India, with a population of more than 1.3 billion, was often regarded as “the next China” as far as the tech opportunities were concerned. Compared to other emerging markets, the investment race in India started much earlier and intensified much faster. Everyone was plagued by the worry – “what if India becomes the next China but you miss the bus?”

This explains why capital of different origins have been battling it out, not willing to budge on whatever they have seized on, most of the time at least. At the same time, entrepreneurs in India are having one roller coaster ride after another, driven by capital, competition, and the insatiable pursuit of growth and valuation.

In May 2018, Walmart, which had been trying for years to enter India, and which had been anxiously watching Amazon’s ascent, finally took the leap to acquire 77% of Flipkart for US$16 billion (yes, overpaid, but so what?). Softbank kept pumping in more money into its portfolio in the market, including OYO, which made rapid and aggressive push into China. Naspers and Tencent just doubled down on Swiggy.

Also in 2018, China’s cross-border ecommerce players, led by Club Factory & SheIn, continued to expand into India, leveraging their competitive pricing and SKU range. Mobile content platforms continued to struggle to monetize, while giants including Netflix and Times of India invested heavily in their own content.

What will happen to this market in the coming 2019? Here are the predictions of Momentum Works:

-

Profit is still elusive for ALL ecommerce platforms

India is arguably the most invested market for ecommerce in the world. Over the last couple of years, Walmart, Amazon, Softbank, and Alibaba have all placed big bets here. In addition, tycoon Mukesh Ambani (who is behind Jio) also launched his own ecommerce business this year. Cross-border ecommerce companies from China, seeking topline and valuation growth, will continue to invest in India unless they are stung by the regulators. The competition will not recede in 2019.

Making a profit is still a long way off for most of the players – platforms or sellers.

Low basket size, high logistics cost, heavy spending on discounts and advertisements with low sales conversion rate, and high commissions are some of the reasons. With the competition intensifying, ecommerce players will continue to burn cash in order to not lose market share.

-

Social commerce continues to attract investment, not gross profitability

This year, the IPO of Pinduoduo in China made many investors re-discover social commerce and their role in a world where customer acquisition cost keeps rising.

India is the world’s largest market for WhatsApp – and people are very social. So naturally how to explore that for ecommerce growth is high on the agenda.

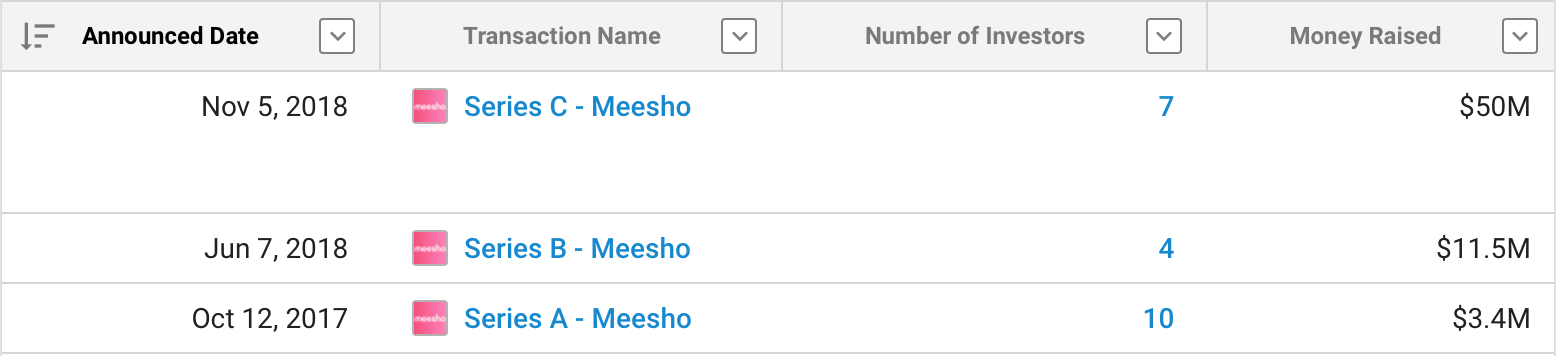

Meesho, Shop101, and Wooplr have been leading the pack. Meesho raised three rounds in the span of almost a year with the recent one reaching US$50 million. Wooplr, an older player who used to compare themselves to Mogujie in China (except the latter was heavily bruised by Taobao later on), is rejuvenating.

A few Chinese players also joined the game, although most of them are operating in stealth mode (i.e. keeping themselves away from any media or industry attention).

We expect this trend to continue in 2019. Alas, WhatsApp and Facebook are very different from WeChat, as far as ecommerce sharing and conversion is concerned; social commerce faces the same issues of marketing and fulfilment that bug any ecommerce in India.

Therefore, after an initial phase of rapid growth, how they maintain steam as they scale up is a test of the team’s capabilities and their strategy.

-

Delhivery continues to lead delivery space, though competition continues to intensify in the last mile space

With the rise of ecommerce, logistics companies have also developed rapidly. Recently, India’s largest ecommerce logistics startup, Delhivery, announced its FY 2018 results and reported a revenue US$15.33 billion, an increase of 42% compared to last year. Softbank plans to invest $450 million in it, which might have led Delhivery to postpone its IPO plans.

The logistics sector is vast, and although Delhivery claims to have covered more than 1,700 cities, with more than 4,000 trucks operating daily, and have processed more than 300 million orders, it needs to be taken with a truckload of salt.

Indian social media forums reflect poor ratings of Delhivery with negative feedback involving complaints about slow delivery times and poor service among many others.

There are lots of players in the logistics field. Delhivery will certainly continue to lead even just because of its size and reach. That said, precisely because of its diverse business areas, in many fields including last mile there are players who have been doing a better job. Many of these players are not known to investors (but to their clients for sure).

Ultimately, the whole tech-enabled logistics sector is still in its infancy with a lot of opportunities to be exploited.

-

Club Factory officially gets stung by the government; more Chinese ecommerce players enter during the first half of the year

After Club Factory tested the waters of emerging markets such as Southeast Asia and the Middle East this year, it zeroed in on India as its focus market. It then introduced free shipping, no minimum order size, and other features to ramp up its growth. At one point it was shipping more orders than Alibaba-backed Paytm Mall.

At present, China’s cross-border ecommerce players that invest heavily in India include Club Factory, Shein, Global Easy, Ali Express, etc. Chinese fashion, beauty and lifestyle platforms are popular among Indian consumers because of wide product range, pocket-friendly prices, and stylish trends. It is expected that more Chinese players will enter in the first half of 2019.

But the cross-border ecommerce model is still in the gray zone, because the Indian government has banned foreign companies from engaging in integrated retail business in India in order to “protect local SMEs” (that is why Walmart has been lobbying for many years and has been unable to enter India).

Nowadays, Amazon and China’s cross-border ecommerce companies generally adopt the method of using third-party related companies. How the government perceives the legality of this setup may change. There are signs of the government further clamping down with a recent announcement that bars platforms like Amazon and Flipkart from selling products in which they have an equity stake.

There are of course other loopholes that are not covered in the latest requirements. As general elections are approaching, and especially if and when the tide is not looking good for the incumbent, we expect more curbs on these practices by foreign ecommerce players.

In this regard, we feel that the potential challenges faced by Chinese players are greater than that by Walmart and Amazon. After all, the latter two have developed a vast amount of local infrastructure, employed a large pool of locals, and have also given platforms to local sellers.

-

WhatsApp payment fails to take off

Two years after initial discussions with the Indian government, WhatsApp tested its payment function in small areas in India in February this year. It was expected to be officially launched in June, but it encountered heavy resistance. In terms of regulation, the Reserve Bank of India (RBI) requires payment companies to store user data in India and has asked WhatsApp to provide a compliance schedule. Additionally, its competitor Paytm expressed that Facebook is developing the payment market unfairly.

As mentioned above, WhatsApp has a strong user base in India, and it has the huge potential to be the de facto system for trade, as many merchants contact their suppliers on WhatsaApp anyway.

However, existing obstacles will continue to hold it back in 2019 – the row about the fake news being spread over WhatsApp is not helping its case, especially when elections are coming close.

And the ongoing delays also give regulators, banks and competitors more time and space to cope. India’s financial regulation is very, very smart and cannot be underestimated.

-

Investors are still struggling to identify good early stage companies; many VCs go into seed investment/incubation

Obviously opportunities have been seized by existing companies, while early stage VCs now need to work much harder to find gems in hundreds of startups whose business models are not that conventional anymore.

Tough for many – even just the sheer work of analysing all these business models properly. The fear of missing out is almost always at play as well.

To solve this issue, we expect more early stage VCs to move even earlier, building incubators and even ventures, following what Kalaari has done with KStart.

-

Seeking new growth, major smartphone manufacturers go into venture capital

India is the second largest smartphone consumer market in the world. In FY18, Indian consumers spent more than US$ 6.8 billion on the purchase of Xiaomi, OPPO, Vivo and Huawei phones. Chinese brands account for around 50% of smartphone sales with Xiaomi holding 27% market share.

However, smartphone sales in India have shown signs of slowing in 2018. According to reports by the Passage Group, Lenovo, which was once ranked second, has withdrawn from the market, and OPPO is also slowing down.

This trend will inevitably continue in 2019. In addition to building factories, mobile phone manufacturers will look for new growth points, such as strategic investments into startups which could leverage their vast installed base.

Xiaomi’s founder Lei Jun has announced that he will spend $1 billion over the next five years to invest in 100 mobile app startups in India. Other mobile phone brands, including Samsung (which recently invested in an India-focused OTA based out of China), will also follow suite. This is also in line with the real needs of startups when prices for customer acquisition rise.

It sounds great in theory but many factors would impact its actual success.

-

More entrepreneurs enter the fray to build direct-to-consumer brands

Many ecommerce players are effectively bazaars, piling on hundreds of thousands of SKUs. Over the course of this year, we have been reflecting that maybe what is really needed by consumers, especially those in middle class with growing income, is brands.

Western brands have been flooding the mass segment of Indian market for years now but many have struggled to catch the wave of shifting demands of the middle class. The same happened in China by the way, exemplified by P&G’s slumping sales – the brand is perceived as too “mass market”.

Mobile internet has been the biggest enabler for new brands because they have the ability to reach out directly to consumers, through social media and through ecommerce. We expect more direct to consumer brands, good ones, to continue emerging in 2019.

Now do you prefer Bira or Kingfisher?

- Fintech lending would still attract big capital, though only the ones with good core of risk control and data would increase in valuation

India’s fintech sector has generated a large number of well funded startups over the past few years, covering various segments including SME financing, consumer credit, marketplaces and SaaS tools. More than $40 million in financing for a startup in this sector is not news anymore.

That said, the market is still in its infancy, especially consumer facing business models. Regulators (we have to say that Indian regulators are usually very very smart) are keeping a close eye on the sector as well.

Bear in mind that in the business of finance, risk control is the key. Only companies which manage to do that well can grow their valuation in leaps and bounds.

- Late stage Chinese money still prefers to invest, instead of acquire;

The sentiment of Chinese strategic investors towards the Indian market is that big opportunities are not to be missed, but at the same time many are not confident in the short term (rightly so).

Also India, though geographically much smaller, is a much more diverse country than China. To run a subsidiary in a vast foreign country, you need to be able to slowly sink in and plough. Mountains of challenges need to be overcome along the way.

Therefore, strategic investors are making bets in a way in which we see as not wanting to miss the boat, rather than making outright acquisitions to run the companies themselves.

This will continue in 2019.

These opinions are based on our long-term observation and practice in the local markets. If you have different opinions, please leave a comment or write to us at [email protected].

Preview: We will soon be publishing the 2019 forecast for Latin America, so stay tuned!

Momentum Works Emerging Markets Tech Investment Index

Momentum Works has released the Emerging Markets Tech Investment Index for various emerging markets. The image below is an example that shows the projected time between the different stages and the valuations you can expect at each stage:

We also launched Indonesia Fintech 2018 report and Indonesia ecommerce 2018 reports that comprehensively and systematically analyse opportunities, risks and investment opportunities in the respective sectors.

We also launched Indonesia Fintech 2018 report and Indonesia ecommerce 2018 reports that comprehensively and systematically analyse opportunities, risks and investment opportunities in the respective sectors.

If you are interested, please write to us at [email protected] with your name + email + company + position to get more details about the report.