Recently, Sweden-based BuyNowPayLater pioneer Klarna announced a new funding round of $800 million. What caught the attention of many was the drastic reduction of valuation: from US$45 billion in 2021 to US$6.7 billion in the latest round.

What is interesting is how they handled this news. Their press release announcing the funding round is a great lesson for many other high flying startups, which might have to announce down rounds soon.

Start with the title, which sets the expectations: “Major financing round” and “worst stock downturn in 50 years”. Of course, how to quantify the “worst stock downturn” is not elaborated here.

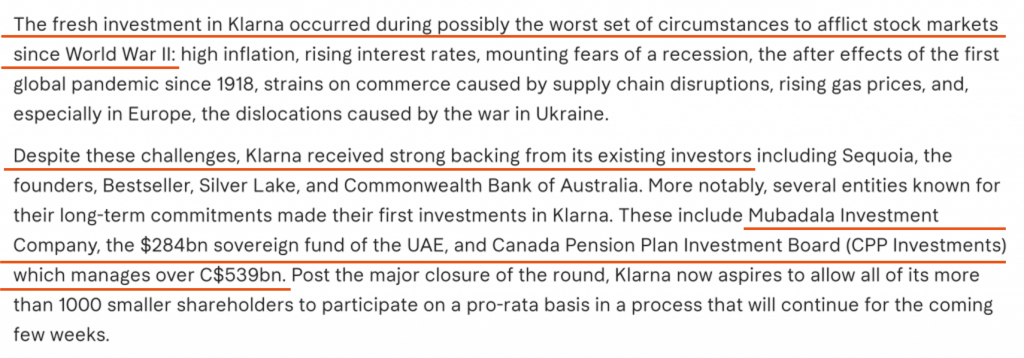

It is interesting how they acknowledge that their valuation has taken a massive hit, but decide to compare against 2018 rather than last year and against public peers. This is their lowest valuation since 2019 when they were valued at $5.5 billion and shift the blame to the macroeconomic environment and changing investor sentiment. They are not entirely wrong, though.

Read: the circumstances are very, very bad. However, long-term investors, including Abu Dhabi and CPPIB, are coming in. They manage a lot of money – though if you think a bit deeper, actually how much money your investors manage should hardly be relevant here.

In our Friends of Momentum Works (FMW) Community, there was an interesting discussion on Klarna’s new financing round and someone from Sweden commented, “Klarna has a lot of cash reserve, but the Swedish finance agency has increased the capital requirements quite heavily lately – something that Klarna is trying to appeal against.”

In May this year, the company announced that it was laying off 10% of its workforce, and there were media reports that Klarna was trying to raise funds at a valuation somewhere around $20-30 billion, lower than their previous $46 billion. However, the Financial Times said that they couldn’t find significant traction.

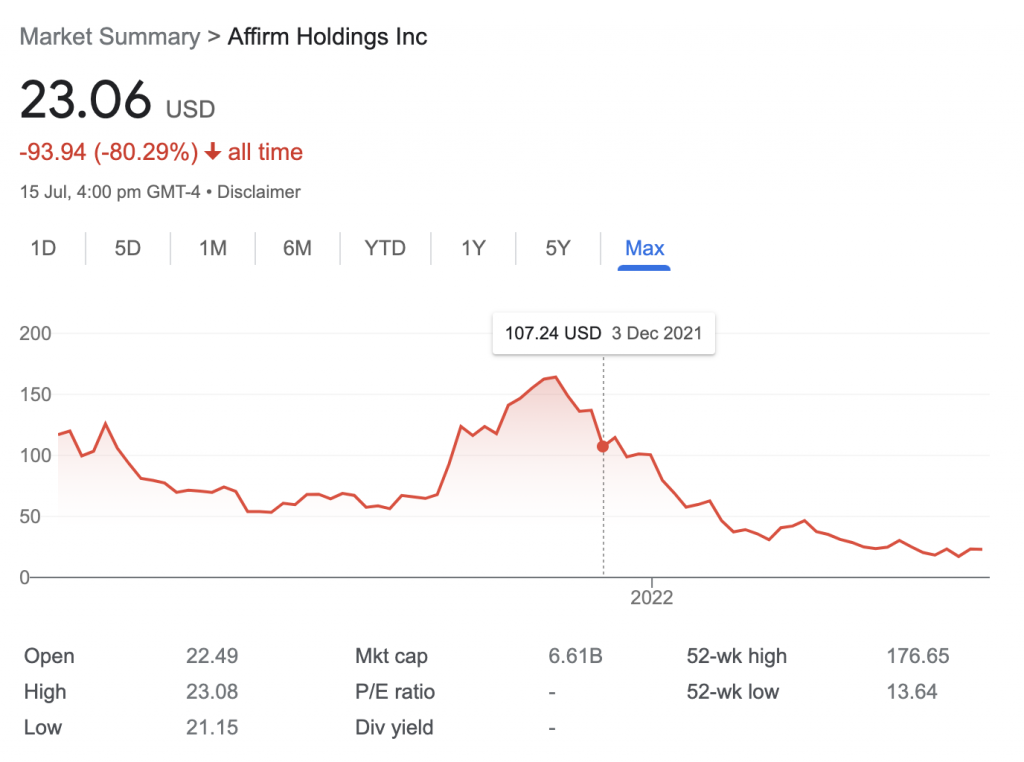

The changing investment landscape has not just affected Klarna but also other BNPL players. Shares of US-listed BNPL player Affirm have fallen by 90% and Australian players such as Zip and Zebit etc. have also taken a big hit. Square, which acquired Australia’s BNPL poster boy AfterPay (and renamed itself Block), has followed the same trajectory.

Klarna also made efforts to reassure investors and the public’s perception of Klarna’s business model. Their CEO, Sebastian Siemiatkowski later tweeted the message as well, reiterating that Klarna was focused on profitability.

There is no doubt that Klarna is one of the better players in the market. They also operate in the best markets (Europe and now United States) where infrastructure is mature, online consumer traffic is fragmented (unlike many parts of Asia where large ecommerce platforms dominate), and consumption power is relatively high. Besides, players like Capital One have already shown how to run consumer credit businesses successfully; while Alibaba/Ant Group have plenty to offer about channelling customer traffic.

As Klarna is sufficiently capitalized and the overall investor sentiment is bearish, the company actually has room to breathe (instead of being forced in a rat race for growth) and work on an efficient, profitable business model.

The cylinders of the growth engine can be reignited after the current period, and they can be very powerful.