Sea Limited is a fast and rising internet and mobile platform company, which primarily operates through 3 main segments – digital entertainment through Garena, E-commerce through Shopee, and digital financial services through the SeaMoney.

Formally founded in 2009 as a purely digital entertainment company via Garena, it has diversified its business offerings and IPO-ed in NYSE in 2017, successfully raising $1.2Bn. Since then (or rather, after more than a year), it has grown at an exponential rate, with its digital entertainment being a highly profitable segment of their business model, and its E-commerce segment, Shopee, rapidly rising in scale and further widening its lead over peers in number of downloads and active user count among Southeast Asia’s biggest shopping apps.

This has catapulted Sea’s share price from an initial share price of $16.20 to $114.46 (Last Trading Price 4.00 pm EDT, 02 July 2020).

Source: Yahoo Finance

Source: Yahoo Finance

However, when we look deeper into the financial metrics of Sea Limited, we start to see that the circumstances are not as rosy as depicted by investors.

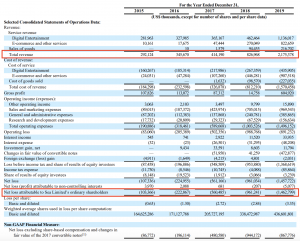

Despite its net sales increasing impressively over the past 5 years, Sea has never been profitable, with both its EBITDA and net income being in the red consistently in the past 5 years. More interestingly, its net income loss has been widening, with its being ($103.4M) in 2015 to ($1,462.8M) in 2019.

This seems counterintuitive, and begs the question, on why a company’s share price is consistently increasing while its profitability, basically a testament to a company’s ability to make money, is on the decline.

Source: Sea Financial Statement

A company’s share price is basically a reflection of investors’ confidence and represents the intrinsic equity value of the company. Despite Sea’s unprofitability, investors are still confident on Sea’s ability to turn a profit in the near future due to these few reasons, among others:

1. Shopee as a main driver of profitability

Many believe Shopee to be the Amazon of Southeast Asia, despite the fact that Shopee’s business model is miles away from that of Amazon.

However, one thing is similar, both had a stellar performance in Q1 2020.

Source: Amazon Quarterly Results (Left) & Sea Limited Quarterly Results (Right)

Source: Amazon Quarterly Results (Left) & Sea Limited Quarterly Results (Right)

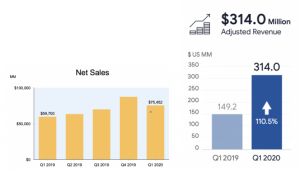

It is #1 in average monthly active users (MAUs) and total time in-app on android in both Southeast Asia and Taiwan and is #1 in downloads in Southeast Asia. In addition, adjusted revenue also experienced a significant gain of 110.5%, jumping from $149.2M in Q1 2019 to $314.0M in Q1 2020.

It is clear that despite Shopee being unprofitable, it is able to ride big secular tailwinds that are only being accelerated by Coronavirus, and the common sentiment is that Shopee will continue to be the leading E-commerce company in Southeast Asia.

Having said that, being popular among users does not guarantee profitability. Despite popularity being a key driver towards eventual profits, an equally important driver would be Shopee’s ability to effectively monetize its services. Shopee must be careful in monetizing its services without compromising on its popularity among merchants and customers, a huge challenge that many E-Commerce companies face.

To become the leading E-commerce website within a timespan of 4 years is no easy feat, and much of its growth has been accelerated by effective marketing campaigns such as the Cristiano Ronaldo commercial. (And of course, Lazada and Tokopedia helped it educate the market to a certain extent before its entry).

This is reflective in total sales and marketing expenses, jumping by 37.5% from $705,015M in 2018 to $969.543M in 2019. As such, we believe keeping a watchful lookout on Shopee’s key unit economic indicators such as customer acquisition cost and profit per customer would be pertinent in determining if Shopee would be able to achieve profitability in the (near) future.

2. Expected Synergies Among their 3 Businesses

A key differentiating factor Sea Limited possesses is the existence of strong potential synergies among their 3 businesses, whereby the growth of one platform helps to drive and accelerate that of the others, leading to a gain in the breadth, depth, and interconnectedness of their overall ecosystem.

For example, as an increasing number of their Garena players and Shopee customers, complete transactions using their SeaMoney platform, growth in both the digital entertainment and e-commerce platform will accelerate their digital financial services platform.

This is further supported by exciting news such as Sea being successfully shortlisted by MAS as a potential applicant for a digital banking license, and 40% of Shopee’s gross orders in Indonesia being paid using SeaMoney in April 2020.

Shopee’s journey is in a way more similar to that of Alibaba, which went from ecommerce (Taobao) to payment (Alipay) to financial services (Ant Financial).

On one hand, such synergistic relationships bring about huge potential for growth and success. On the other hand, this also brings a huge risk where a decline in user activity in one platform may adversely affect other platforms.

For example, a disruption to the Shopee platform may likewise cause a negative impact on Sea’s e-wallet transaction volume. This highlights the importance of balancing the interest of all participants in Sea’s ecosystem and ensuring that this ecosystem remains appealing to all participants.

As an investor, one must be aware of such a downside to having an ecosystem and take that into account when deciding on whether to invest into Sea.

3. Highly profitable digital entertainment segment

The digital entertainment segment has been a significant driver of growth for Sea, showing a strong front on both revenues and EBITDA. For revenue, digital entertainment experienced a 30.3% gain from $393.3M in Q1 2019 to $512.4M in Q1 2020, while for EBITDA, a similar gain of 32.3% was seen from $225.8M in Q1 2019 to $298.4M in Q1 2020.

In addition, the unit economics of digital entertainment is also performing well, with EBITDA margins sitting at 58.2% in Q1 2020.

Such numbers are astounding as it shows that there is not only a demand for digital entertainment by Garena, but it also demonstrates that it is a profitable business segment. This significantly boosts investor confidence in Sea as they know that if Shopee is eventually unable to turn profitable, Sea still has Garena, a highly profitable business.

Being backed by Tencent (24.03% shares) also places Garena in an excellent position to remain a leader of the Southeast Asia digital entertainment platform space.

Initial criticism of Garena’s business model was that due to its heavy reliance on licenses with third-party game developers, this places huge risk on the reliability of revenue generation as it would be highly dependent on these third-party game developers. Though a valid point, this has been effectively quelled through the establishment of a mutually beneficial relationship with Tencent, a leading video game publisher worldwide.

Closing Words

The equity market is highly driven by market sentiments, and it is clear that many believe that Sea Limited will perform even better in the future. Its competitors are weaker and less localized, giving it a huge advantage for further growth even though its systems are far from perfect.

However, given the inherently volatile nature of expectations as opposed to concrete data, it is important to look at factors objectively and form an unbiased opinion.

No one knows what the future holds for Sea Limited, but at least for now, it looks quite optimistic.

Read more articles: Why did SEA employees sell their shares?