This commentary first appeared on Sheji Ho’s LinkedIn article. Republished here with permission. You can access the other commentaries from the author on the same website as well.

This is a follow up on something I previously posted on LinkedIn:

On a long enough timeline, every startup in emerging SEA (ex. Singapore) will either:

1) become an ecommerce enabler or add an enabler / managed service component to its business; or

2) become an offline fried chicken or some other F&B brand

IYKYK

Fight Club (1999)

A few conversations with people in the SEA tech space (you know who you are) leads us to refine this “fried chicken theory” a bit more:

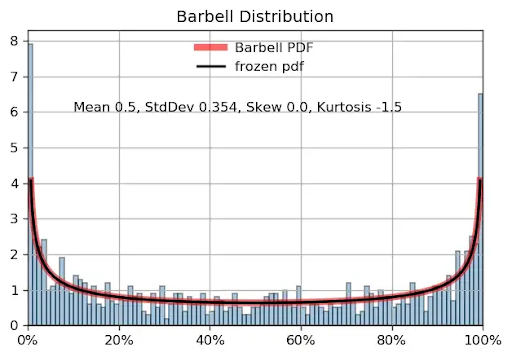

Unpopular opinion: The startup business model opportunity in emerging SEA (excl. Singapore!) follows a barbell distribution, instead of a normal distribution.

Let’s look at this from a few perspectives to understand why:

a) Value chain – “Do you add value and are you hard to replace?”

Applying the barbell distribution theory, the real business model opportunities accumulate at the very edges of the value chain, i.e. the most value is in:

- Controlling / aggregating users at scale (Stratechery’s Ben Thompson!) – i.e. marketplaces (Shopee, Lazada, etc.), media (TikTok, etc.), super app platforms (Grab, GoTo), etc.

- Controlling the ‘product’ i.e. being a manufacturer, owning heavy assets (hospitals, F&B, hotels, airlines, warehouses/fulfillment centers, delivery fleets), owning a brand (e.g. for D2C), being a bank or insurance company, owning technical IP, operating a school, etc.

Like in Netflix’ Narcos series, the biggest value is in product (Columbia) or distribution (Mexico).

Narcos: Mexico

That said, like in the image of an Olympic weightlifter below, there is an opportunity in the middle but it requires a more “heavy lifting” i.e. a tech-enabled / managed-services approach. (This is the part referred to in the “fried chicken theory” as ‘become an ecommerce enabler or add an enabler / managed service component to its business’.)

Olympic lifter Lasha Talakhadze lifting 258 kg at the 2016 Olympic Games in Rio, Brazil (Wikipedia)

Whereas the edges are more scalable but require “heavier assets”. Think scaling an ecommerce marketplace or ramping up production in a factory.

You control both product and distribution? Congratulations! You’re now full-stack i.e. you’re a typical Southeast Asian conglomerate.

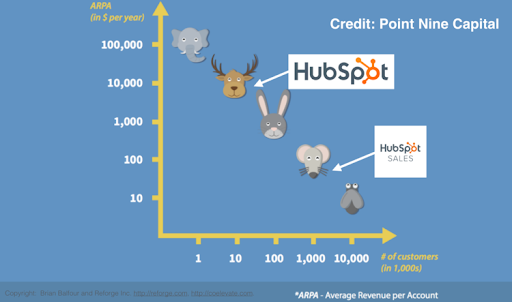

b) Monetization – “Can you get people to pay for the value you created?”

Again, applying the barbell distribution hypothesis, there’s max money to be made from the “edges”.

Brian Balfour of Reforge has written extensively about this. He has this really intuitive chart showing ways to monetize ranging from making a little bit from millions of users all the way to charging a lot to a few really big customers.

Building a Growth Framework Towards a $100 Million Product (Brian Balfour)

But what if it’s an “either or” case in emerging SEA markets today?

- Charging small amounts but monetizing millions of users – e.g. ecommerce / marketplaces, super apps / ride hailing platforms, logistics / delivery, F&B, etc.

- Serving several really big accounts with higher average revenue per account (ARPA) – e.g. ecommerce enablers

This isn’t to say there’s no money to be made from mid-sized customers but it’s just much harder to scale monetization efficiently i.e. make the CAC or GTM justify the returns. This is assuming you can get those (M)SMEs to pay in the first place. Unless… you monetize mid-sized customers as part of your marketplace, see ecommerce marketplaces like Shopee, Lazada, Meituan, Taobao, etc.

Obviously there are exceptions to the rule as well as variations and nuances across different verticals and industries but this is based on what I’ve observed in SEA so far. I don’t have empirical data to support this so take it for what it’s worth. Also note I didn’t say which models are the most investible. Two different things.

As a previous operator in the ecommerce space in SEA and currently building a healthcare startup, I’m seeing the same patterns in healthcare. On one end, you make money via heavy assets by building hospitals or clinics and/or consolidating them. On the other end, we’re aggregating millions of patients similar to ecommerce marketplaces. And then in the middle you have tech-enabled healthcare business that can grow to billions of dollars but mostly in developed markets.

The Six Stages of Health Tech Grief (Out-of-Pocket Health)

Extrapolating from here, and applying the barbell theory, these are some areas I think could work well in emerging SEA:

- Unbundling of general ecommerce marketplaces – e.g. vertical ‘ecommerce’ (assuming TAM big enough of course) such as HR/jobs (most job platforms are running on early 2000s interfaces), healthcare, beauty/lifestyle upgrade, parenting, etc.

- Creating new products (not D2C; D2C just a channel) – e.g. new local F&B brands (fried chicken theory) e.g. food, coffee (welcome back Luckin!), etc. Not whitelabeling Chinese OEMs mind you… it’s hard to compete in that space without having the world’s biggest factory sitting next to you.

Have you seen similar patterns? Would love to hear your thoughts.

Liked this article? Read some of my previous posts:

Super Apps: Nothing Much Super About Them