Momentum Works’s third annual “Food Delivery Platforms in Southeast Asia” report was launched this week, answering key questions from investors and stakeholders on the macro landscape, players, and challenges during the post-pandemic period.

After two years of significant growth, combined GMV of food delivery platforms in Southeast Asia grew at a more modest 5% in 2022, to US$16.3 billion.

The report is complimentary – you can download your copy here.

A question that every investor and industry practitioner is concerned about is: how will the platforms achieve profitability, now they must?

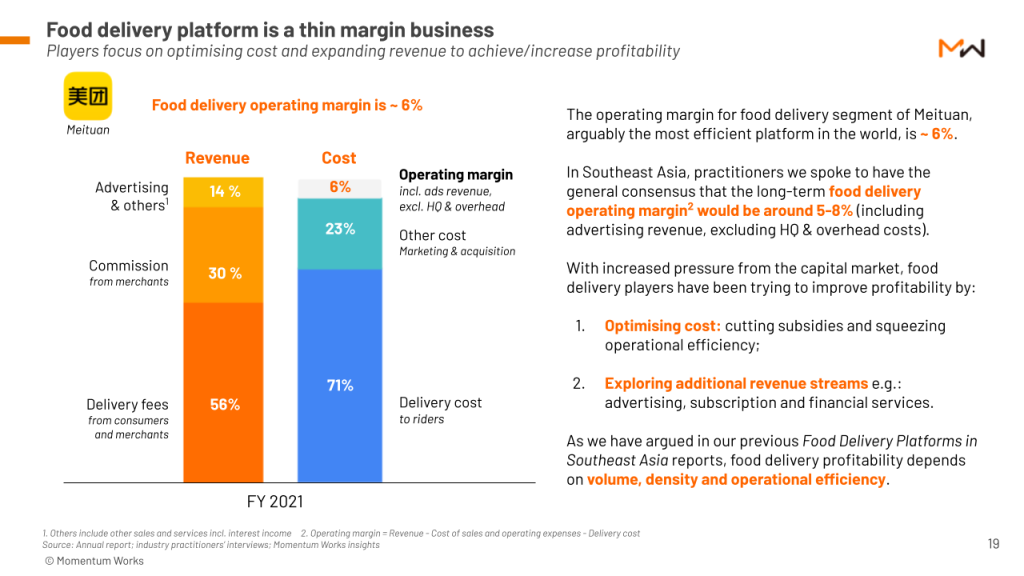

For starters, food delivery is a low margin business; as we have mentioned in our previous edition of Food Delivery Platforms in Southeast Asia report in Jan 2022, profitability is attainable through volume, density and operational efficiency.

As a benchmark, Meituan, arguably the world’s most efficient food delivery platform, achieved a food delivery operating margin of ~6% in 2021. Note that this is achieved through relentless optimisation over the course of eight years since 2013.

Players in Southeast Asia are taking mainly two types of initiatives: optimising cost and expanding revenue streams.

Let’s look at costs first – There are three ways of optimising cost:

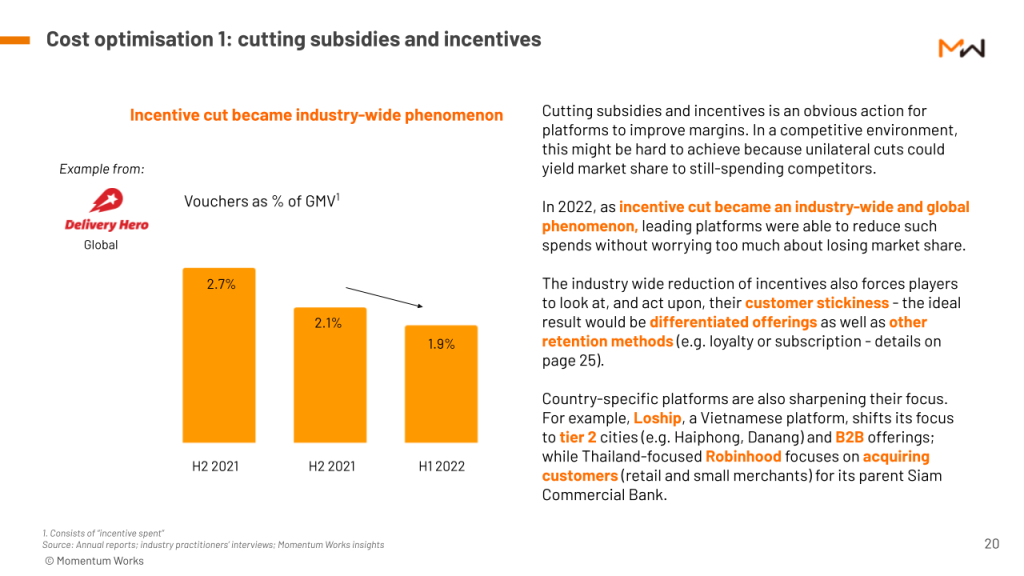

1. Cutting subsidies and incentives

Everyone understands this – the question is how to balance growth and customer retention.

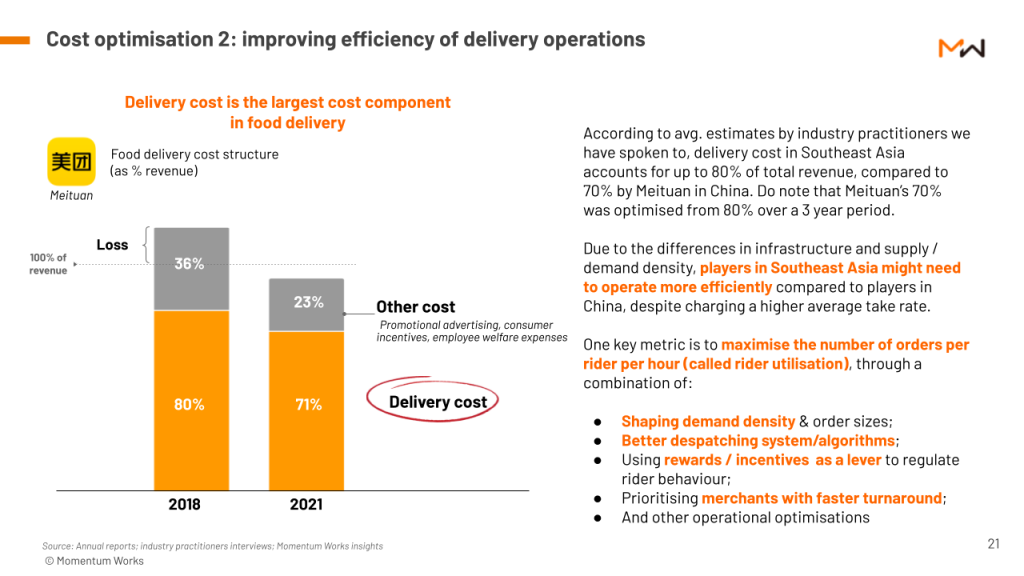

2. Improving efficiency of delivery operations

Over the years, Meituan has made a lot of investments into optimising its delivery operations to achieve profitability: cutting delivery costs from 80% of total revenue in 2018 to 70% in 2021.

The question for the players in the region therefore, is how to keep increasing order volume and density, while at the same time improving the efficiency of delivery operations – this will be a long-term game which, as mentioned above, requires relentless effort.

One key metric is to maximise the number of orders per ride per hour (i.e.: rider utilisation), as we have discussed in the report.

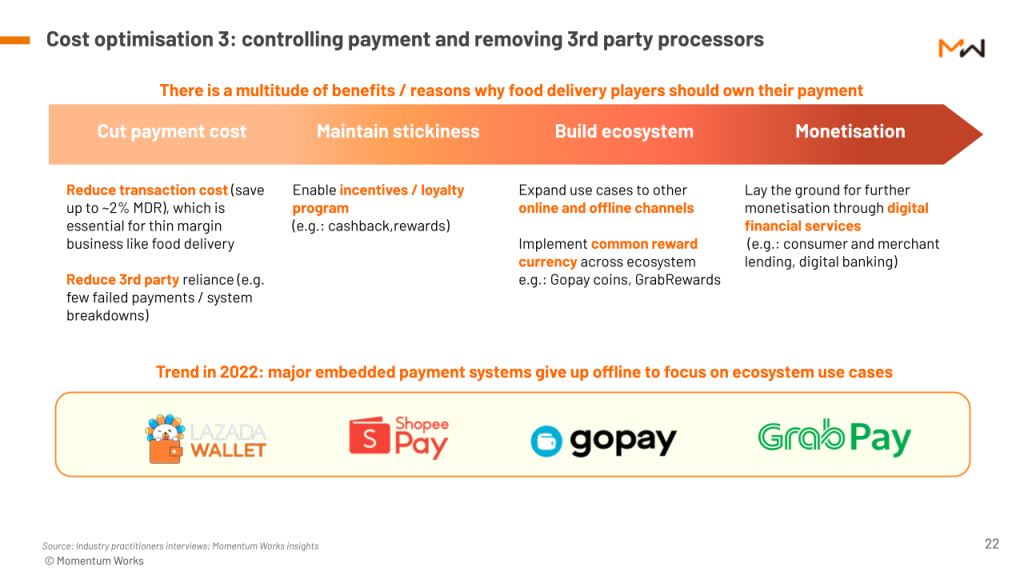

3. Controlling payment and removing 3rd party processors

As delivery platform is a thin margin business with single-digit operating margin, paying 1-3% to payment processors is obviously not an ideal situation.

Key food delivery platforms (Grab, Goto, Foodpanda, LINE MAN WongNai) have also integrated their own payment systems/e-wallets onto its platform.

In our previous article: Why do ecommerce platforms build their own payment, we have also mentioned at length about the ultimate monetisation game plan for payment, through digital financial services e.g.: lending, investment, and digital banking. But increasing conversion and reducing cost through removing 3rd party dependency in this core part of the transactional platform is the first and foremost objective of building own payment rails.

More insights

Ultimately, optimising cost is only part of the equation to improving profitability. A bigger part comes in the platforms’ ability to leverage its existing infrastructure, user and merchant base, to expand into other revenue streams, which we will discuss in part 2 of this article.

The Food Delivery Platforms in Southeast Asia report is free – and you can obtain your copy here.