In mid September, Grab released its Q2 2021 results, the first quarter that was compared to a Covid-impacted year-ago period. The statements shared contained valuable information, especially about the true effects of the pandemic, which we covered in our previous article.

While Covid is still impacting businesses in most of Southeast Asia, on 11 November 2021 Grab presented its Q3 2021 results. In addition, Grab provided an update on its IPO process as well as strategic priorities for the upcoming quarters.

Here is our take on the key highlights of Grab´s Q3 2021 earnings call.

Top line growth, widened losses, and strong cash position

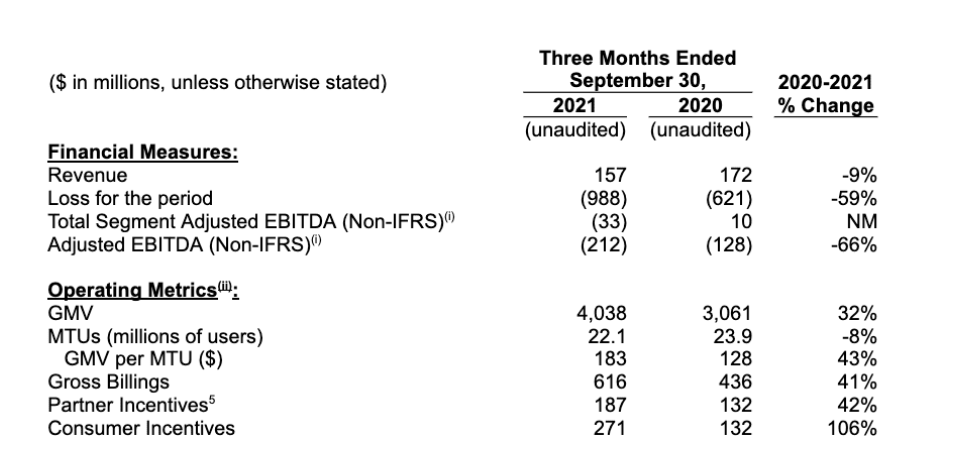

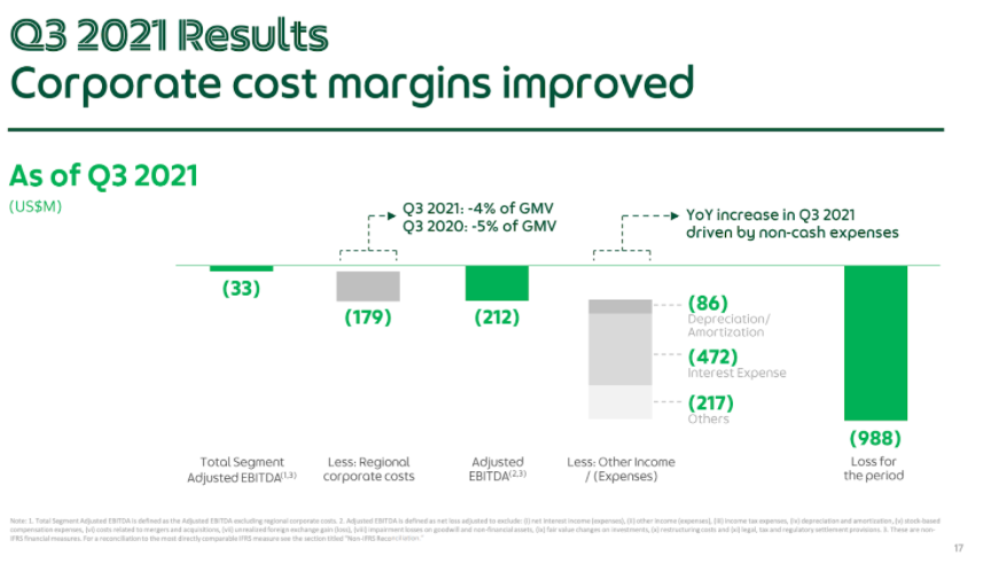

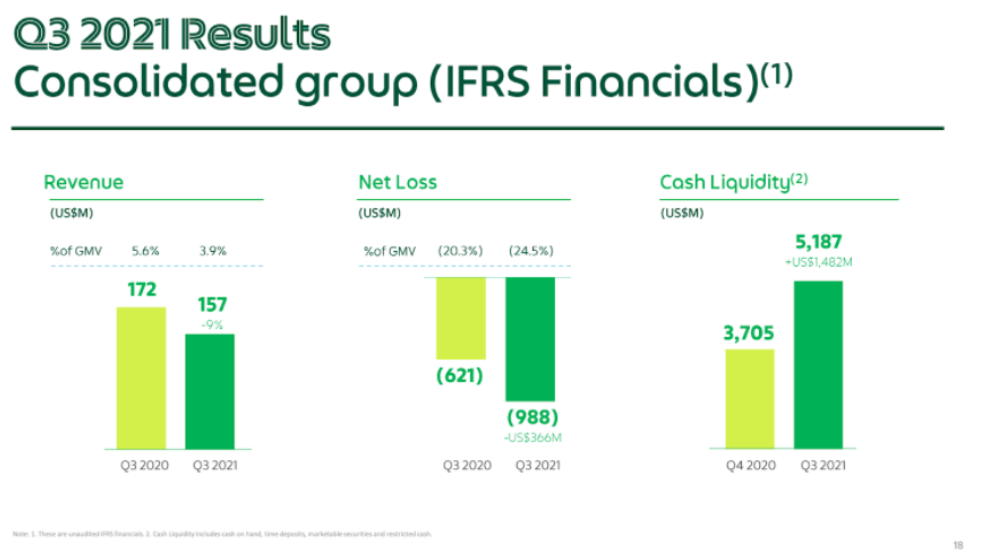

First, top line growth continued, despite movement restrictions in much of Southeast Asia, and particularly in Vietnam, during the quarter. Grab’s quarterly GMV reached $4.0 billion for the first time, increasing by +32% YoY and +4% QoQ. Gross billings, which is basically take rate, also went up 41% YoY to reach $616 million.  Losses, however, have widened to US$988 million. However, more than ¾ of these (US$775 million) are non cash items attributed to accrued interest on convertible redeemable preference shares (CRPS), depreciation/amortization and other non cash items. As explained earlier, the accrued interests of CRPS will disappear when the company goes public.

Losses, however, have widened to US$988 million. However, more than ¾ of these (US$775 million) are non cash items attributed to accrued interest on convertible redeemable preference shares (CRPS), depreciation/amortization and other non cash items. As explained earlier, the accrued interests of CRPS will disappear when the company goes public.

That, put together with Grab’s $5.187 billion cash position, would mean that the business will be able to invest in operations for a very long time. That is not even considering the proceeds it will receive from the SPAC business combination and public listing.

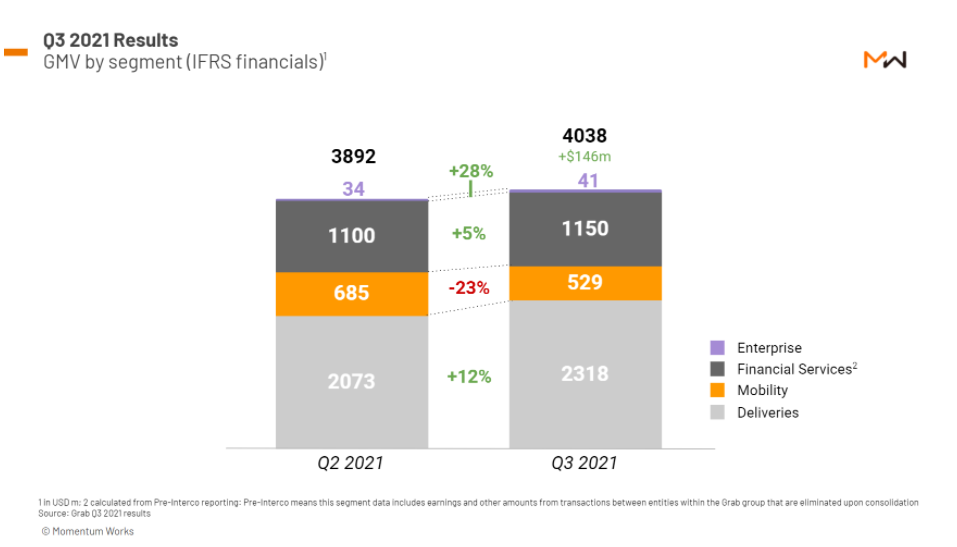

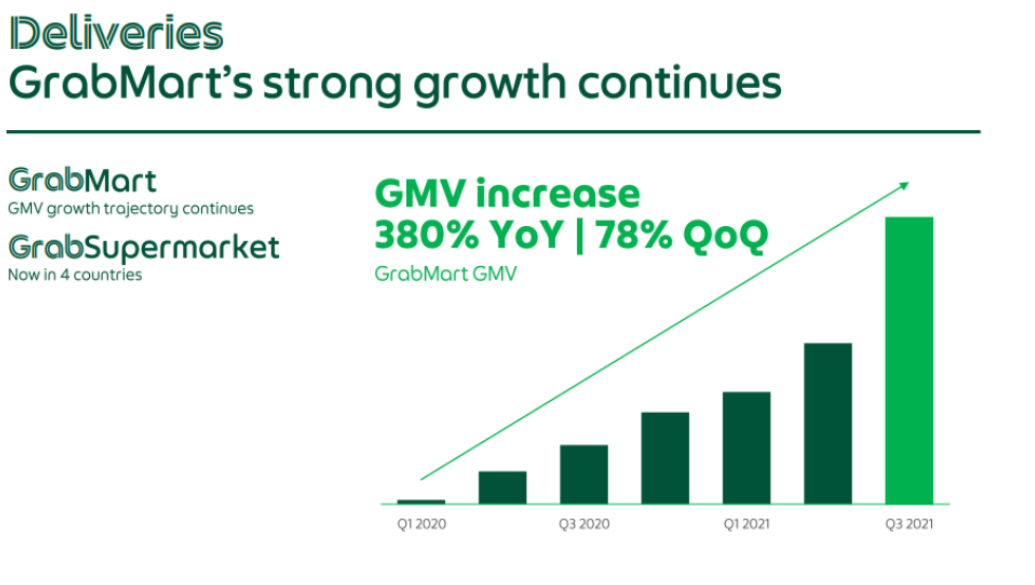

Deliveries are in the spotlight

To understand more about how each of Grab’s business units has been performing, let’s disaggregate the numbers by segments:

On a QoQ basis, the Mobility segment showed a significant (23%) decline as the covid-19 situation intensified in much of the region in the quarter. The deliveries segment, however, showed significant QoQ growth, offsetting the Mobility decline.

A significant portion of Grab’s deliveries growth can be attributed to the expansion of GrabMart, which almost quadrupled GMV on a yearly basis. Here Grab pursued a strategy where it leverages its large user base, delivery and payment networks to work with partners with inventory and assortments in different markets. Its new partners include Indomaret in Indonesia (>15,000 stores), Big C in Thailand (>1,000 outlets), Lotus’s Malaysia (formerly Tesco Malaysia, 62 hypermarkets), S&R supermarket in the Philippines and Mega Market in Vietnam.

Cautious optimism for Q4

Cautious optimism for Q4

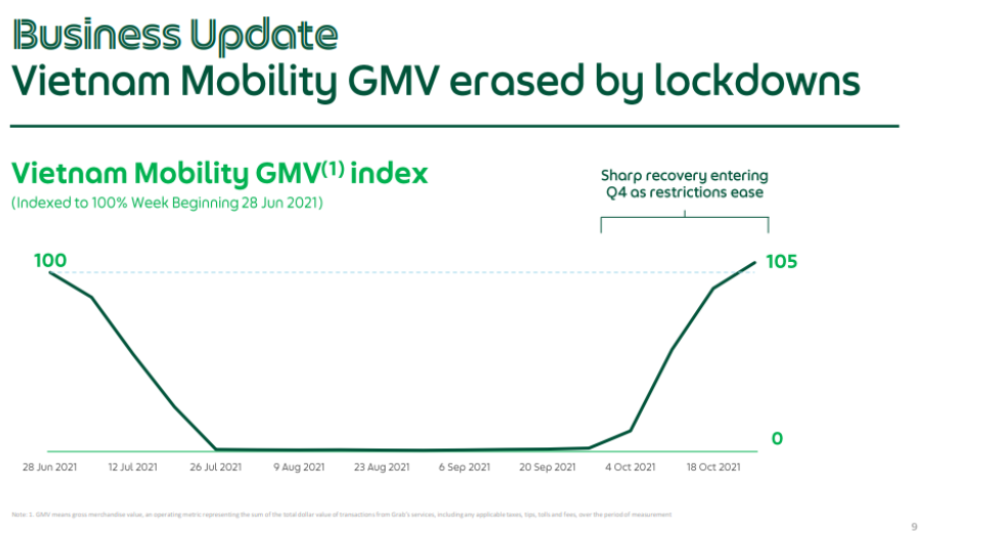

The good thing is that Mobility is recovering, also particularly in Vietnam. The following graph shared during the earning call is quite telling:

From July to the end of September mobility GMV was zero or close to zero. However, with the steep drop in daily cases in October measures have been eased, pushing Mobility GMV back to pre-lockdown levels.

From July to the end of September mobility GMV was zero or close to zero. However, with the steep drop in daily cases in October measures have been eased, pushing Mobility GMV back to pre-lockdown levels.

This was an example of the reason why Anthony Tan, Grab’s CEO, said that the team was cautiously optimistic about recovery of mobility business in Q4. This optimism is contingent on the Covid situation improving further thanks to the elevated vaccination rates across the region.

A definitely bright side is that the mobility is still segment-wise profitable, achieving US$64 million positive Segment Adjusted EBITDA in Q3 2021. Grab is leading definitely in ride hailing across the region, and this segment is expected to continue to provide the cash flow for the group.

How is Grab addressing these challenges?

In the Q3 earnings call, Grab presented several strategic updates with a heavy focus on the expansion of the deliveries segment.

The management sees a large opportunity across both online and offline demand for prepared meals and groceries: “Our strategy is to be the go-to platform for anything that our consumers want to eat”, Ming Maa, President of Grab mentioned during the call.

The opportunities here are massive – where volume, density and operational efficiency are the key winning factors. Expect the team to be on the grind for the next few years to try to capture this expanded TAM.

We are currently collecting data to issue an updated version of “Food Delivery Platforms in Southeast Asia”. Expected launch date would be in mid January – do keep an eye on it!

On the financial services side, a key update is Grab increasing ownership of OVO effective 1 October, acquiring stakes from Tokopedia to accumulate close to 90% share ownership in the business.

As we explained in our Blooming Ecommerce in Indonesia Part 2.1 Payment report, OVO has remained the leading independent (i.e. non-embedded, or what Grab calls “open ecosystem”) wallet in Indonesia. It should be able to focus more on building a digital financial super app since it has been unshackled from the splitting priorities under the Grab – Tokopedia dual parent previously.

Is the IPO process still on track?

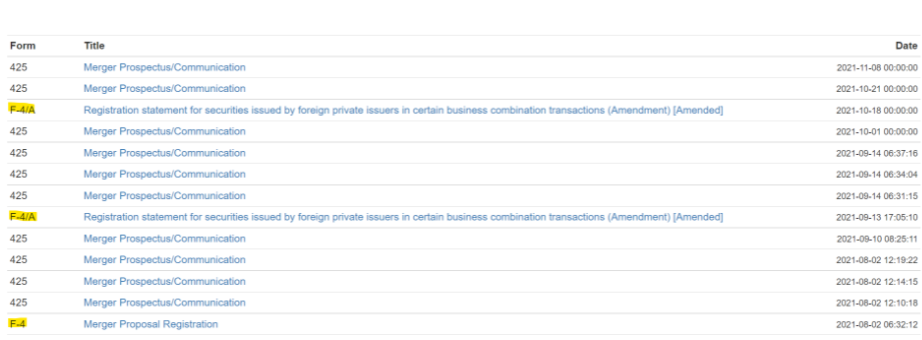

A key question many had is whether Grab’s SPAC merger for public listing remains on track. In the earnings call, Peter Oey, Grab’s CFO, sounded confident about the Q4 2021 timeline.

However, the exact dates are probably still pending on SEC approving Grab’s F-4. The form has undergone 3 iterations since the company first filed the first F-4 on 2 August.

Another revised F-4 will be filed soon, according to Oey. Once the F-4 is cleared, both Altimeter Growth Corp and Grab will issue an extraordinary general meeting notice to their shareholders.

After the shareholders’ approval, Grab will be in a position to move forward with the public listing very quickly. In a nutshell, expect about 3 weeks from the clearance of F-4.