On 30 November 2022, Jianggan Li, CEO of Momentum Works, was invited by Huxiu, the Chinese media platform, to join their “Chuhai Periscope” event where he shared his thoughts on “Market trends in Southeast Asia and growth potential”.

“Chuhai Periscope” (出海潜望镜) by Huxiu is a series of sharings by industry practitioners on their strategies and insights, especially for Chinese tech companies going overseas.

Jianggan shared his perspectives on the Southeast Asian market environment and future prospects with investors and entrepreneurs at the event, which we have divided into two parts.

In the first part, we outlined the macro and investment trends in Southeast Asia and the financial services industry.

In this second part, we outline the key points Jianggan shared on the ecommerce and consumer industry, the opportunities and challenges and his answers to some of the participants’ questions.

4. Ecommerce and consumer industry

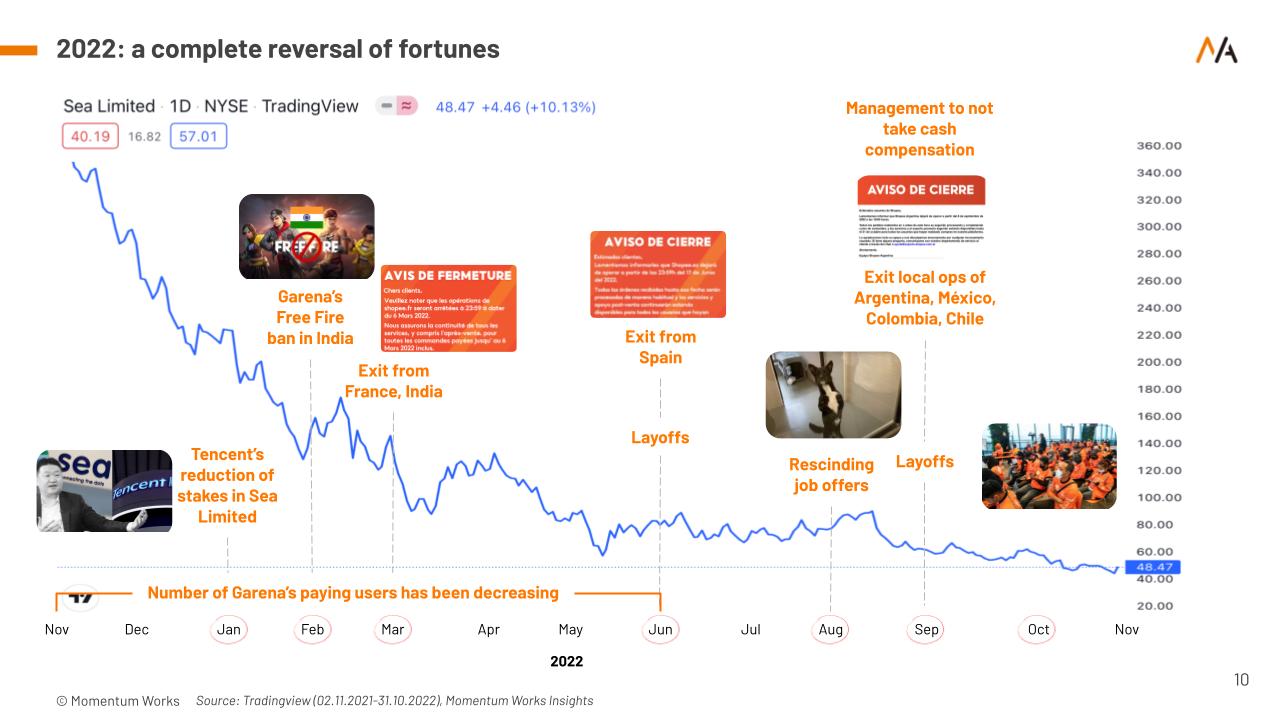

In our last event, Off the Record: Shopee’s turbulent 2022, we spoke about the different scenarios Shopee faced in 2021 and 2022. (Read recap here)

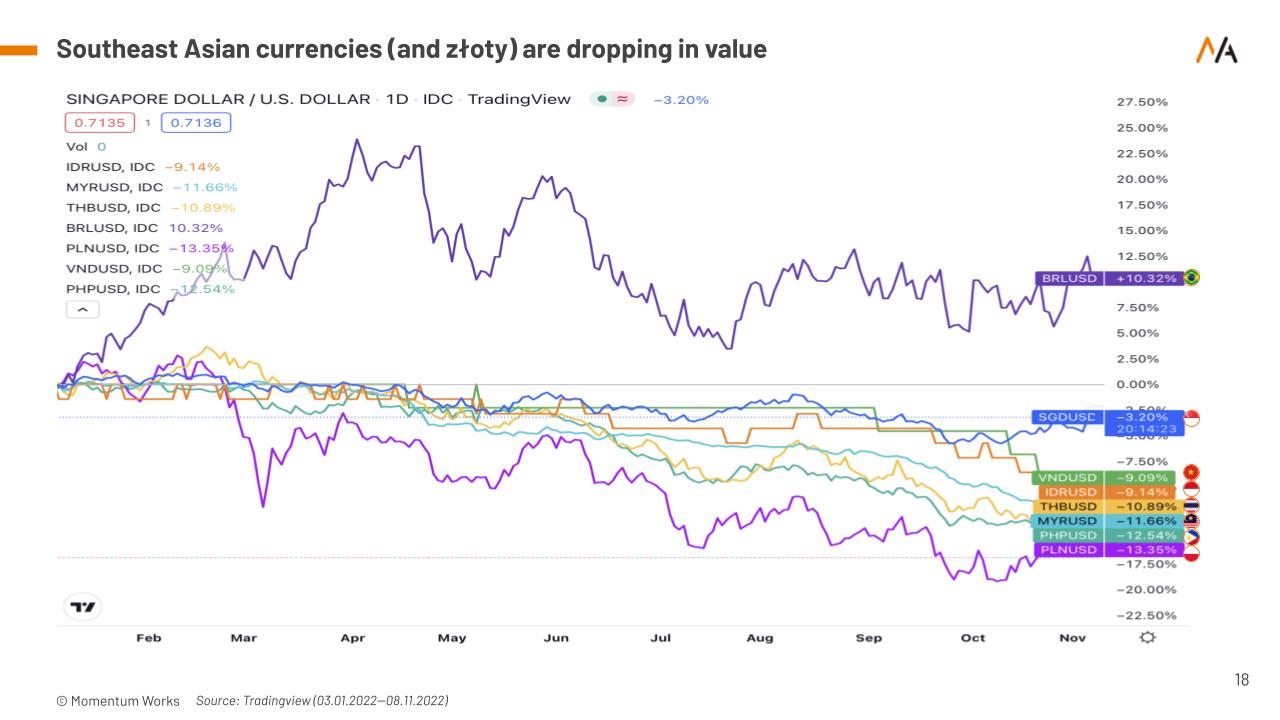

Over 2022, many Southeast Asian currencies have depreciated against the strengthening USD.

Fluctuations in oil prices have affected the cost of living, consumers’ purchasing behaviour, as well as the cost of e-commerce fulfilment. We are also seeing an increased recovery of offline consumption, and many people are back at shopping malls.

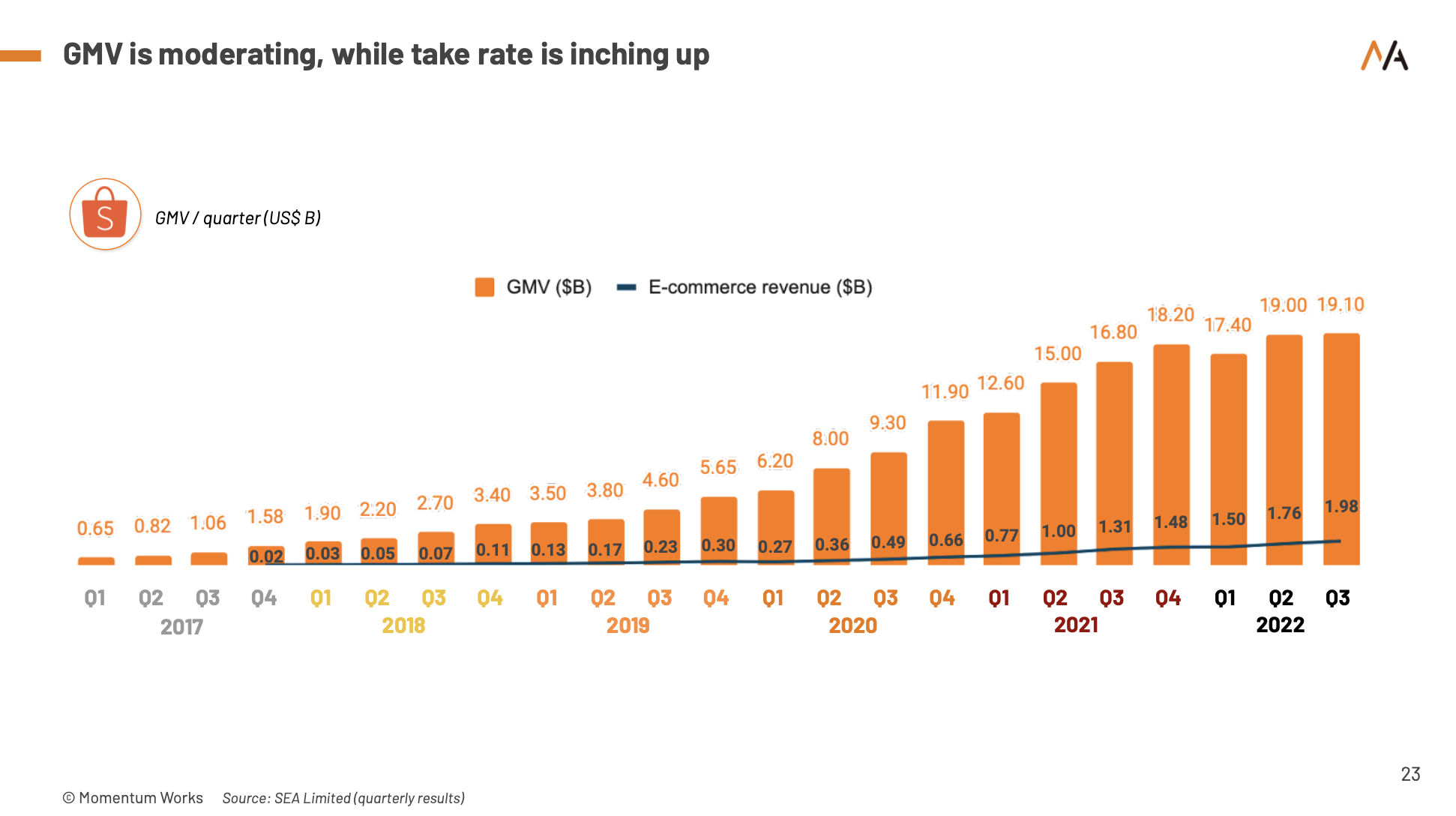

Shopee’s GMV and revenue for the past few years also show that growth is somewhat weak this year.

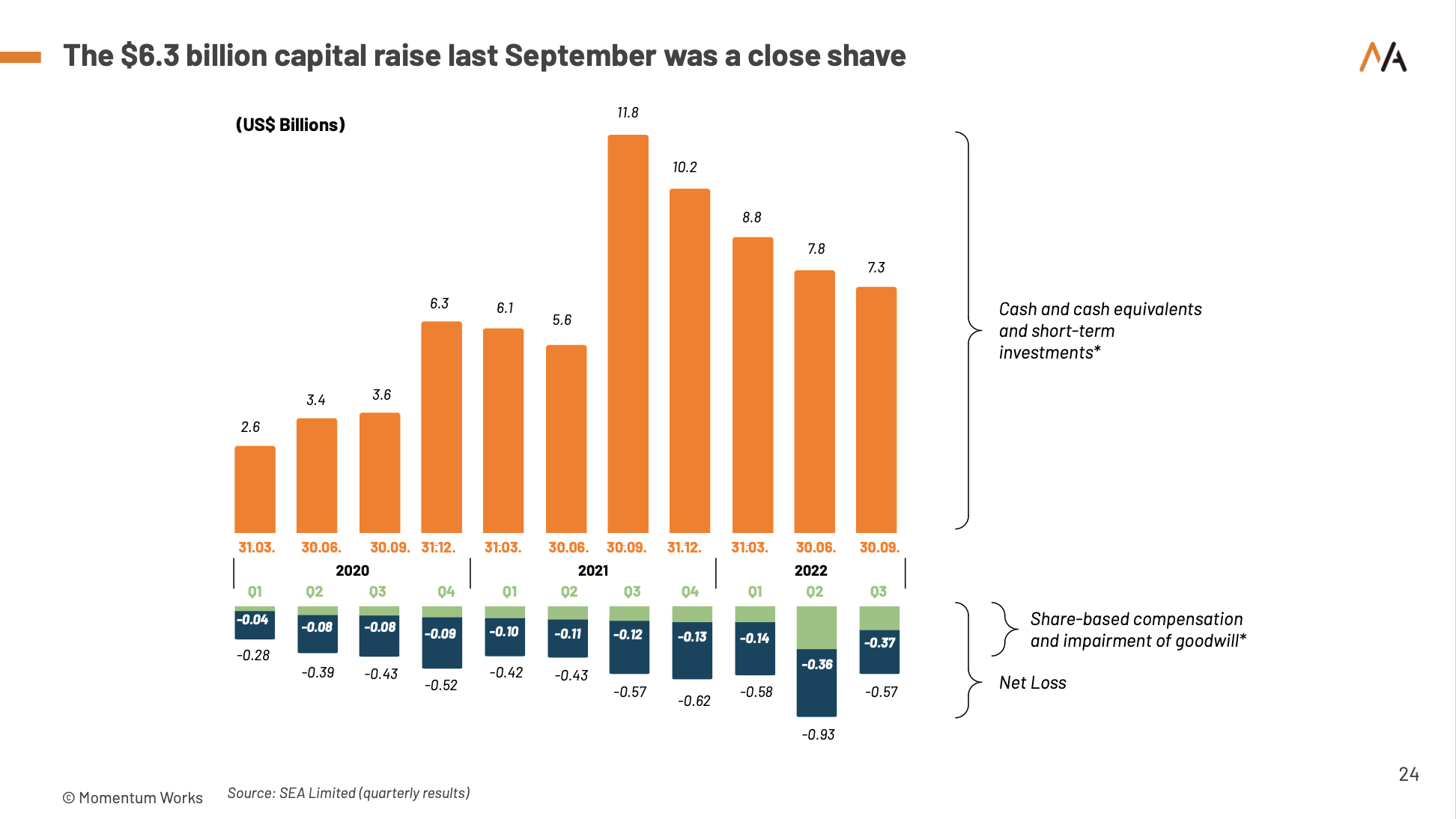

No one expected this year’s market environment, and now it looks like the $6+ billion raised by SEA Group last year was very timely. They currently have $7.3 billion in cash and cash equivalents.

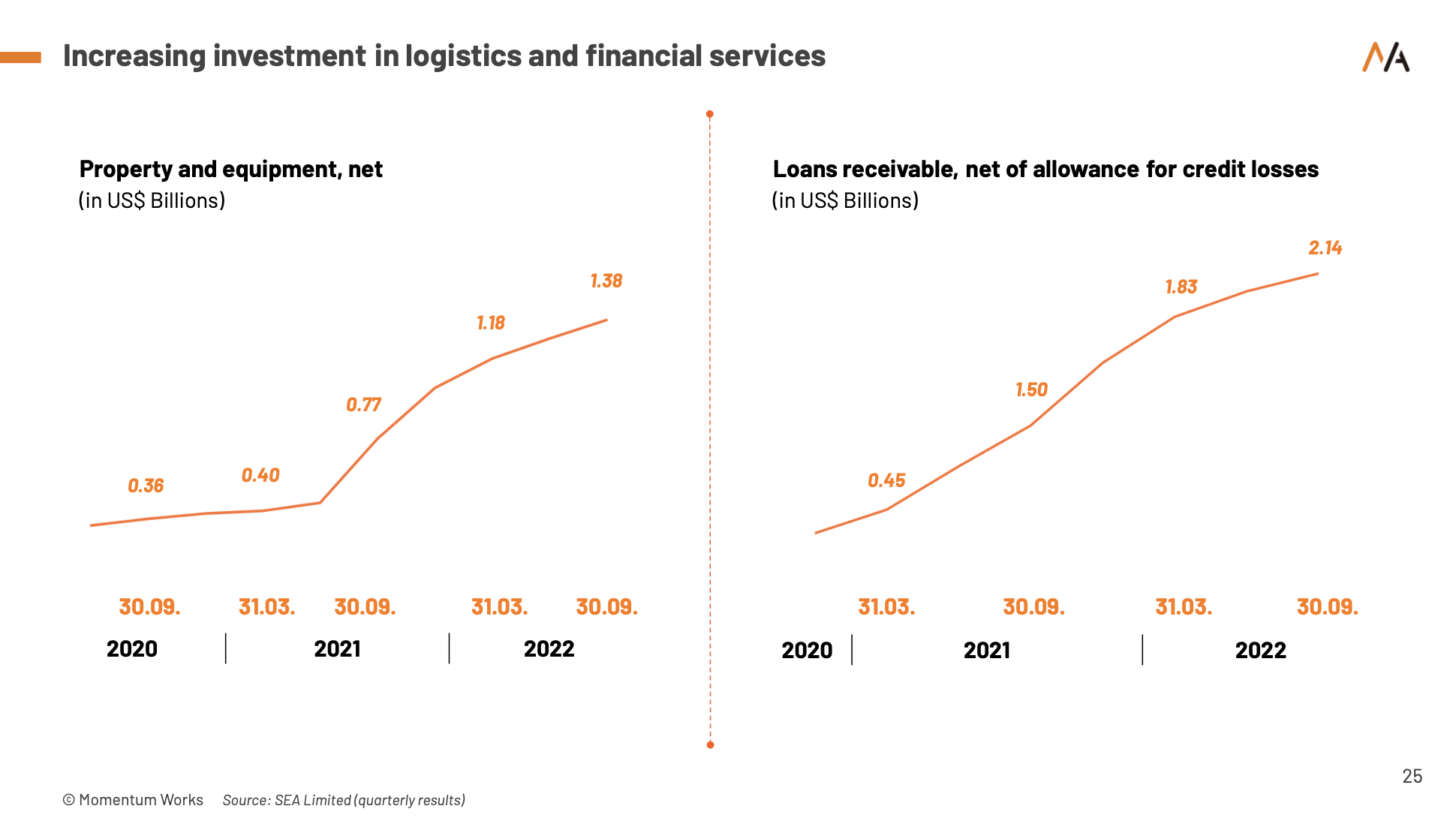

Shopee’s investments in logistics and financial services are very beneficial as well. (Read what we shared about Shopee’s strategy)

Let’s take a look at Lazada. To understand what they have done this year, one can look at the four key men behind the organization. And the last of the original Rocket Internet founders is finally leaving.

Tracing the development of Lazada, one can see that there are problems with organizational coordination (especially the synergy with Alibaba) and company culture. These are not easy to solve. It is a common challenge that most companies going abroad face.

Lazada has invested in Dana and Touch ‘n Go digital wallets in Indonesia and Malaysia – a positive signal considering its strong control over payments. Earlier this year, someone said that Lazada might be expanding into Europe, but there seems to be no concrete action.

As for TikTok, it expanded its ecommerce business to six countries in Southeast Asia this year. TikTop Shop, however, still faces the problem of cashing in on traffic. At present, the app’s homepage has an added shopping entrance, which is different from Douyin (TikTok’s Chinese counterpart). It remains to be seen how it improves the conversion rate and whether other operations will differ from Douyin.

When analyzing and comparing these platforms, one needs to see their positions in the company’s bigger group – what role they play, how much attention and resources they can receive, and if the organization’s processes and coordination are smooth. These are practical questions for large domestic manufacturers when they land overseas.

5. Opportunities and Challenges

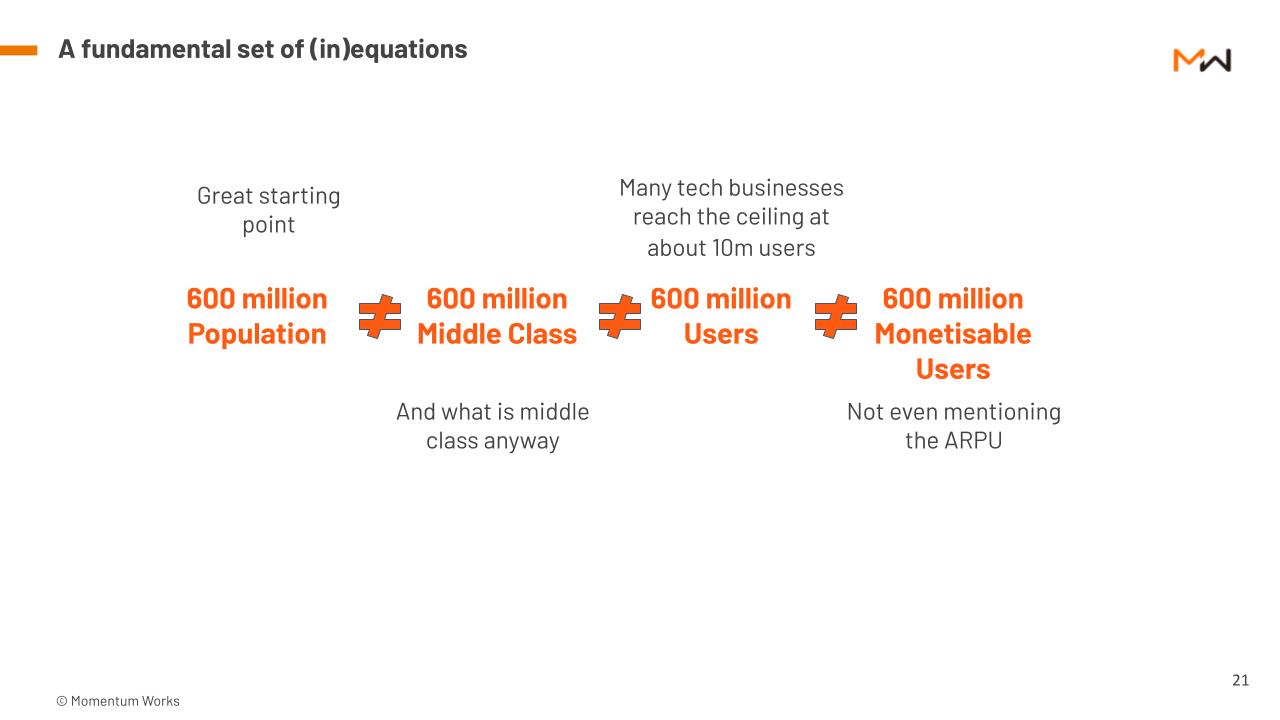

What is the real meaning of data? A simple example is this core equation. It takes work to establish an appropriate expectation and perception of the market.

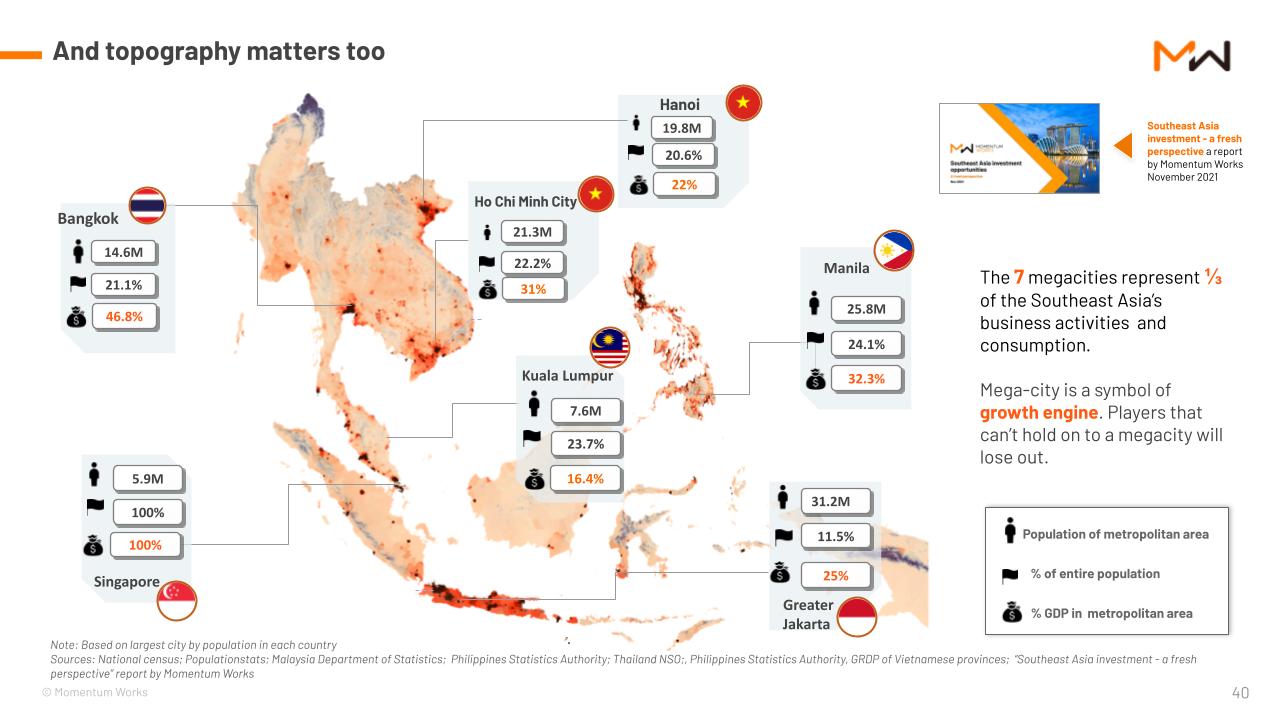

A large population in Southeast Asian countries (or a substantial consumption power) is concentrated in megacities. Under this macro environment, if it is a pure internet model, it may not make much sense to deploy in lower tier markets. From the perspective of consumption, we can gain inspiration from how Chinese companies open offline channels to sell traditional consumer goods.

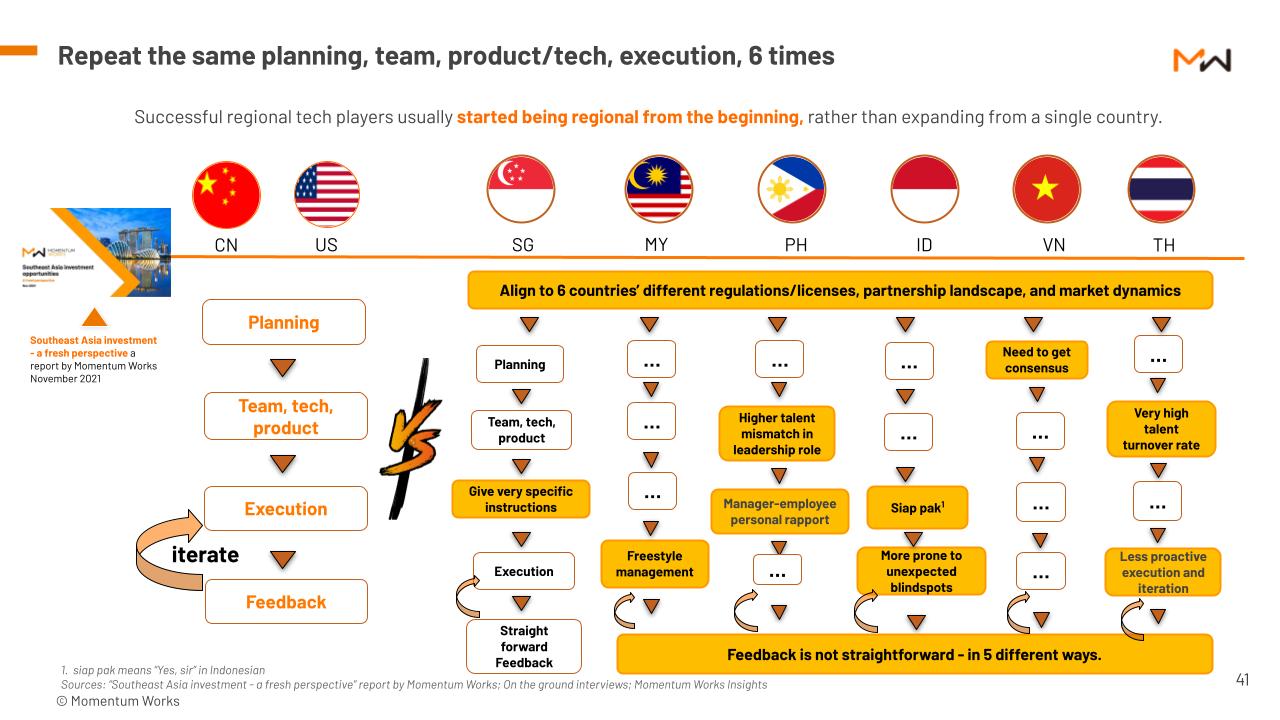

Unlike the large single market in China or US, management in Southeast Asia needs to be differentiated and adapted to the local context. The six countries may need to have six different teams.

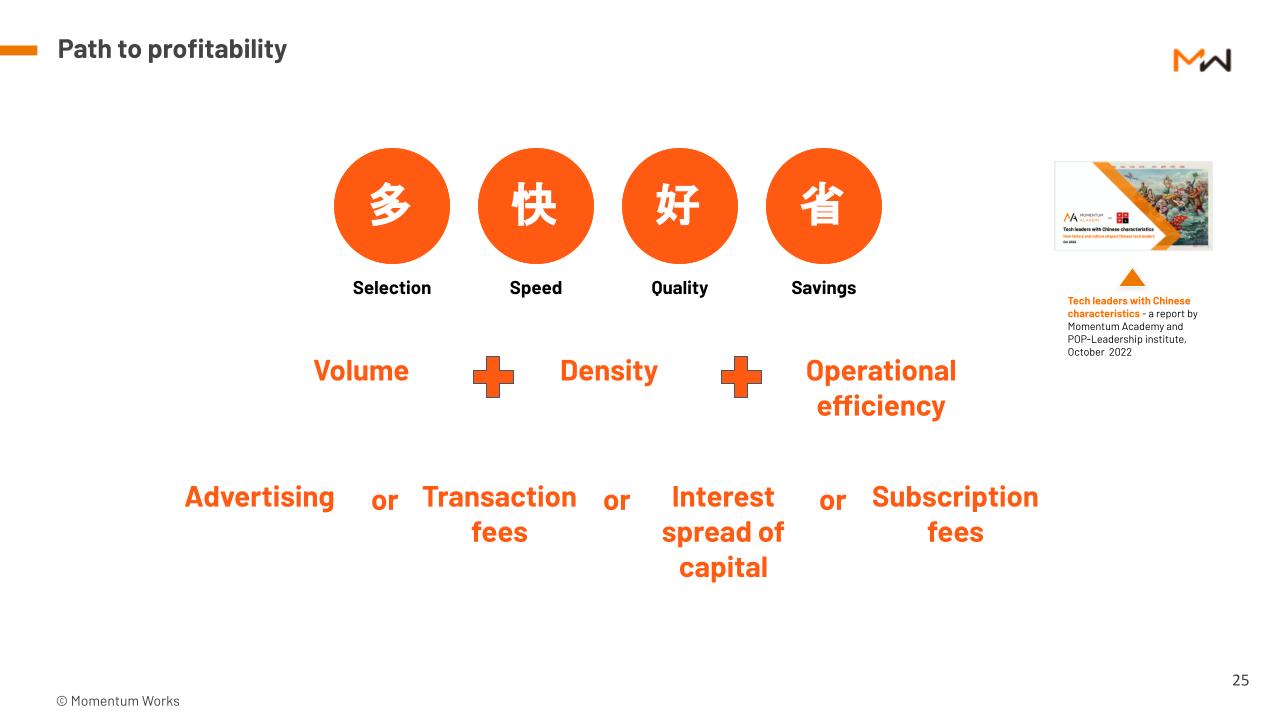

The “Duo Kuai Hao Sheng” theory applies to most business models. If companies in Southeast Asia want to achieve the same level as China, the requirement for efficiency may be a little higher because the market infrastructure is insufficient.

Q&A

1. Will Lazada split up and go public? Can you share the story of Shopee overtaking Lazada in 2019?

In the current capital environment, it is unlikely. From the perspective of Alibaba Group – will it be better for Lazada’s long-term survival to get financing after going public? It could also have an impact on Lazada executives’ motivation and constraints – will the decision be very different if there is an independent board of directors and external investors to monitor? With Lazada’s money burning level, Alibaba should still be able to hold it up. Of course, it ultimately depends on Alibaba.

Between 2014 to 2015, Shopee started as a C2C platform. From 2015 to 2016, the change of leadership in Taiwan made it hard for Taobao to continue, creating an opportunity for Shopee. Garena, Shopee’s cousin in game development, has been operating in Taiwan, so Shopee utilized their understanding of local operations and consumer preferences to make Taiwan its first successful market.

In 2016, Shopee entered Indonesia. In the first few years of COVID-19, it insisted on doing free delivery, shopping festivals, and influencer advertising, slowly growing its volume. In 2019, the capital market began to pay attention to Shopee, and SEA’s share price also increased. At the same time, Lazada experienced some leadership changes and adjustments, which hurt the organization, and Shopee slowly caught up.

2. Why is JD.com shutting down its Indonesian business next year?

In 2017, JD’s investment deal with an Indonesian e-commerce platform was cut off by Alibaba, resulting in a change in JD’s strategy in Southeast Asia. The joint venture between JD and Central in Thailand was quickly negotiated – and may have been influenced by this cut-off. However, the process was not smooth in terms of coordination. Central is a traditional retail group, and JD’s Indonesian partner is a capital company, so the partnership was not compatible in terms of pace and purpose. The two markets are far from profitable, and both require continuous investment. Traditional companies in Southeast Asia do not quite understand the lack of profit.

3. You mentioned that the Thai regulatory system is very efficient. Can you explain in detail?

When you take a look at the overall financial environment in Thailand – cryptocurrency has developed a lot, and financial regulators are highly efficient. Our friends who have obtained licenses in Thailand have dealt with regulators and noted that their professionalism and ethics are unparalleled in Southeast Asia. PromptPay, the real-time clearing system mentioned earlier, coordinates well with banks and regulations.

4. Recently, investments in Singapore are very popular, and institutions and family offices are growing rapidly. Will this trend have any impact on China’s financing environment?

There will not be any apparent impact on China’s financing environment. There were many difficulties in investing and financing in China due to COVID-19, and many people were willing to go abroad to identify opportunities. But if China opens in the future, there may be fewer people. From Chinese investors’ perspective, the market here is very small (with the benefit that competition is not as fierce), and it is not sure how many people will stay in the long term.

5. Some mentioned that Web3 in Singapore is hot. There are some views that although a lot of capital is pouring into Singapore, local startups and the Web3 industry is not particularly mature. What is your opinion?

We have a team that has been working on Web3 at the application level. It is very early stage, so it will take a long time before it is applied. The Singapore government’s protection of local consumers and the regulatory attitude towards cryptocurrency are much more conservative than in other places. You can read about the recent Temasek investment in FTX, and the Singapore parliament’s debate which had many interesting points.

6. Why do many large companies set up branches in Singapore? What are the aspects of Singapore that they are interested in? What are the challenges of integrating the Singapore team with the China team?

Singapore is neutral in China–US relations and other geopolitical issues. The location is convenient for expanding to other markets, the living environment is very suitable, and the climate is good – these are influential factors.

The first problem is the company’s culture and management style – talent and executives here are accustomed to the Western corporate culture. Second is the language problem – locals are not able to use Chinese as their working language, so communication and culture need to be bridged.

7. Is there an opportunity for a D2C model in Southeast Asia?

Many Chinese brands are looking at opportunities in Southeast Asia, and there are opportunities in the market for consumer products. But offline channels are more important than online, and the volume of D2C online may be small. In the short term, there is the bonus of TikTok Shop for people to sell their goods. However, building a brand is a long-term process, and there is a lot of offline work to do.

8. What will be the impact of Indonesia’s capital relocation?

It is still unknown what will be the political ecology of Indonesia after the 2024 elections. Who will be in position after the elections? Will Joko have the influence he has now? Will he be enthusiastic in promoting the capital relocation? These factors may affect the scale and process of the relocation. From a business point of view, it should not have much impact.