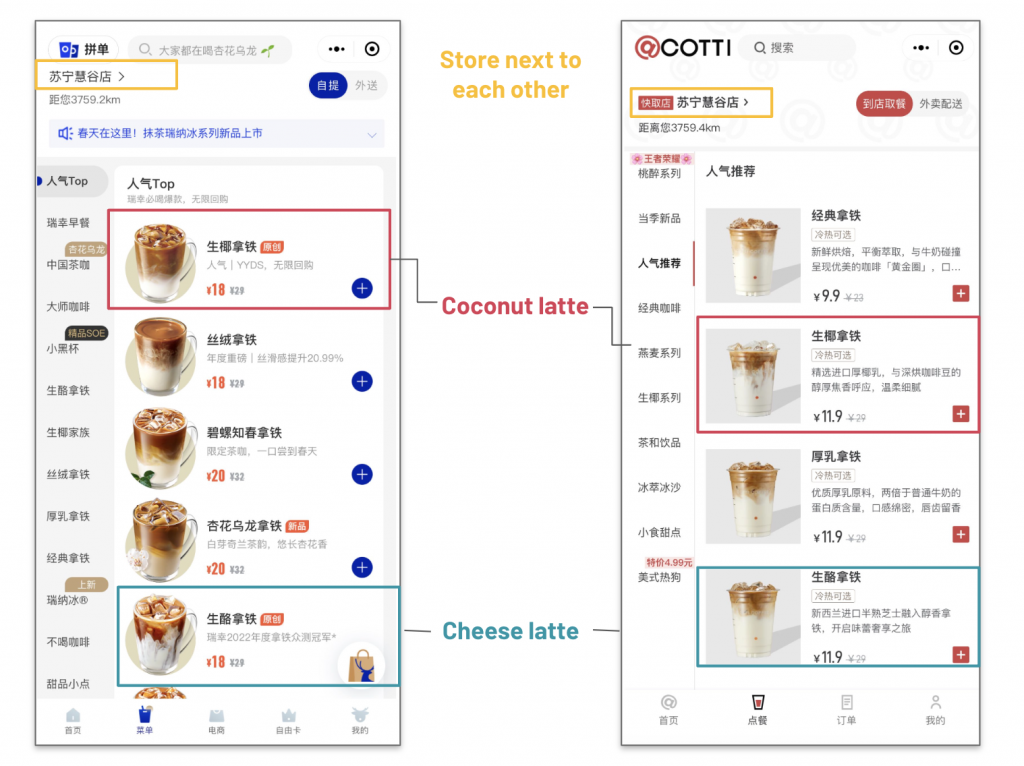

Both Luckin and Cotti focus on the latte series, with the best-selling items being the Coconut Milk Latte and Cheese Latte. They positioned themselves within the mass market segment, focusing on white collar and students (< US$ 2.90 for a latte vs. Starbucks’ US$ 4.50).

If you dig deeper, Cotti is priced relatively cheaper than Luckin: The price of a coconut latte is ¥11.9 (US$1.70) for Cotti and ¥18 (US$ 2.60) for Luckin.

Product and pricing of Luckin vs Cotti

-

Similar location selection, focusing on mass opening of stores

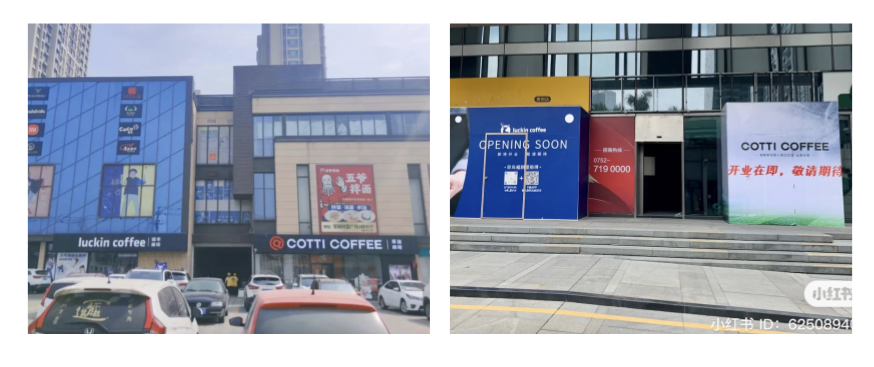

Cotti claims to focus on lower-tier cities, where “Luckin has missed” (32% of Cotti’s stores are in Tier 3 cities and beyond vs. Luckin, which has more than half of its stores in first-tier cities).

In reality, their markets largely overlap. In many locations, you can see Cotti placing itself next to Luckin.

-

Similar product marketing

Aligned with their mass market positioning, the tactics to acquire customers are also similar, e.g.: “Everything-¥9.9-coupons” and celebrity endorsements.

Cotti coffee was the 2022 Word Cup official sponsor of the Argentina football team in China

Celebrity endorsement is a common strategy of Luckin e.g.: Olympics’ freestyle skiing gold medalist Eileen Gu

The key difference lies in the expansion strategy

Luckin focuses mainly on self-operating model. It has only expanded into a franchise model in 2019 after having 3,000 self-operated stores.

Whereas Cotti focuses on the “joint venture” model from the get-go (which is, at its core, a franchise model – instead of charging ‘franchisee fees’, Cotti charges ‘service fees’, which is a % of the store’s gross profit).

Some of the benefits Cotte uses to promote its franchise model include “established by the founder of Luckin” and “full joint venture model with no self-operated stores”.

Cotti’s franchising benefits (official website)

Of course, as expected, some franchisees of Luckin have moved over to Cotti, or operating both Luckin and Cotti at the same time. You can see consumers on social media claiming

“the Luckin in my neighborhood has become Cotti”.

Will Cotti become a formidable challenger to Luckin and other major players?

Cotti will pose some pressure on the growth of Luckin (and other brands).

However, building a valuable and profitable brand amidst the saturated purple ocean market with low differentiation is no easy feat: Cotti has to find its way amongst strong players like Starbucks (“Third Place between home and work”), Luckin (with mass market pricing) and McCafe (“fast and easy”).

Despite the experience from (the success and fallout of) Luckin, the macro environment Cotti is facing today is also very different from that when Luckin first started in 2017. For example, Luckin had the luxury of a more favorable capital environment – ample funding has enabled it to expand massively on a self-operated model.

The competitive environment today is also much more saturated: Many players have emerged post-2017, including Mixue’s Xingyunka 幸运咖 ( > 1800 stores) and Nowwa (> 1200 stores).

Top coffee brands in China by the number of outlets

Top coffee brands in China by the number of outlets

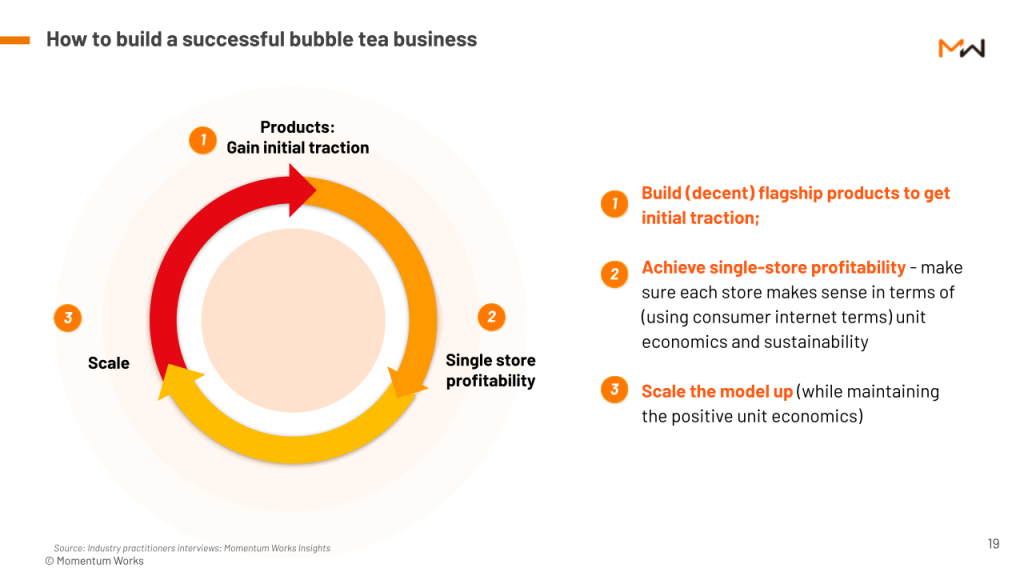

Ultimately, F&B chains (from coffee to bubble tea) have similar underlying logic – this offers various learnings for operators:

How to build a successful F&B brand? It is a lot harder than it sounds.

You can refer to our Bubble Tea in Southeast Asia report as the two industries have a lot in common.

The question comes down to: who can continuously captivate more consumers? Who can keep consumers engaged and capture a more significant share of wallets, while also maintaining positive unit economics and generating a good return for the shareholders?