It’s a big pie

In several recent articles, we have emphasized many times that Indonesia will be the next battle ground with huge growth potential in internet and mobile business. Interrelated to opportunities in consumer finance and payment (refer to our previous articles on Consumer Finance and Electronic Payment), e-commerce is no doubt the biggest sector and is growing fast. Some have estimated that Indonesia’s e-commerce market valuation would swell to a whopping US$130 billion by 2020, with an annual growth rate of 50% [1]. This may be an over optimistic outlook by the local government, as Macquarie sees a US$65 billion market in 2020 and IDC expects a US$21 billion market [2]. Nevertheless, the growth of the market is going to accelerate as investment and new players continue to rush in.

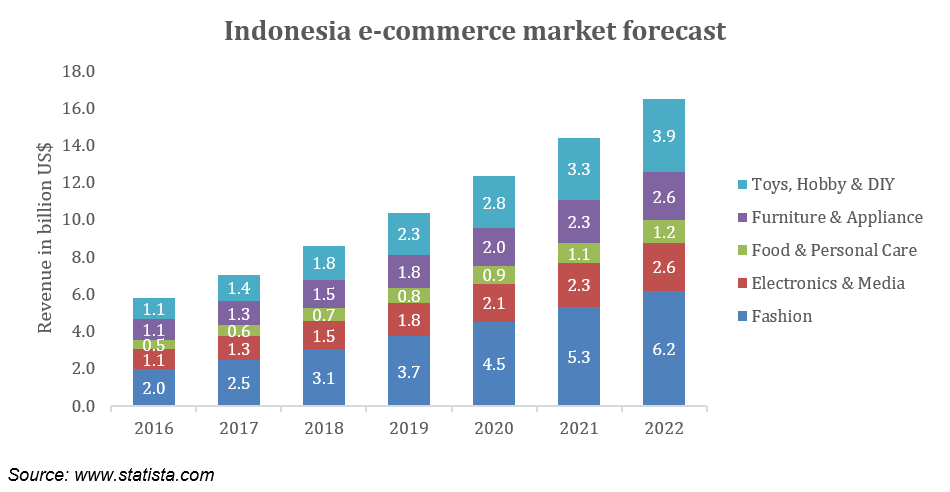

For B2C and C2C sectors, the revenue totaled at US$7 billion in 2017, with fashion taking the lion’s share of the sales[3]. Fashion is also estimated to be the second fastest growing segment after toys, hobby & DIY, with an annual growth rate at over 20%.

Consumers are within reach and going mobile

The long-term market prospect seems promising, but why now? It’s all about timing. Although not all components in the e-commerce value chain are well developed, investments and new players have been entering aggressively, trying to obtain first-mover advantages. The fact is that e-commerce platforms can reach numerous consumers with high internet penetration (51%, 132 million users [4]) and mobile internet penetration (47%, 123 million users [4]).

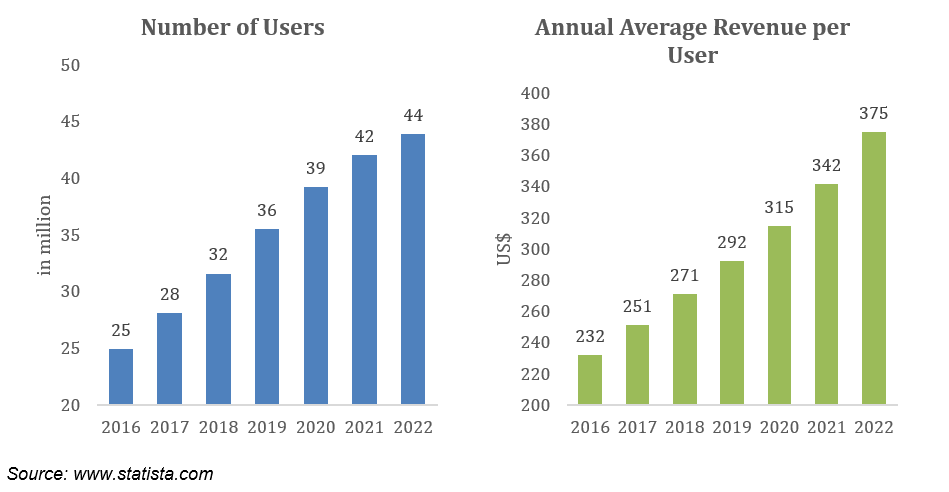

In 2017, e-commerce users are estimated to be 28 million with an annual growth rate of 10%. At the same time, the average revenue per user in 2017 is US$250 and is expected to reach US$375 in 2022.

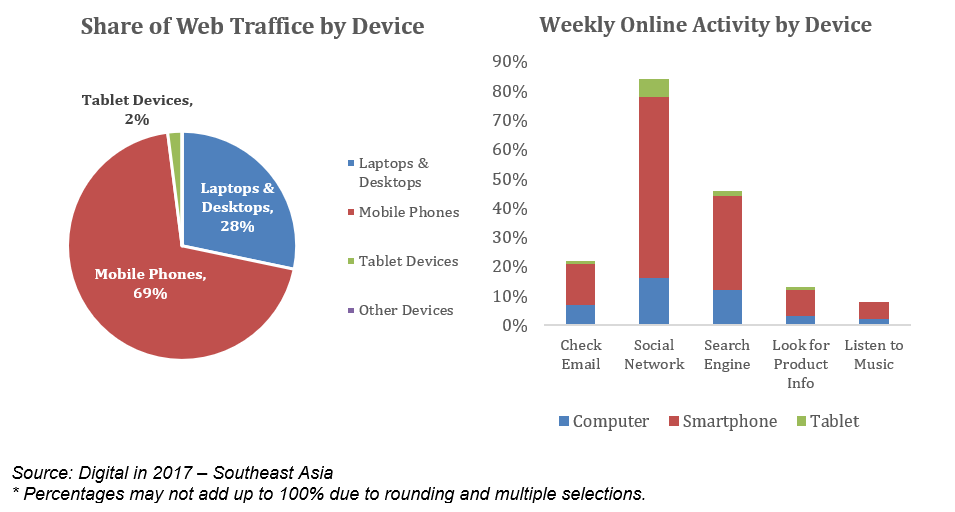

Indonesians rely heavily on mobile phones to access internet (69%, comparing to 28% on laptops & desktops). Among the users, 32% use smartphones to search content and 9% use smartphones to look for products online, about 3 times as many as those who use computers.

However, there is still a gap between internet users and e-commerce customers that the conversion rate is at 21% only. Why? Online shopping experience is still not irresistible to consumers.

According to a survey by MARS Indonesia, more than half of respondents haven’t shopped online because they preferred to buy offline and over 30% don’t trust online shopping. For people who have tried online shopping, the experience does not seem very promising because of a few reasons, such as not being able to try before buying, risk of fraud and products with quality not meeting expectations [2]. However, the positive feedback is that online shopping is practical and saves time for consumers.

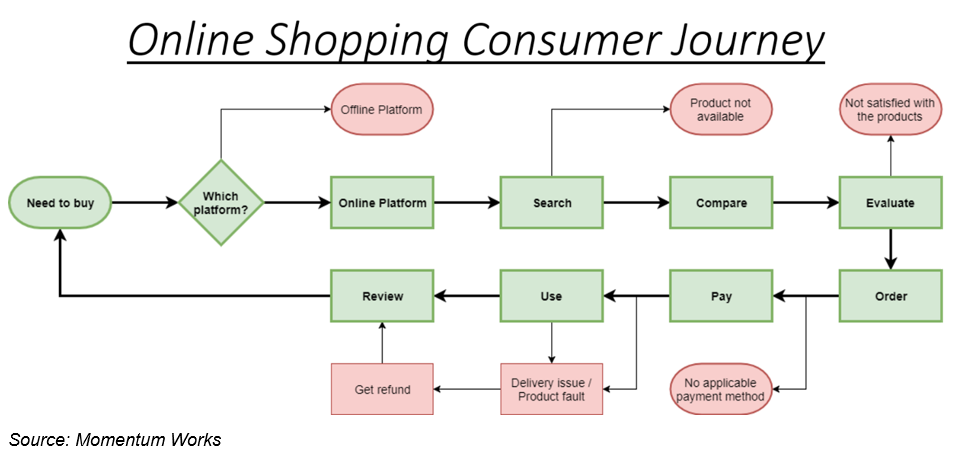

Looking at E-Commerce Consumer Journey

Taking the perspective from a rational consumer in a premature online market like Indonesia, there are many factors that can lead to the end of online shopping experience, even before the journey starts.

While e-commerce players focusing on integrating the infrastructure within the ecosystem, such as payments and logistics, they should also emphasize on building trust with Indonesian consumers and improving the overall consumer experiences. Whoever answers these questions better will take advantages in the race.

Changing Landscape in E-Commerce Market

In 2017, the biggest investment in Indonesia’s e-commerce was led by Alibaba, with US$1.1 billion into Tokopedia [5], the largest C2C marketplace in Indonesia. It marked a further step of expansion into Southeast Asia, after taking over the controlling shares of Lazada in 2016 by US$1 billion [6] and with subsequent investment of US$1 billion in 2017 [7].

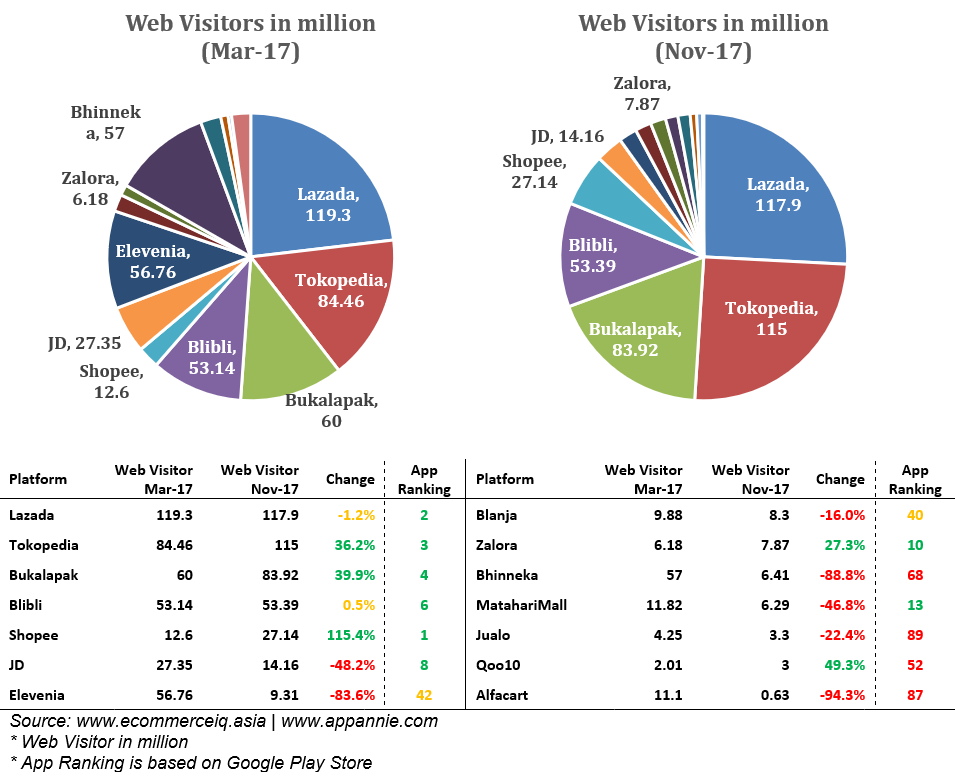

Just over past 12 months, the dynamics among competitors has changed significantly based on web traffic. Bigger players like Lazada, Blibli maintained a stable user traffic to their platforms, while pure C2C players such as Tokopedia and Bukalapak have achieved strong growth (over 30%) in volume of visitors. Smaller foreign players like Zalora and Qoo10 managed to make a lift on their user traffic. Shopee hit a striking 115% growth in traffic, making it the 5th most visited e-commerce platform in Indonesia [8]. On the other hand, local players like Bhinneka and Elevenia had a pitfall and their future remained gloomy.

Nowadays more consumers shop online through mobile devices, and the big players have also gained comfortable grounds from their apps. The top 6 platforms by web traffic are also ranked within Top 10 in Google Play Store. The trend is expected to continue into 2018, and more players will be squeezed out of the game. From the charts above, platforms (Lazada and Tokopedia) invested by Alibaba have occupied over half of the national web traffic, while Shopee tops in mobile apps. More intense competitions will be observed in near future. Nevertheless, some players – including our clients – are still seeking for market entry and expansion in Indonesia, amid the industry’s optimistic perception on the market potential.

Regulatory Environment

After the announcement of Regulation 44 in 2016, 100% foreign ownership is allowed for e-commerce companies which have invested 100 billion IDR (US$7.4 million) or more. Otherwise, the maximum foreign ownership is capped at 49%. With the Three-Hours Investment Licensing Service launched in 2015, companies can be established in three hours instead of 21 days before [9], indicating the government’s effort in attracting foreign investments.

In 2017, the finance minister of Indonesia revealed the plan to release a tax regulation on e-commerce industry soon [10]. The regulation will provide a comprehensive guideline for collecting taxes from international and local e-commerce companies. The scheme is expected to include both Income Tax and Value-Added Tax at various stages of the e-commerce value chain. Once the new tax regulation is implemented, all players will see a share of their revenue flowing to the government, and smaller players with less deep pockets may take more severe damage compared to the larger players.

Although the regulatory environment of e-commerce companies is still friendly, payment may pose risks in the future. As one of the most important links in the e-commerce value chain, the government has been strict on the electronic payment industry. With the recent launch of National Payment Gateway (NPG), government is aiming to push for a standard electronic payment system. You can read our previous article [MV Special Report] Payment Overview in Indonesia for more information. The integration between the e-commerce platform and the future e-payment system can be crucial. Foreign companies may face challenges in expanding their own payment vehicles or in international transactions.

Opportunities and Risks

Generally, the prospect of e-commerce is bright with continuous growth in revenue and customers. Both international and domestic players have established their grounds, but the landscape is constantly changing. Still, there may be room for new players to enter depending how fast existing companies acquire new consumers and how well they manage customer retention.

One challenge faced by all e-commerce platforms is the infrastructure of payment. In Indonesia, cash on delivery (COD) and bank transfer are still the most popular payment methods for online purchases. The former adds on the operating cost of sellers and the later induces inconvenience to customers which at the same time deteriorates the overall customer experience. Given the low penetration of online banking, debit cards and credit cards, the best solution is electronic payment. However, Bank Indonesia (BI) has strict controls over issuing the license of electronic money operators. So far, only 26 licenses have been issued over the past 9 years [11] and the number of new issuance is not predictable. In 2017, extended e-money services, such as TokoCash (by Tokopedia) and ShoppePay (by Shopee), have suspended their credit top-up features while waiting for the approval from BI for their e-money operator licenses. One way is to corporate with existing e-money operators such as Go-Pay and GrabPay (powered by OVO), however whether a seamless integration will happen is still uncertain.

Through our recent work on client projects in Indonesia, we’ve come to the conclusion that the custom clearing experience has been improved tremendously over the last 12-18 months with standardized and impressively transparent procedures. We believe that the efficiency of logistics before domestic transportation and last mile delivery will improve by 1 to 3 days. Many third-party logistics (3PL) providers are present in Indonesia (even Go-Jek started courier services), but the risks are that the progress and quality can sometimes be out of control. The status will solely be relied on the feedback from 3PL partners. On the other hand, some big players (like Lazada) chose to build their own warehouses and domestic delivery networks. Which way is better in Indonesia’s context? Please wait to see our subsequent article on Logistics Overview in Indonesia.

Conclusion

With a fast growing economy and uprising household incomes, the e-commerce market may not be saturated for several years. Remember the high consumer confidence index (120, 4th globally [12]) and mobile internet penetration (47% [4]). With the development of infrastructures in e-commerce value chain, e-commerce players who can provide higher-quality customer experience will take advantages in customer acquisition and retention. The main focus should be on building trust with consumers, including sufficient choices of products, quality of products, quick delivery, user friendly user interface (UI) and secure payment methods. That said, the risks embedded along the entire consumer journey should be mitigated or even removed, simply because the integration of all links in the value chain contributes a big part of customer experience.

References

- All eyes on Indonesia’s e-commerce pie, www.straitstimes.com

- Ecommerce still falls behind expectations in Indonesia, www.techinasia.com

- Indonesia eCommerce Market Report, www.statista.com

- Digital in 2017: Southeast Asia, We Are Social & Hootsuite

- Alibaba leads $1.1b investment in Indonesia’s Tokopedia, www.techinasia.com

- Alibaba pours a total of $1B into Southeast Asia e-commerce platform Lazada, www.techcrunch.com

- Alibaba ups its stake in Southeast Asia’s Lazada with $1 billion investment, www.techcrunch.com

- Indonesia – The Country’s Top Ecommerce Websites, www.ecommerceiq.asia

- Press Release: Vice-President Launched Three-Hours Investment Licensing Service, Indonesia Investment Coordinating Board

- Indonesia: Taxation on e-commerce transactions, International Tax Review

- List of electronic money operators licensed by Bank Indonesia, September 14th 2017, Bank Indonesia Website

- Q4 2016 Global Consumer Confidence, viz.nielsen.com

4.0")