Last week, Grab released its amended F4 as well as its Q2 2021 financial results. Q2 2021 was the first quarter that compared to a Covid-impacted quarter a year ago, both Q2s saw severe surges in cases and large-scale lock downs across the region. Grab’s statements thus contain valuable information, especially about the true effects of the pandemic.

The widening loss and the downward adjustment of full year projection naturally made attractive media headlines:

We have always argued that for growth companies, we need to understand what are causing the losses in order to properly assess the prospects of the business.

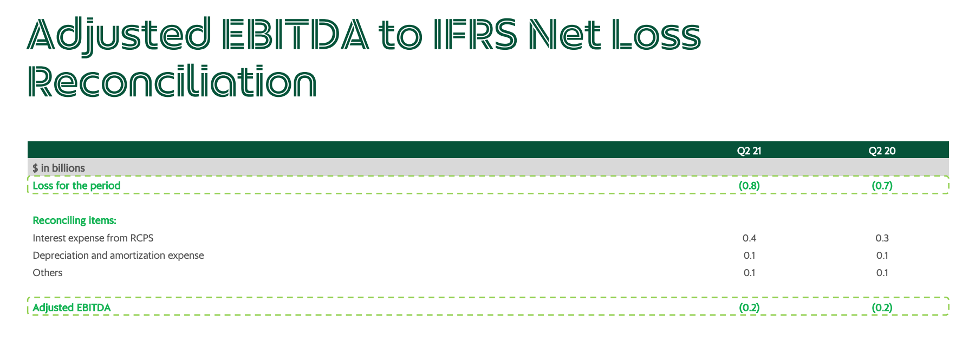

As we explained in the previous post on Grab’s Q1 results, a majority of the losses are non-cash items attributed to the interest of Redeemable Convertible Preferred Shares (RCPS), which will disappear once the company lists.

Here is our analysis on key highlights of Grab’s Q2 2021 performance.

Here is our analysis on key highlights of Grab’s Q2 2021 performance.

The impact of Delta variant

Compared to a Covid-shook Q2 2020, where most of Southeast Asia was also on lockdown, Grab’s overall GMV increased by +62% YoY to $3.9 billion, making Q2 2021 the all-time high quarter.

However, on a sequential basis (QoQ) this translates into a more modest growth of 6%, driven by continued mobility restrictions across countries.

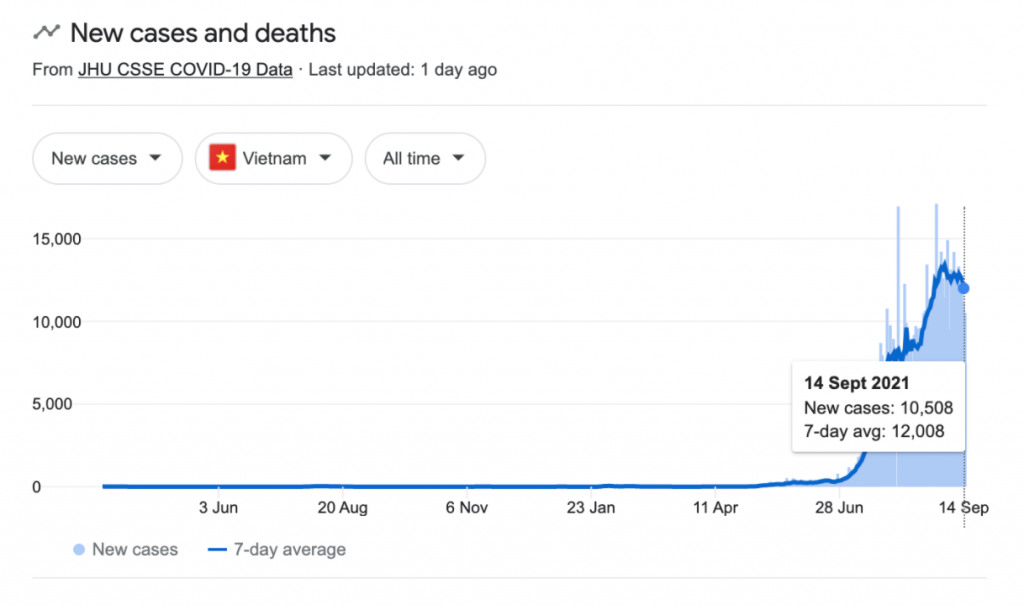

As we all know, from May this year onwards Southeast Asia has been the hardest hit region globally by the more transmissive Delta variant. Just to give a bit of context, Vietnam implemented probably the strictest lockdown measures in the region. In addition to mobility, food delivery, which is considered essential services in many other countries, was also restricted.

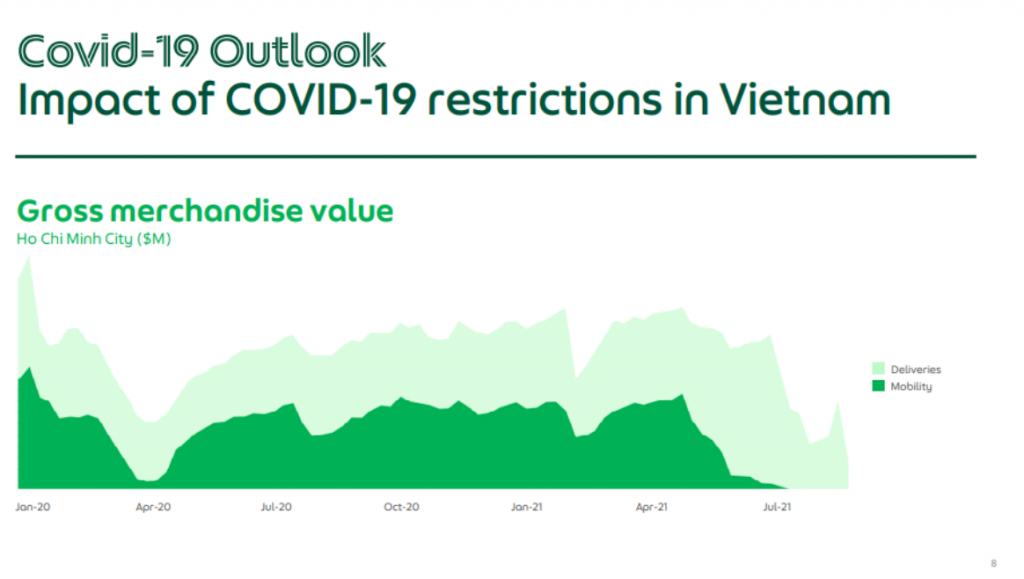

Hence, in its earnings presentation, Grab showed the drastic reduction in mobility and impact on deliveries that were caused by the lockdowns in Ho Chi Minh City, as can be seen below:

The even stricter restrictions in and around Ho Chi Minh City will probably impact Q3 numbers (and even maybe Q4), as the covid situation in Vietnam significantly worsened from the end of June – probably a major contributor to the downward adjustment of the year’s projections. Most of these cases concentrated in the southern part of the country around Ho Chi Minh City:

The even stricter restrictions in and around Ho Chi Minh City will probably impact Q3 numbers (and even maybe Q4), as the covid situation in Vietnam significantly worsened from the end of June – probably a major contributor to the downward adjustment of the year’s projections. Most of these cases concentrated in the southern part of the country around Ho Chi Minh City: The even stricter restriction in and around Ho Chi Minh City will have a severe impact on Grab’s Q3 (and even maybe Q4) numbers – probably a major contributor to the downward adjustment of the year’s projections.

The even stricter restriction in and around Ho Chi Minh City will have a severe impact on Grab’s Q3 (and even maybe Q4) numbers – probably a major contributor to the downward adjustment of the year’s projections.

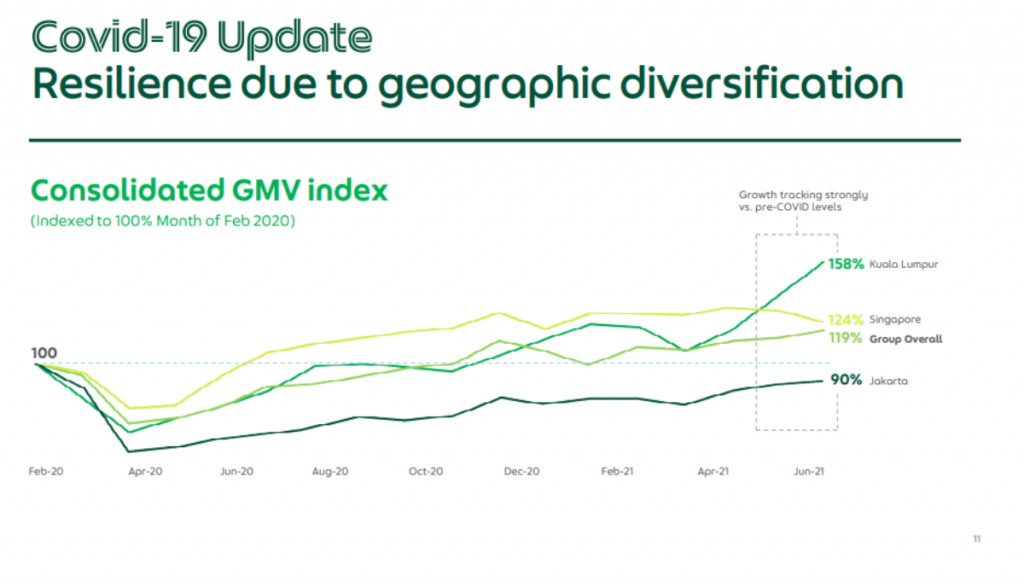

While the impact to Grab’s numbers in Vietnam is more drastic, covid also has impacted other mega cities in Southeast Asia to different degrees. Jakarta, the biggest metropolis in the region in terms of population, remained weak compared to pre-covid-levels. On the other hand, Singapore and especially Kuala Lumpur have grown to above Q2 2020 levels a long time ago because of high vaccination rates.

Segment performance

Segment performance

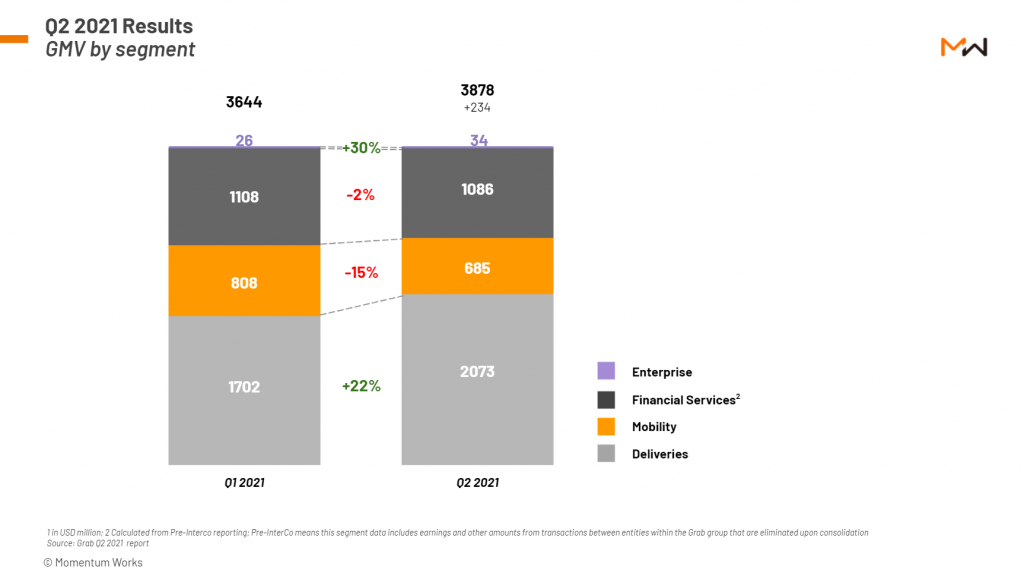

Looking at the break down of Grab’s GMV by business segment, we can see that mobility is, predictably, the most impacted sector by the Delta outbreak, dropping 15% quarter over quarter.

Financial services again contributed to most of the operational losses incurred by the group. For example, off-Grab payment, where GrabPay users pay third party merchants directly, remains weak amid movement restrictions.

Deliveries, which Grab has doubled down on, is showing double digit growth QoQ (22%). The Adjusted EBITA margin has also improved from -2.7% to -0.9% YoY.

Enterprise business, which includes ads, map and fraud/risk solution, has been growing QoQ by 30%.

Besides GMV, what other metrics to judge the company’s performance?

It is arguable whether GMV is still the best indicator for Grab’s actual business performance, as each business segment in the super app is actually quite different.

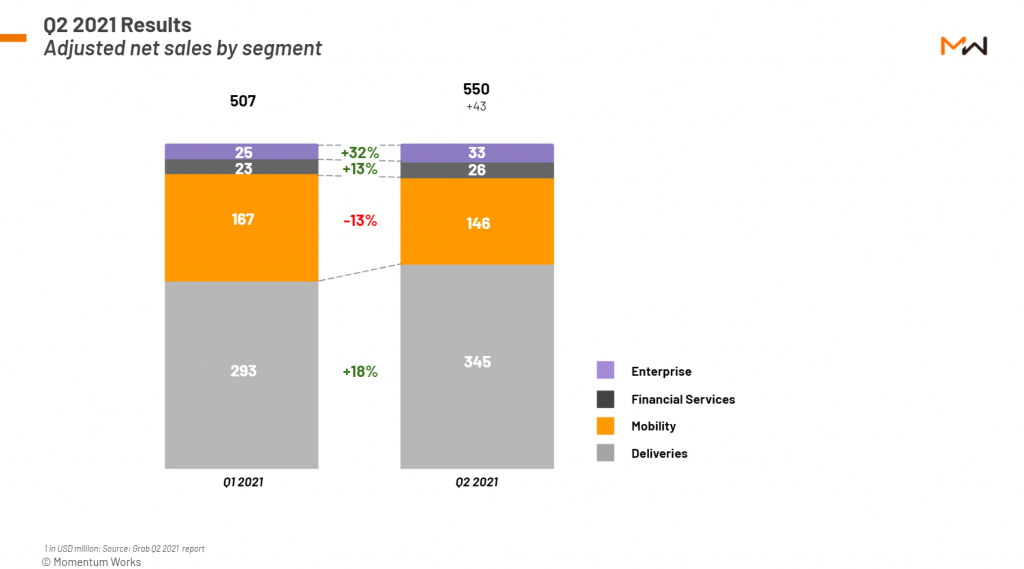

Grab sees Adjusted Net Sales (ANS), which is defined as Gross Billings (you can think of it as take rate) minus ‘base’ (i.e. more permanent, not temporary) incentives paid to drivers and merchants, as a key indicator of the company’s performance.

Looking at ANS terms, we actually see a 8.5% growth at the group level, as well as a 12.6% growth of financial services. The other sectors are more or less in line with the GMV growth:

While there are some debates on whether ‘temporary’ incentives are indeed temporary, investors can also look at revenue and adjusted EBITDA to get a more holistic view in order to form their own judgement. Also look into how comparable platform companies derive their definitions of revenue, as there are varying ways of revenue recognition. We did some comparisons in our analysis of Grab’s Q1 2021 earnings.

Doubling down on deliveries

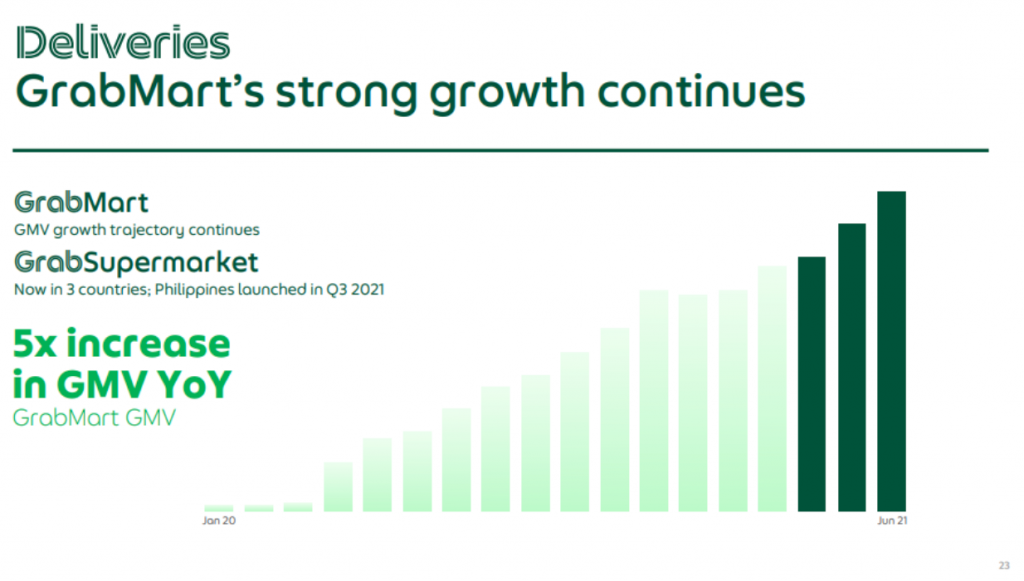

In its earnings presentation, Grab mentioned that GMV-wise, its Mart business within the deliveries segment has been growing consistently month over month since the beginning of last year. In the meantime, operation-wise, it also improved the productivity of the fulfilment fleet by 58% YoY.

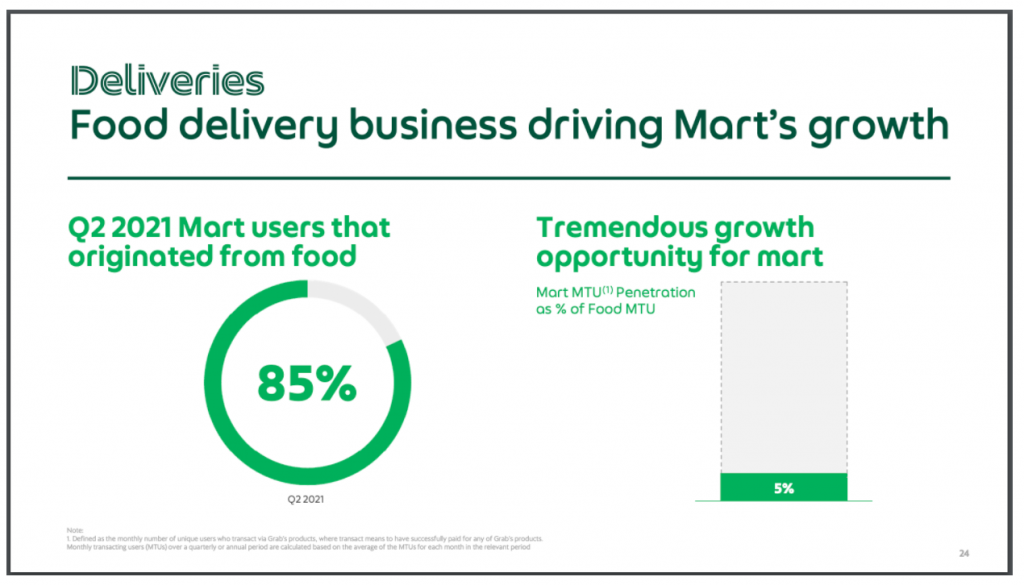

The company plans to convert more customers from its regionally leading food delivery business into GrabMart. Currently, 85% of Mart users originated from food, but only 5% of food users use Mart. This could be a good growth opportunity.

The company plans to convert more customers from its regionally leading food delivery business into GrabMart. Currently, 85% of Mart users originated from food, but only 5% of food users use Mart. This could be a good growth opportunity.

It also launched its Supermarket in three countries as a sub vertical of its deliveries business, with Thailand the next country for roll out. This has some similarities with China’s community group buy (where Meituan and Pinduoduo are leading) in the sense of pre-order and next day delivery (so minimized inventory/wastage).

What is the road ahead for Grab?

In its outlook on full FY21, Grab cuts its forecast announced earlier this year. GMV is expected in the range of $15b-$15.5b (down from $16.7b) and adjusted Ebitda loss will increase to up to $-0.9m (down from $-0.6m).

Our opinion is that investors need to examine carefully the numbers to determine which are caused by the short term covid-19 surge, and estimate when such effect will wear off and the growth will resume to a normal speed.

At least we know that most other Southeast Asian countries are making steps towards opening up in the last quarter of the year. The effects of covid-19 will last for a bit longer, but will eventually wear off.

With the increased investment in deliveries, foray into mart and BNPL, will Grab be able to convince investors? It has a lot to prove.

Anyway, after the SPAC merger, Grab will have more than US$9 billion in the coffers, it will be able to ride through short term challenges.