Recently we have presented a series of articles on B2B (or some would call “B2B ecommerce” or, in China, “Industrial Internet). From Yuemei Lv of Lightspeed China’s essay to redefine B2B, to a debate on whether Tencent has the gene to succeed in B2B, to sharing of David Wei, ex-CEO of Alibaba, on how to build, and scale B2B companies.

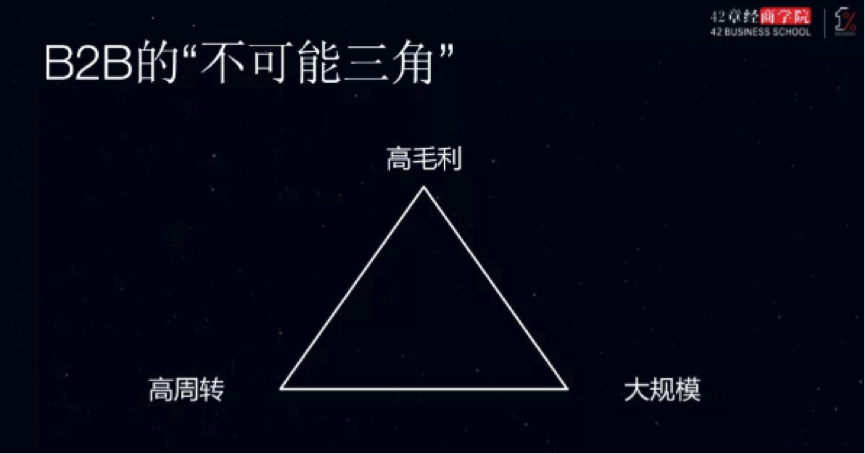

Recently, Dai Wujun, a veteran investor, shared what he thinks is the impossible trinity of B2B ecommerce.

Instead of Free Capital Flow, Fixed Exchange Rate and Sovereign Monetary Policy as you would see in economics, Dai uses Large Volume, Quick Turnover and High Gross Margin.

Companies doing B2B typically can only achieve 2 out of the 3, according to Dai. For example, companies with High Turnover and Large Volume would naturally be in industries where scaling is difficult – and they typically take leverage to maximise their returns.

Choose your client base

One choice companies in B2B space would need to make, especially in their early days, is whether to focus on big or small clients.

Dai says for big customers, naturally you would fall into the High Margin and Low Turnover. Reasons are big customers typically have long payment cycles, and high requirements on your inventory – as a result your turnover is low, and the margin is required to cover the costs and risks.

For those focusing on small customers, Low Margin and High Turnover are the norm. Small customers are price sensitive, but they pay fast. The challenge is they are often not standardised, resulting in difficulty in Scaling. When you have thousands of SKUs and thousands of customers – how to manage your IT system and inventory/assortment is a big challenge.

Many companies in this bucket find it hard to raise VC money in early stages, because of low margin and often low customer satisfaction – because of the benefits of digitalisation will take a long time to realise.

However, those who manage to survive would see their cashflow improve drastically with their volume. Sysco, US Foods and PFG are three typical examples.

How to pick your investments

For investors, Dai suggests a few general principles to look at companies in these buckets.

For those focusing on big companies: look whether they possess strong and continuous fundraising capabilities, deep understanding about macro economy and the industry, as well a good pace on both fundraising and operational scaling.

For those focusing on small customers, the key is IT and customer acquisition. Another key focus is how do they manage key cash and turnover metrics (definitely not cohort which people often use in 2C business models).

Why not using cohort

According to Dai, because B2B is significantly different from B2C, and includes seasonality and business cycle. Another key consideration is that the achievements of B2B is often discrete rather than continuous – so you would see some metrics performing badly, but over night because they achieved critical mass to replace existing channel, turning sharply upwards.

Another metric, according to Dai, that investors need to be careful about is unit economics. Companies which are on the growth trajectory typically employ very bad unit economics for growth – and suddenly turning profitable once they achieve critical mass. It takes more effort to look at the ‘potential’ unit economics rather than the current one.

All make sense?

It is worth noting that what Dai proposes is a general principle that does not necessarily apply to all B2B sectors. B2B is complex and in many sectors not transparent at all – so oddities do exist.