We at Momentum Works have been keeping track on a lot of trends lately, and we have discussed before about Facebook’s ambition in ecommerce. It is a fact that Snapchat is immensely popular especially with the young (even in Southeast Asia), and even after discounting the users who do not use Snapchat, Facebook is still increasingly being perceived as “old” and out of style. That being the case, Facebook is definitely losing its ground, and needs to change fast.

This is not hearsay, as the slew of news recently covered Mark Zuckerberg’s intentions to change Facebook’s algorithm to serving less “news contents” and going back to more what it used to be, despite potentially losing billions of dollars in revenue.

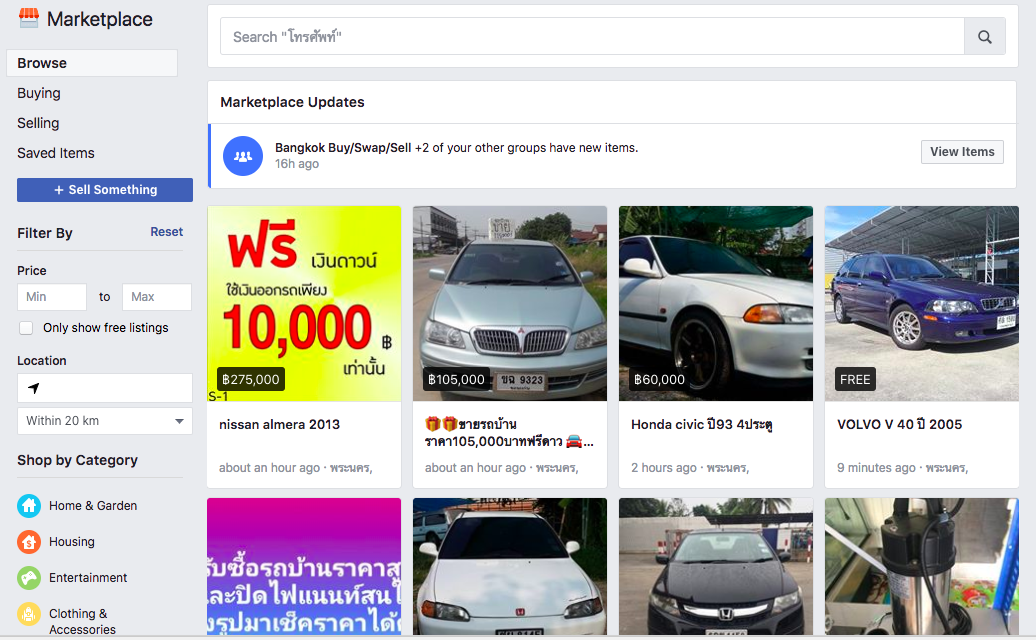

Enter Marketplace – why now?

If we actually look at China (where Facebook is actually banned), people continue living their lives (still connected, unfortunately – to Facebook’s dismay) relying solely on WeChat. This has not only made Tencent ultra successful, but a global powerhouse. First designed as a chat app, it has expanded to include many other features which Facebook has, but many that it does not.

One can shop on the WeChat app, pay and even receive money on the WeChat app. Can one do that on Facebook? That is what they are working towards. Our take is that, in order to enter China, Facebook needs to be better than WeChat, and they have no choice but to improve. Our experience tells us that the Facebook marketplace does not need to be the profit driver for now (except maybe to be able to sell some ads), but rather just a stepping stone.

Finding the catalyst for its payments business

As we shared earlier, the key to driving up Facebook’s usage and continuous relevance is to provide an all encompassing experience to users, similar to what WeChat provides. The first thing that comes to mind, is of course to provide payments. There’s no surprise here as even Zuckerberg talked about blockchain and issuing Facebook tokens.

However, regulations are going to take time to navigate, judging from the amount of markets Facebook is in – it is easier to say, which markets are they not in. Are they going to wait for government approval? Let’s just say they will not wait for anyone.

The secondhand market is actually quite lucrative (attributing to the success of Carousell, and to some extent, Reebonz), and that it could actually be a really timely move for Facebook to launch its marketplace as a catalyst for its greater ambition – payments. We will not be surprised that they will launch their food delivery business in Southeast Asia in the near future, as they did in the US in late 2017. They would do anything to dominate.

Could Facebook be a bank?

Absolutely! The rise of digital banks has not gone unnoticed, and neither has the shuttering of traditional banking branches in Southeast Asia. The Hong Kong Monetary Authority (HKMA) recently issued the Guideline on Authorization of Virtual Banks, which proves our point that governments around the world are taking notice that traditional banking structures are increasingly less important as users take to digital banking and transacting online.

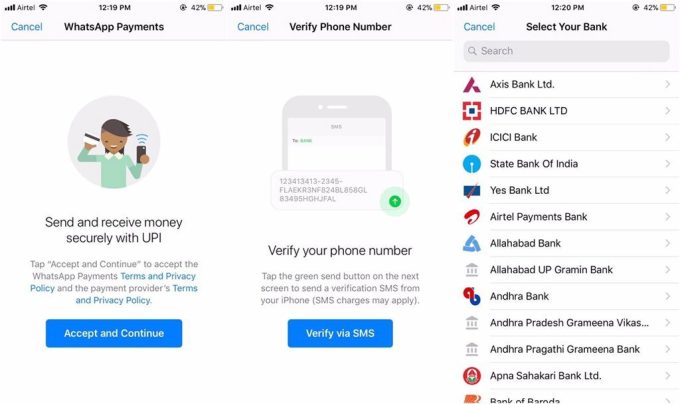

Perhaps for a company like Facebook, this is already in the works, just as Whatsapp recently launched person-to-person payments in India to challenge the dominance of Paytm (owned by Alibaba). Having the biggest user base on the planet would not only make it the most formidable contender in this space, but perhaps the most valuable.

In the meantime, Thailand (like many other developing markets) has a huge rural population and less financially savvy users. So the country is expanding low-cost banking option by using agents. Either way, it is a different solution to the same goal – to increase financial inclusion (with a nice knock on effect of increasing profits).

Conclusion

Facebook may not be losing a huge amount of users tomorrow, but it does not mean they cannot be taking defensive and offensive positions to protect their source of revenue, i.e. users. If that means offering Facebook users more features – e.g. marketplace or payments, then so be it! Marketplace or payments may not be huge income generators in the near term, but will instead generate tonnes of data points, which is far more valuable to advertisers.