Momentum Works’ third annual “Food Delivery Platforms in Southeast Asia” report was launched this week, answering key questions from investors and stakeholders on the macro landscape, players, and challenges during the post-pandemic period.

After two years of significant growth, combined GMV of food delivery platforms in Southeast Asia grew at a more modest 5% in 2022, to US$16.3 billion.

The report is complimentary – you can download your copy here.

With mounting pressure to reach profitability, we see more strategic sharpening of food delivery platforms to achieve profitability/self-sufficiency faster. Among that, cost optimisation and expansion of ancillary revenue streams are recurring themes of 2022.

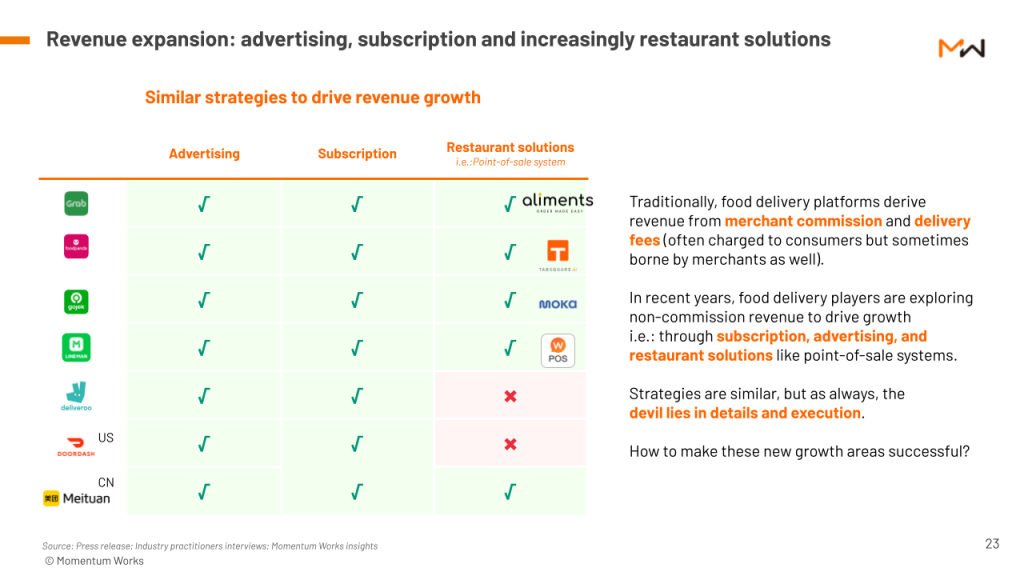

In terms of revenue, food delivery platforms are exploring beyond merchant commission and delivery fees to drive sustainable growth. This includes subscriptions, advertising and restaurant solutions like point-of-sales systems.

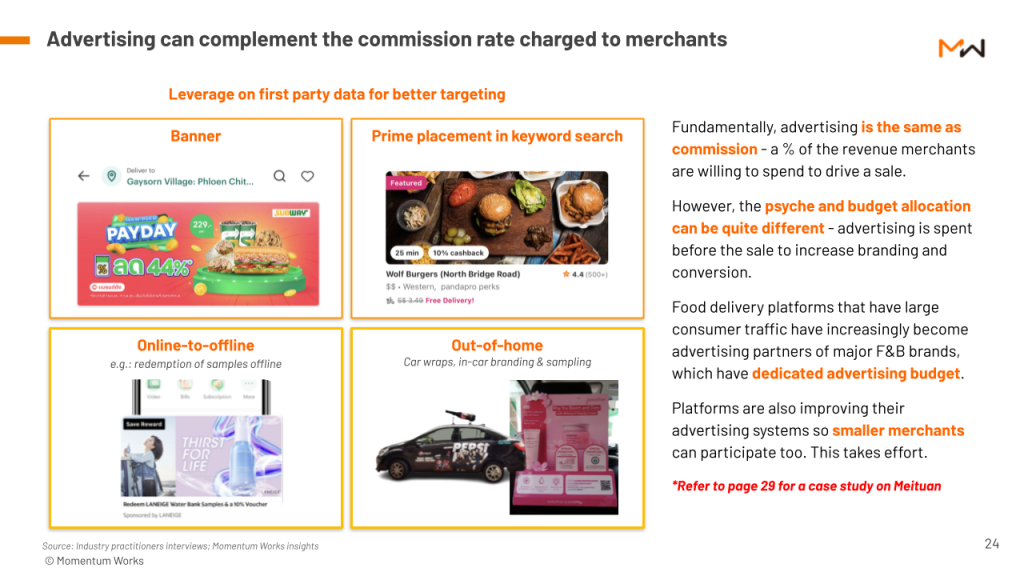

1. Advertising

Food delivery platforms are increasingly tapping into their significant consumer traffic to become advertising partners of major F&B brands. Large food brands with dedicated marketing/advertising budgets are probably larger potential contributors to this revenue stream.

This is not to say that the advertising can’t be open to all merchants who want to increase traffic and sales. Case in point, Meituan leverages its integrated data across multiple customer touchpoints (e.g.: Meituan and Dianping app) to allow (better) targeted ads.

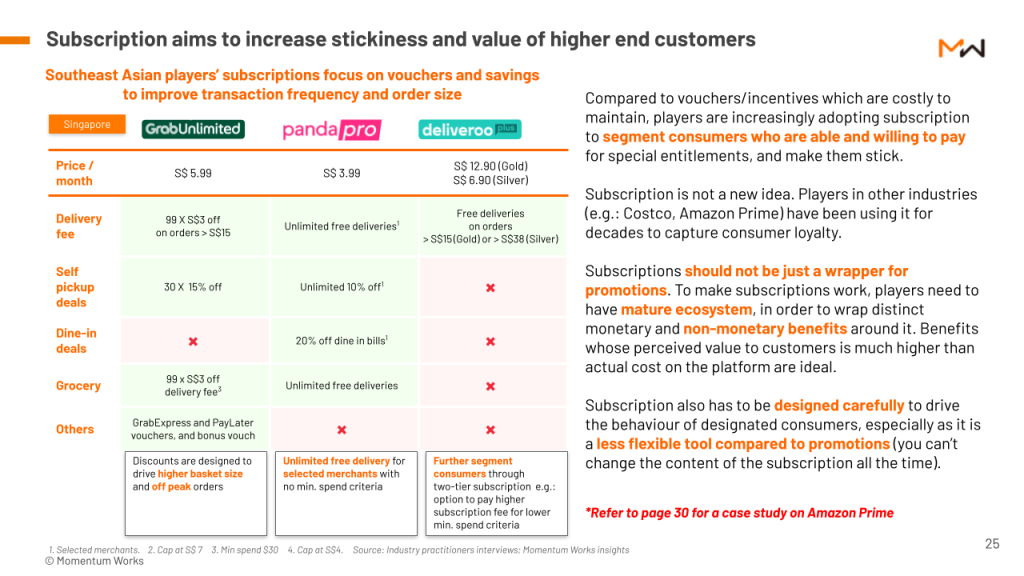

2. Subscription

With various incentive-cutting measures, key platforms are also experimenting with subscription programmes as a tool to improve consumer retention and encourage larger basket size orders.

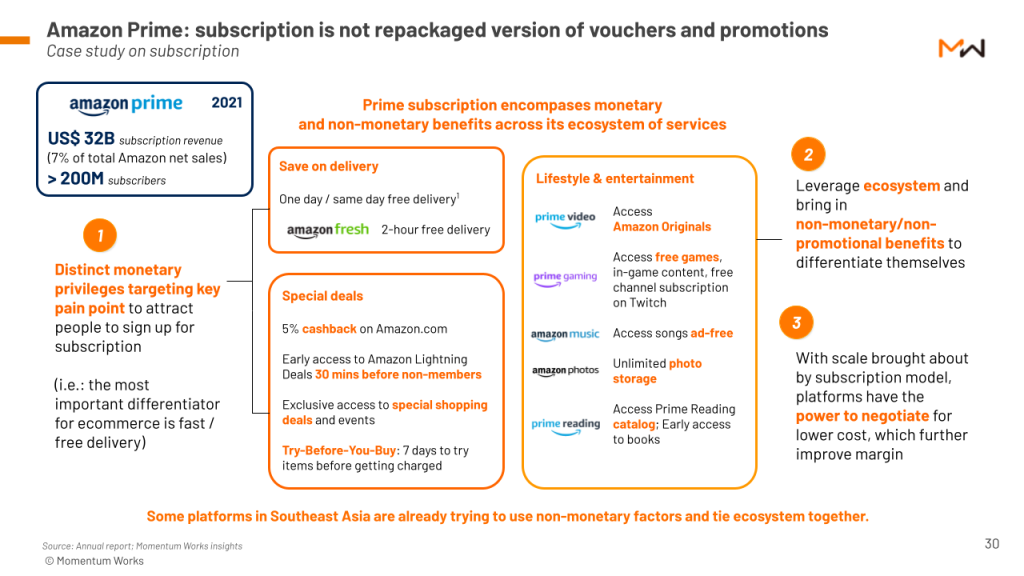

There are however, a few caveats to make subscription work (and subscription should not be just a wrapper for promotions): platforms need to have mature ecosystem in order to wrap distinct monetary and non-monetary benefits around it; Subscription also has to be designed carefully as it is less flexible tool compared to promotions (you can’t change the content of the subscription all the time).

Amazon Prime, launched in 2005, and is arguably one of the most successful subscription programmes in the world with > 200M subscribers, offers some inspiration for practitioners in the region.

3. Restaurant solutions

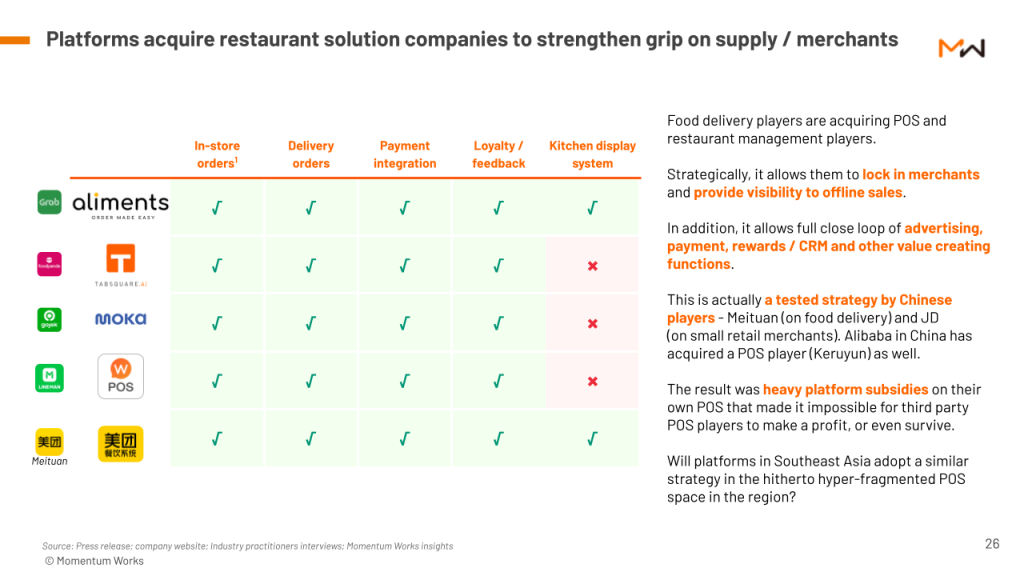

Key food delivery platforms have entered into strategic partnerships or acquisitions with point-of-sales and restaurant management solutions providers in 2022. For example, Grab acquired Aliments, Foodpanda acquired Tabsquare – while GoJek had acquired Moka earlier, and LINEMAN had already been promoting Wongnai’s POS.

These moves are aimed at strengthening merchant retention and enabling platforms to provide more and better-differentiated services to merchants by harnessing online and offline sales data.

More importantly, it creates a full close-loop of advertising, rewards / CRM and other value-creating functions, similar to what Meituan is doing in China.

We think pushing the adoption of these solutions might be a key focus for platforms in 2023.

The bottom line

While the various cost optimisation and revenue expansion strategies across key platforms are similar, the devil, as usual, lies in execution.

Ultimately, profitability in food delivery is attainable with volume, density and operational efficiency.

As most major platforms are publicly listed now, aside from current operating metrics which investors are watching closely, Leadership, People, Organization and Product are critical factors for success (or failure).

More insights

The Food Delivery Platforms in Southeast Asia report is free – and you can obtain your copy here.