Used car marketplaces in China are going through a tough time.

Rumours about massive cost cuts about major players appeared right after Chinese New Year – mostly in forums where employees share gossip and express grievances.

As the coronavirus situation developed, all these rumours were confirmed.

Chehaoduo, the parent company of Guazi, is ‘temporarily’ cutting the pay of employees by 30-50%. The more senior ones get the biggest cuts.

Uxin, the first used car marketplace to go public, announced a package where employees are divided into two groups: those who are taking no-paid leave but with a basic allowance, and those who take up to 40% pay cut to stay on the job.

Yao Junhong, founder of Souche, revealed that the company had recently cut more than 10% of the workforce. While Chezhibao, another player, has simply vanished.

The macro fundraising environment, since 2019, has not been favorable for companies with massive burn rates.

Coronavirus provides the double whammy: dealers are not back to work, logistic networks are curtailed, and people staying at home are not buying items where physical inspections are needed.

However, while the virus outbreak provides a convenient excuse for cost cuts, the industry is facing fundamental challenges.

No Middlemen!

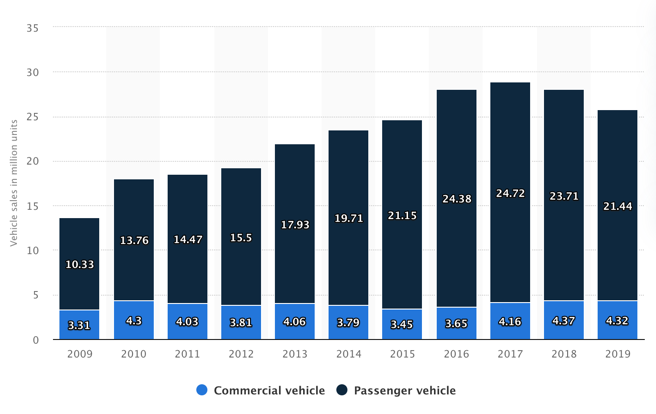

The automobile market of China has undergone massive growth over the last decade. Between 2009 and 2019, more than 250 million passenger and commercial vehicles were sold in the market.

The conventional wisdom goes – a few years after the explosive growth of new car sales, used car sales will shoot up. Consumers seek to upgrade their cars, other consumers and businesses look to buy cars cheap.

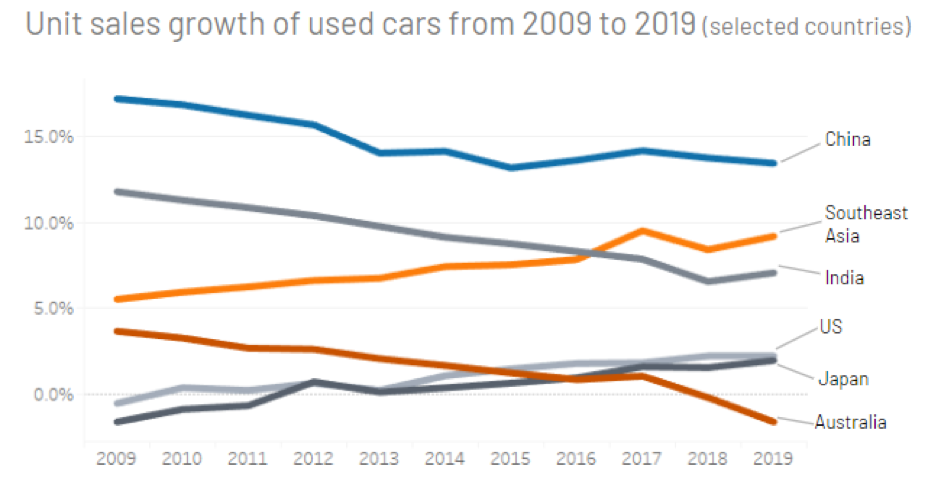

In the US – a more mature car market, used car sales volume has held steady at about 15% of the total registered car population.

Most of the used car marketplaces in China entered the fray around 2014. The promised huge market, the fragmented offline trade (more than 150,000 dealers, none of them very big, one estimate went), and the price differences between cities, make this industry very attractive to capital.

Guazi emerged in 2014, founded by Yang Haoyong, who had merged his previous classified venture, Ganji.com, with 58, the market leader.

Renrenche was also launched in 2014. Its founder, Li Jian, used to hold senior posts at Baidu, 58 and Microsoft. It raised more than US$100 million before the end of 2015.

Uxin, which started earlier, raised more than US$400 million in two successive rounds in 2014-2015.

The platforms above adopted the C2C model, allowing sellers and buyers to connect directly through the platform, which also provides a series of services (inspection etc.). The theory is: if the middlemen are eliminated, value is captured by buyers and sellers, and shared with the platform.

Other models also emerged, such as Souche, which focused on SaaS for dealers.

With the massive capital, the platforms started running. Most of the money is probably spent on advertising – for a long period of time, “Sell direct! No middleman to earn the spread!” Guazi’s ads were omnipresent on TV, on radio, in the lift lobbies, and popping up online. Even school kids who would never buy a car anytime soon were able to recite this slogan.

Burnt, and burnt

Fast forward to 2019, where cracks became quite obvious in the industry. Stories of layoffs, cost cuts and closures proliferated.

Renrenche was rumoured to be close to demise. It would have gone if not for the lifeline Didi threw.

This is how Uxin, the only company which managed to go public, is performing:

Not to mention that Uxin has largely become a car financing origination platform.

Not to mention that Uxin has largely become a car financing origination platform.

Guazi is not in better shape either. Its parent Chenhaoduo announced US$1.5 billion funding from Softbank Vision Fund early last year. However, rumours are saying that the funding is tranched and conditional. Stories of Guazi’s outlet closures, layoffs and cash flow crunch regularly made headlines since May 2019 onwards.

So what happened?

In China, since the ride-hailing battle, both investors and founders are used to the internet way of cashburn-fueled high growth. Used car markets followed the same playbook – massive ad spending and discounts to lure customers from offline, as well as competitors.

Whoever establishing an upper hand will crowd out competition and reap the market – the playbook goes.

The playground seems to be up for all vertices in order to support the top line – financing, leasing, new car sales, brokered C2C deals, yet no one seems to be able to pin point the value created by these platforms that justifies their valuation.

They have effectively become the middle man in everything.

When the funding cycle changed and they can no longer through cash to disguise their ambiguous role in the ecosystem, the veil is lifted one by one. Massive pay cuts and firings are underway.

In contrast, understated supporting services like Che300 that historically have focused on one thing and a clear value – pricing, for example – remained standing.

Lessons for players in Southeast Asia

Southeast Asia has seen a surge of interest in used car marketplaces over the last few years too. Carro, Carsome and Belimobilgue have collectively raised more than US$100 million now.

Carsome and Belimobilgue focus on C2B, while Carro practically tried everything, recently pivoting to an emphasis on unsecured financing.

The market, with 4.7 million used cars sold in 2018, is attractive to investors, entrepreneurs and financiers.

There are plenty of lessons the players can draw from the all out battle in China while risk leaving no one standing. However, we think the key here is to not burn for growth, but to focus on value creation, such as building inspection standard, pricing mechanism, and actually capturing and using real transaction data – all things that this market desperately needs.

Momentum Works has conducted some systematic study about the used car marketplaces in Southeast Asia and will be releasing a report in the coming weeks. We have a limited number copies of the report for free dissemination, if you are interested in obtaining a copy, please write to [email protected]